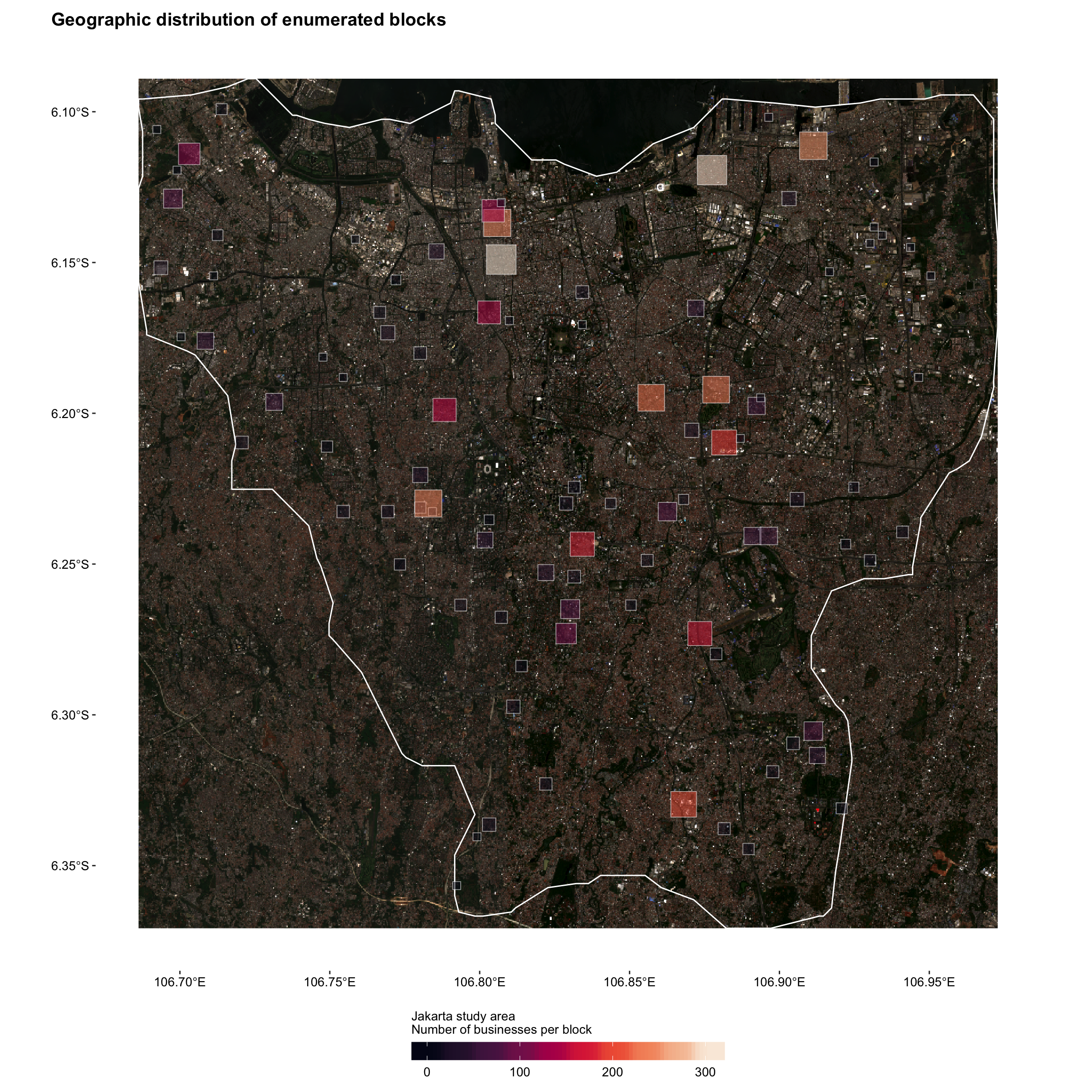

Enumeration was completed in 72 out of 96 initial sampled blocks.

18 of the 72 initial sampled blocks enumerated resulted in expansion to adjacent blocks

184 blocks (including both initial sampled and expansion blocks) were enumerated.

In total, 4460 business were found during enumeration

Of all businesses, 2,887 (65%) were eligible for the study

Of eligible businesses, 905 (31%) were selected at random for interview

Of selected businesses, 812 (90%) were successfully interviewed

Successful interviews originate from 20 initial sampled blocks

Figure 1: Geographic distribution of enumerated blocks

The business landscape

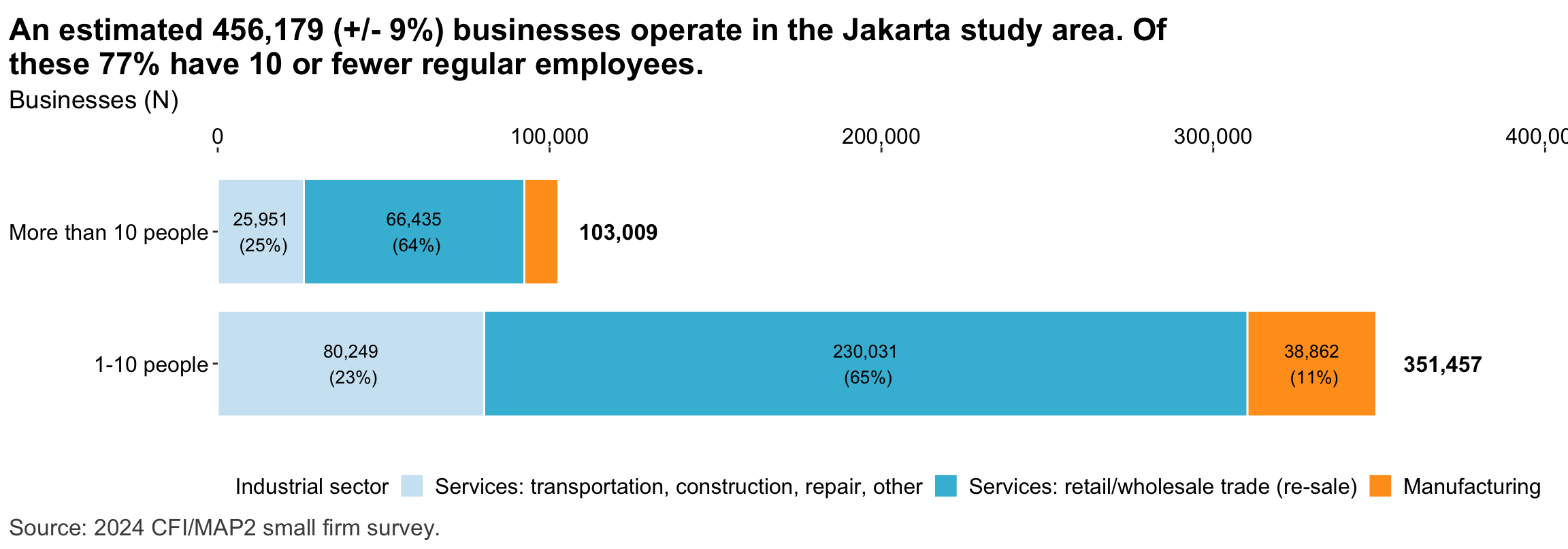

Figure 2: Estimated business population by size and sector

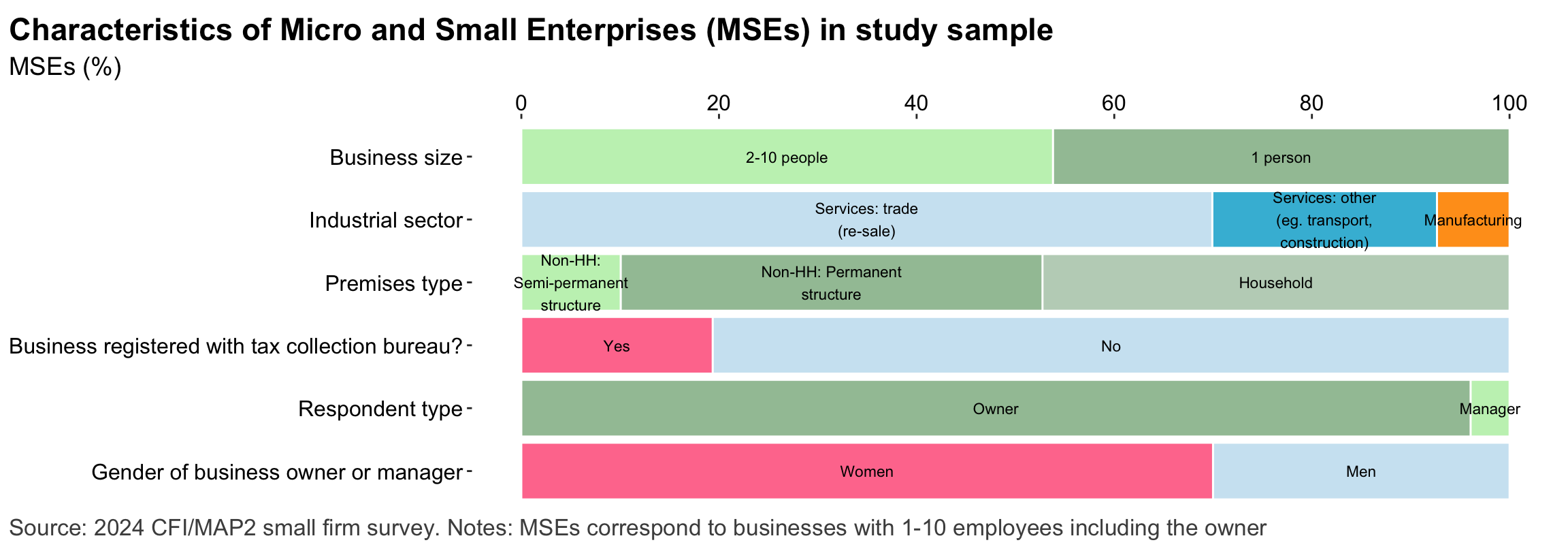

Figure 3: MSE sample characteristics

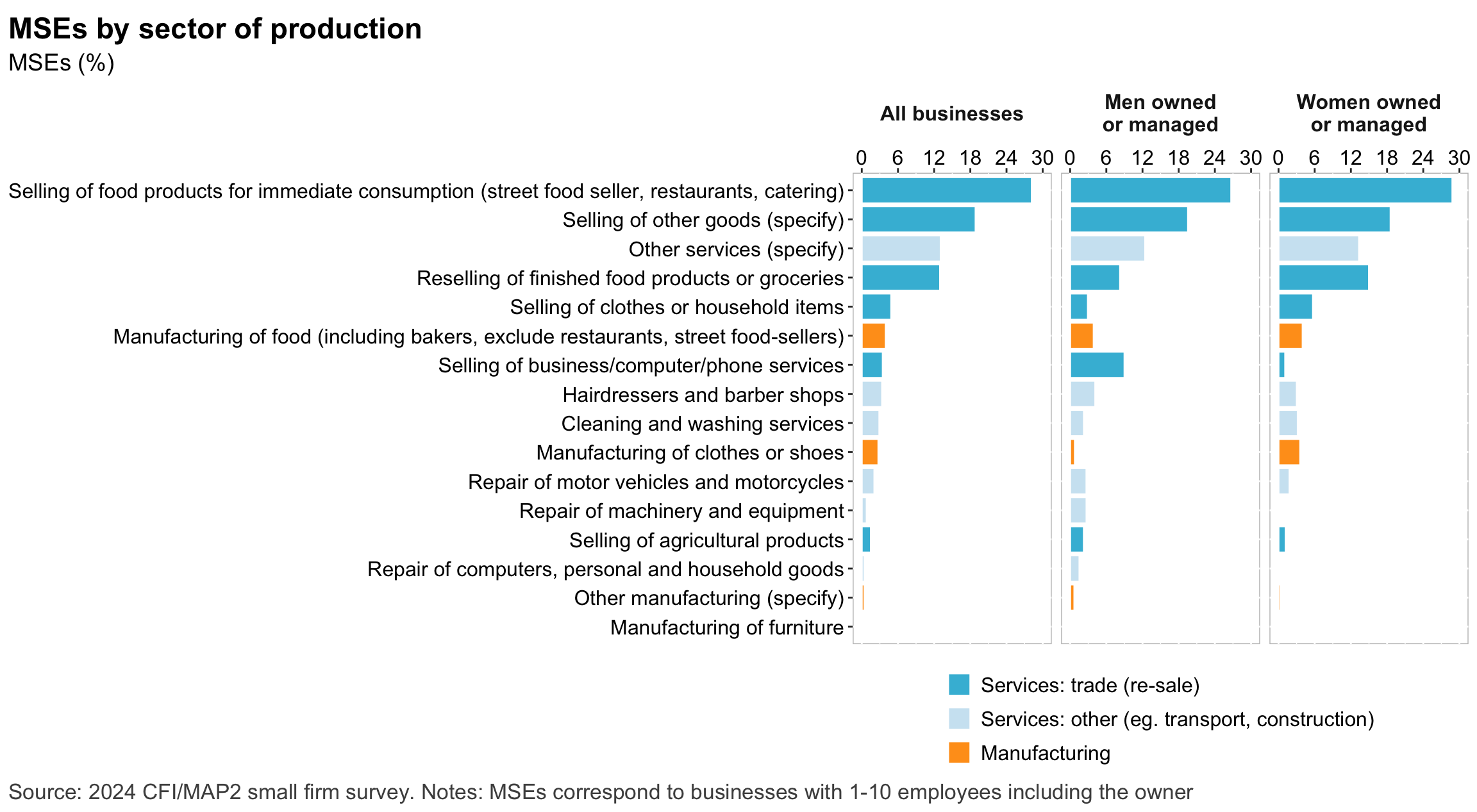

Figure 4: MSEs by sector of production

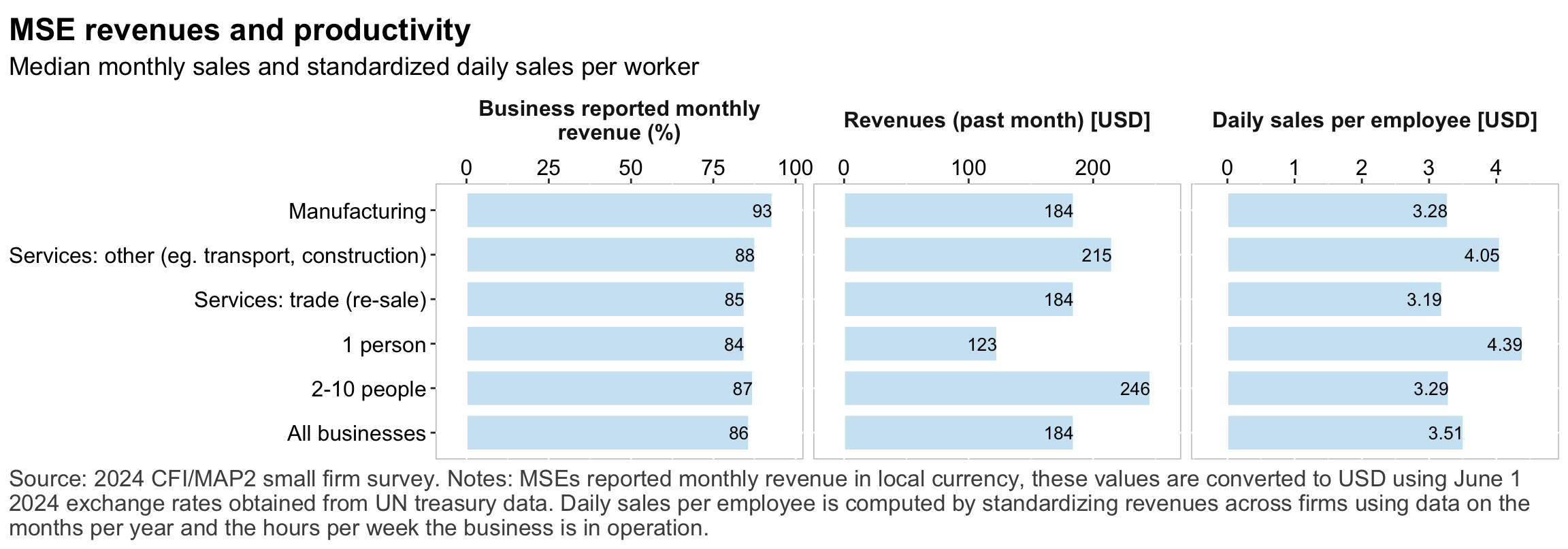

Figure 5: MSE revenues and productivity

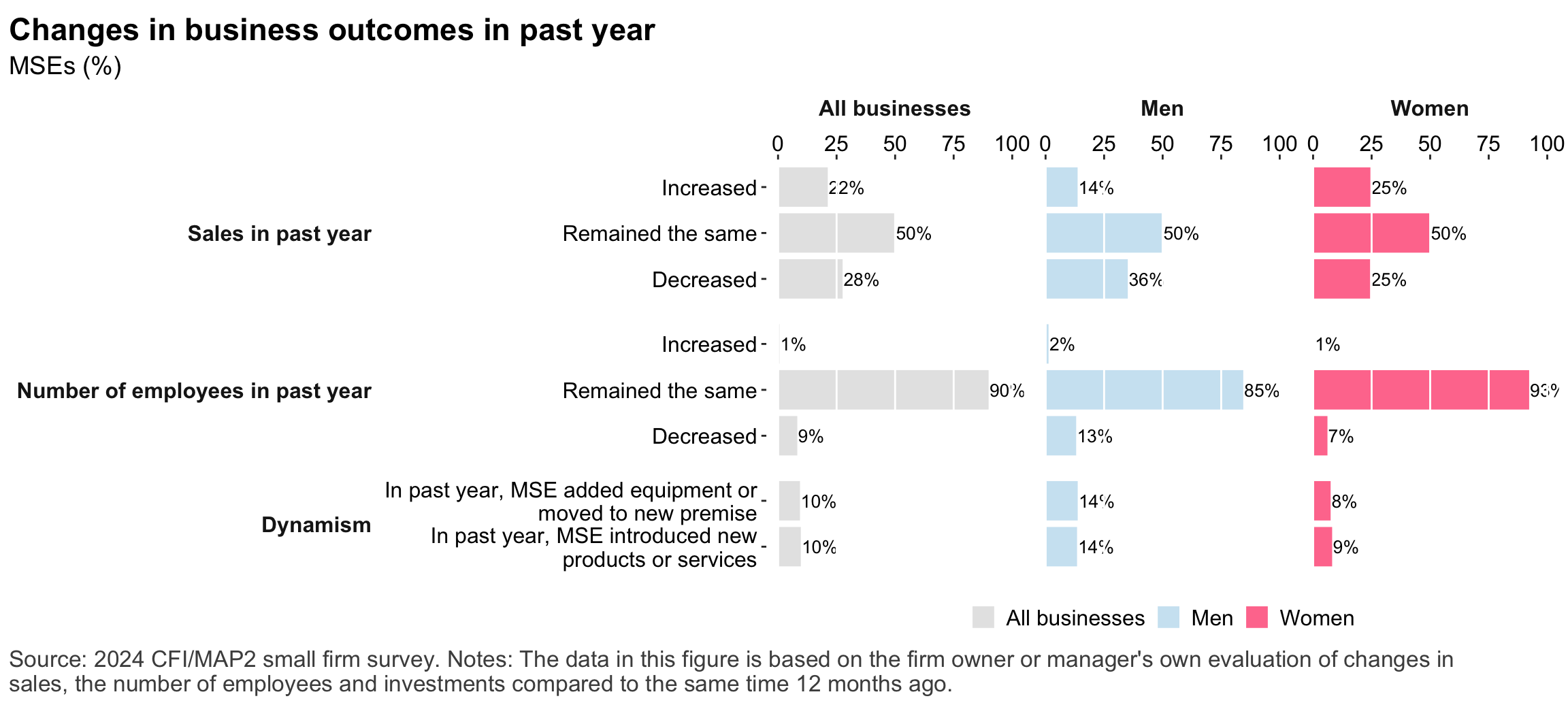

Figure 6: Changes in MSE outcomes in past year

The small firm owner

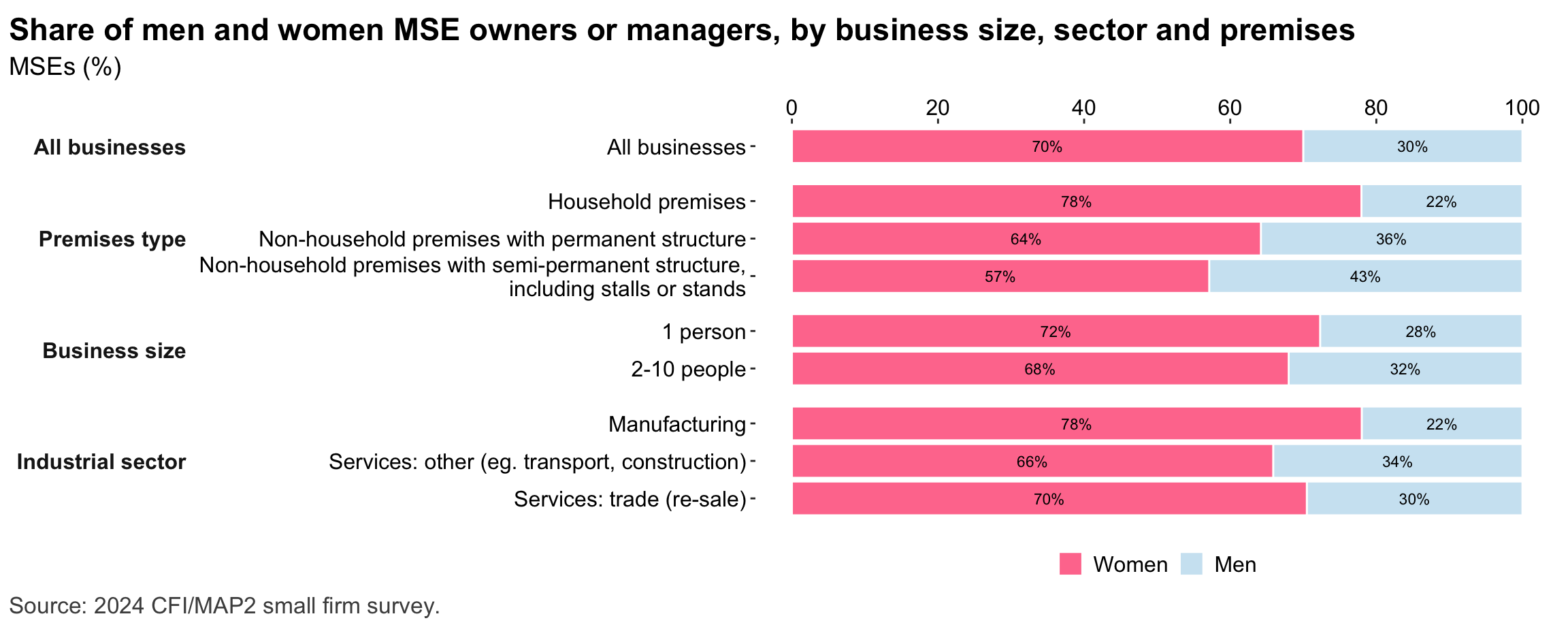

Figure 7: Gender composition of MSEs by sise and sector

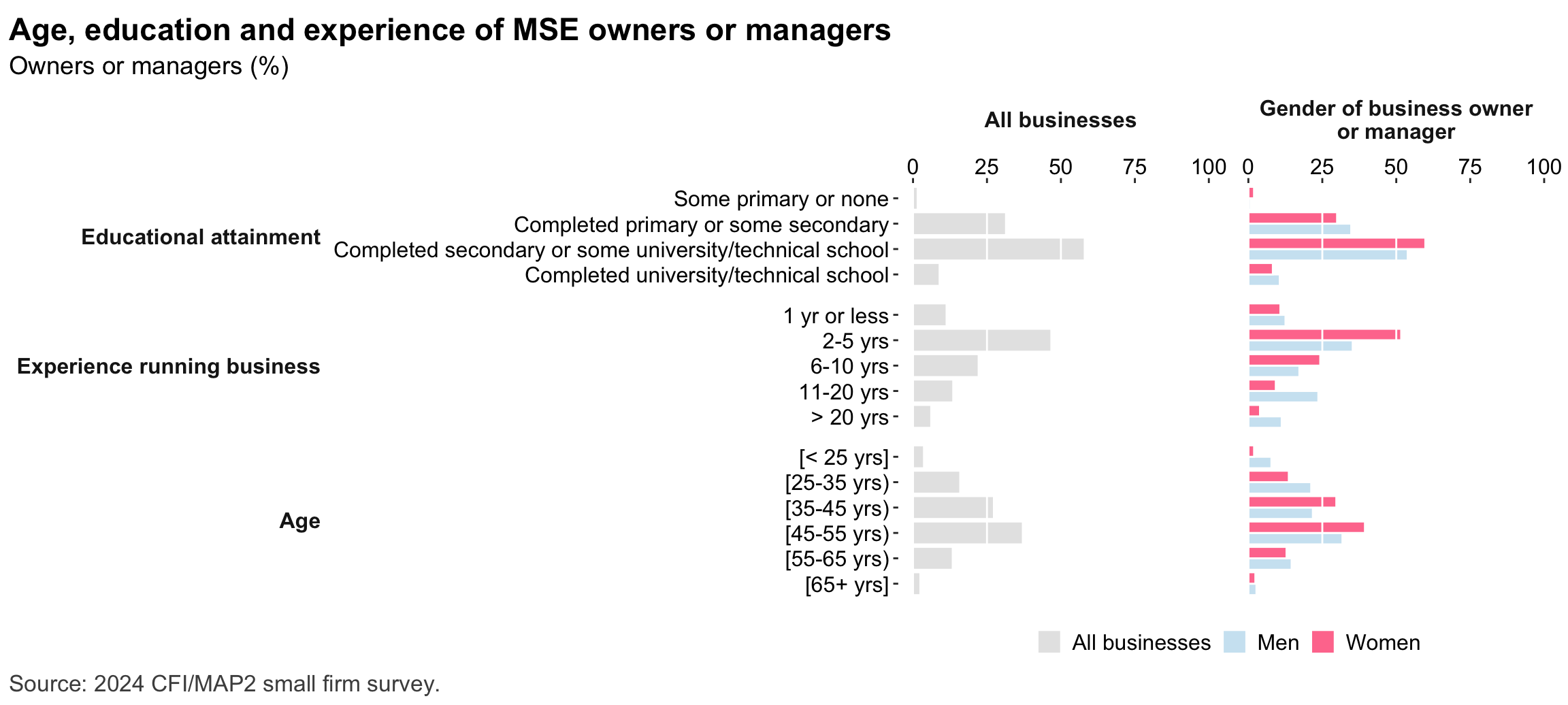

Figure 8: MSE owner characteristics

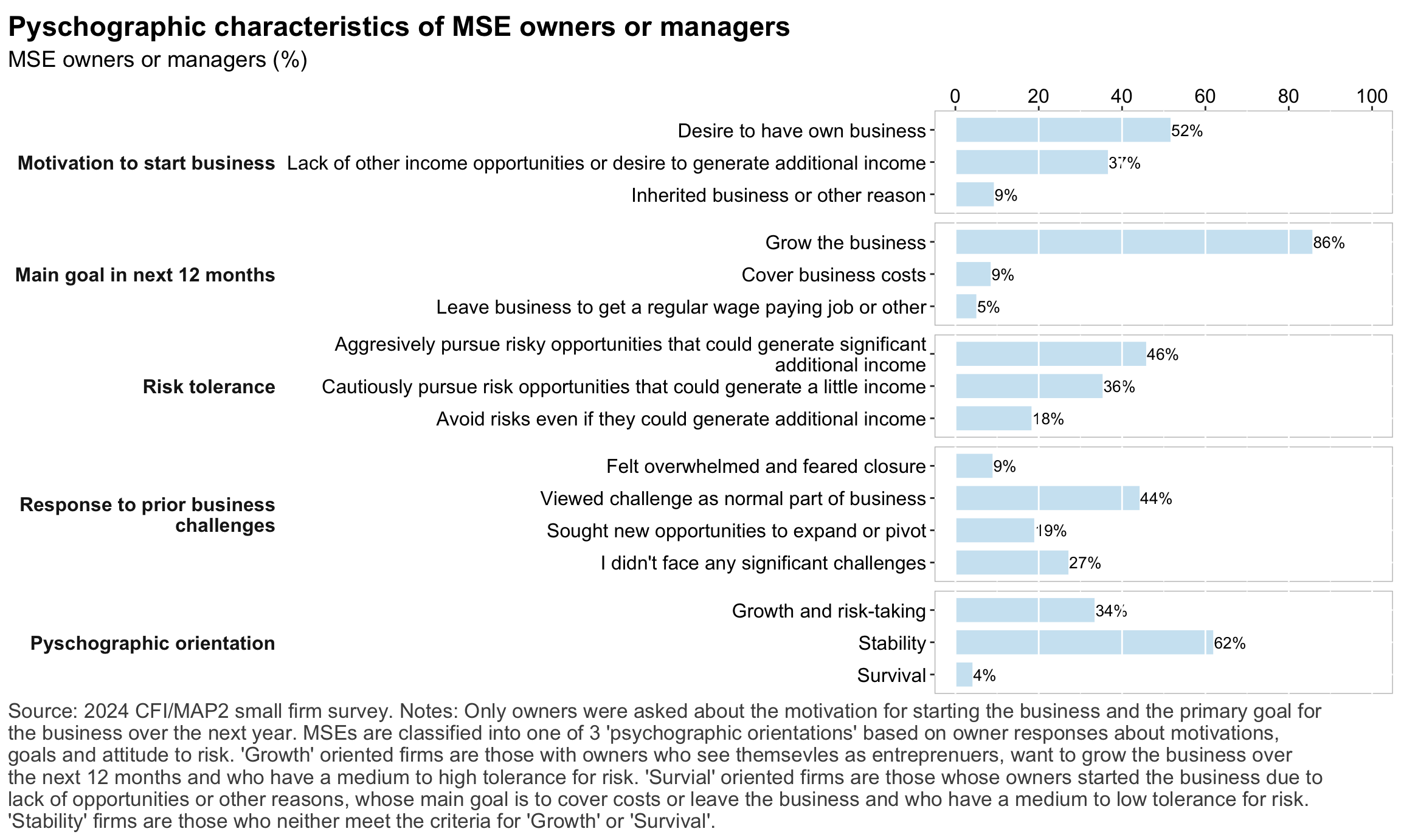

Figure 9: Pyschographic characrteristics of SME owners or managers, by gender

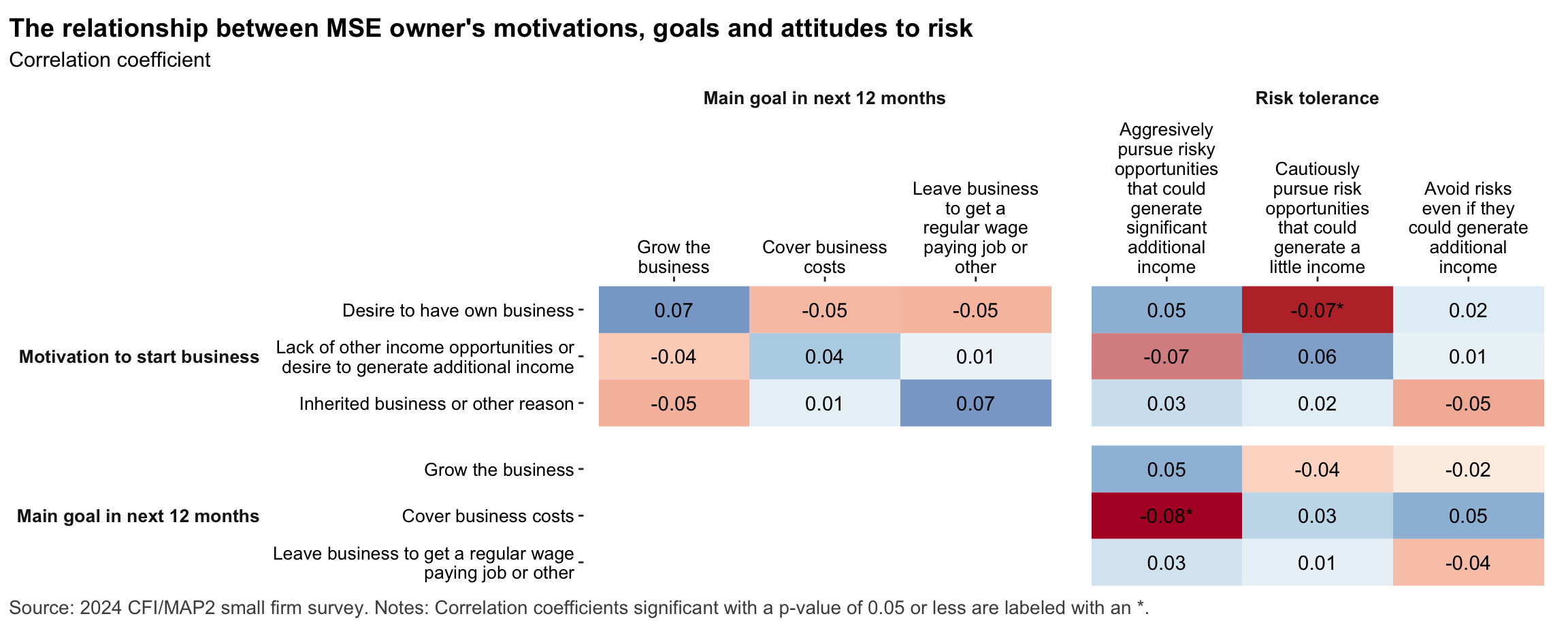

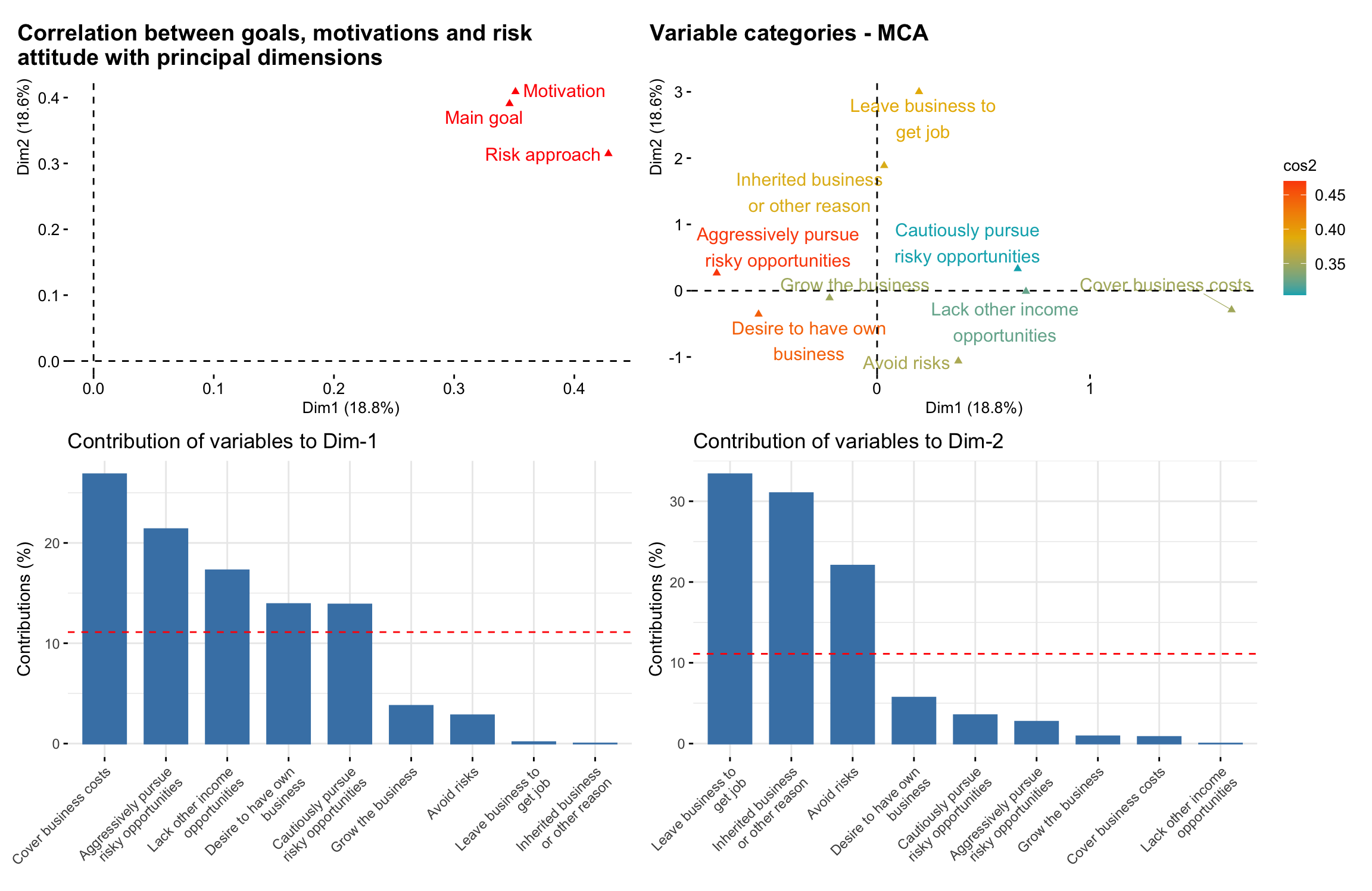

Figure 10: Correlation between owner’s motivations, goals and attitudes to risk

Figure 11: Correlation between owner’s motivations, goals and attitudes to risk

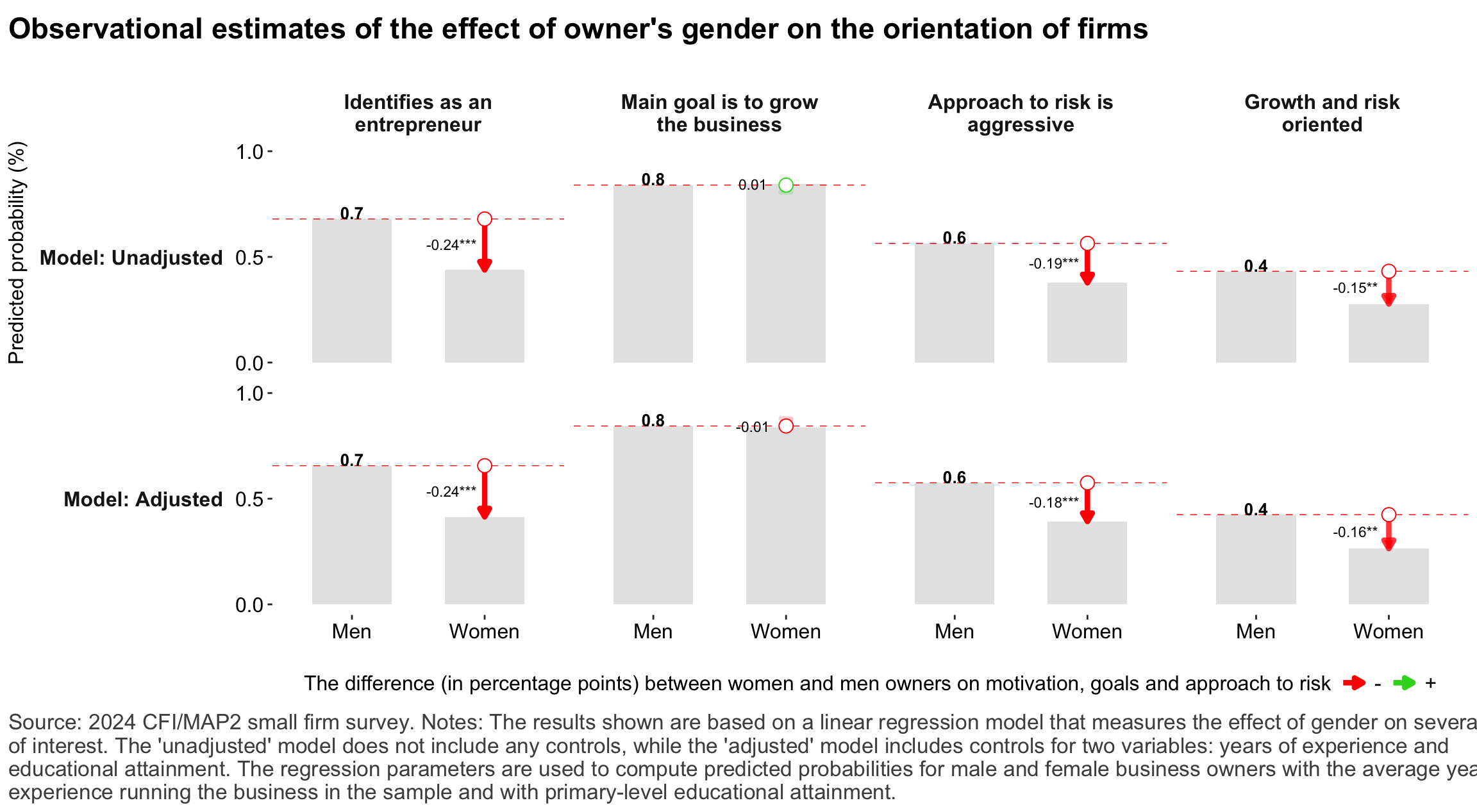

Figure 12: Relationship between owner’s gender and motivations, goals and attitudes to risk

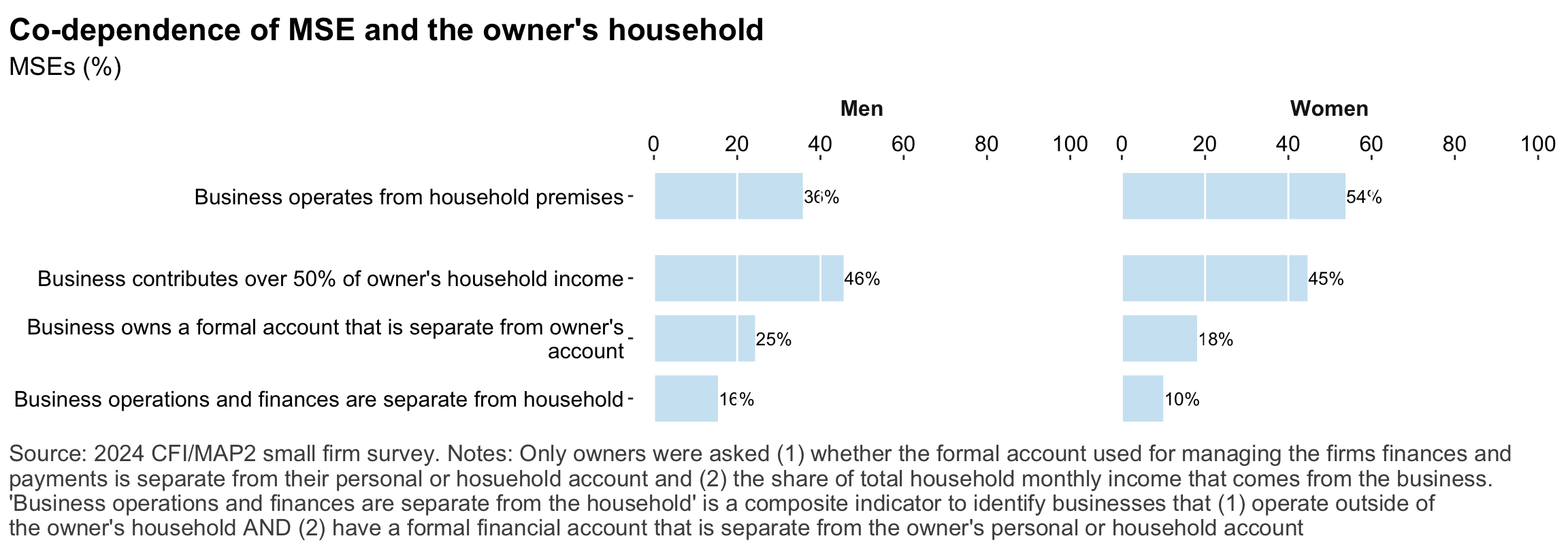

Figure 13: MSEs and codependence with owner’s household

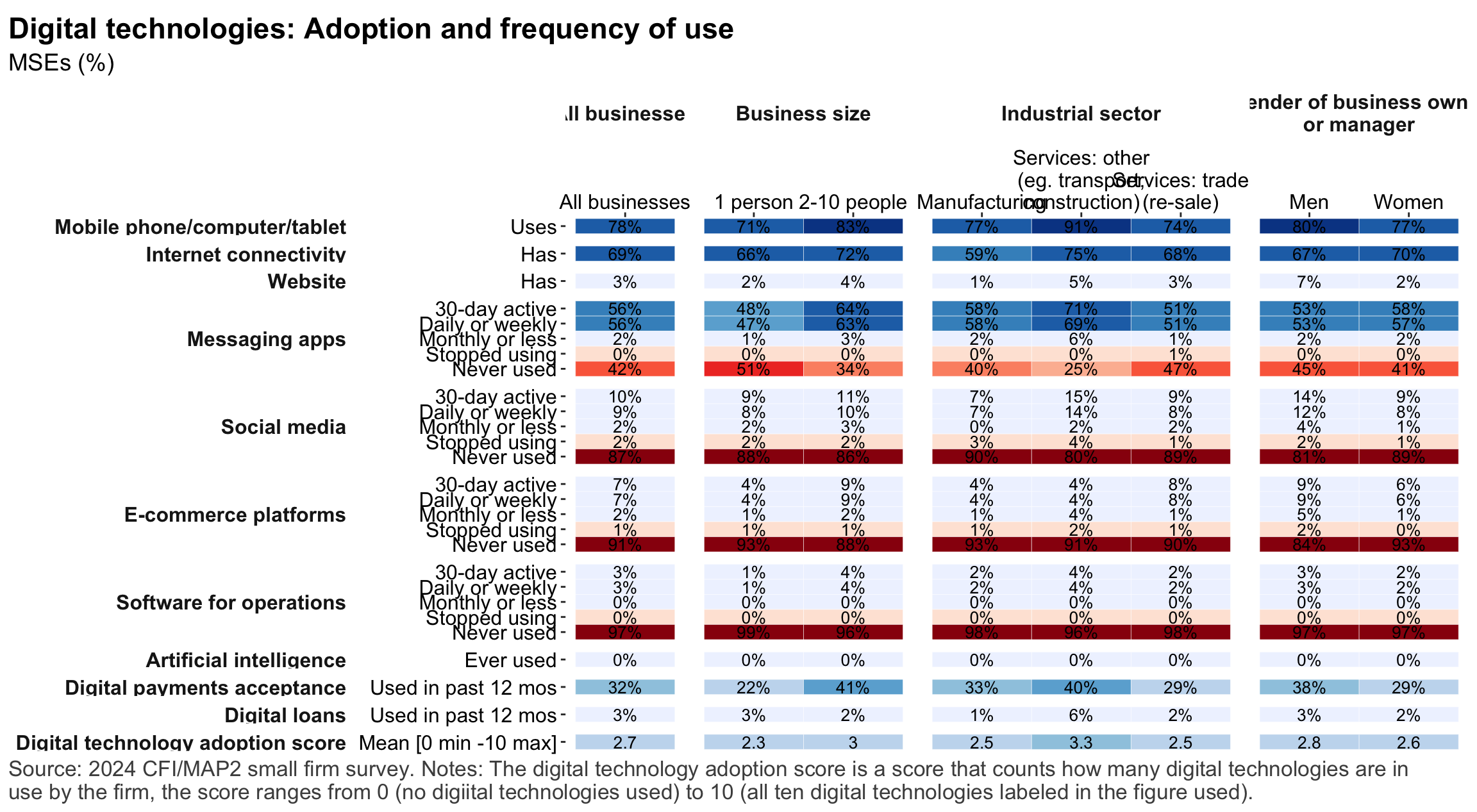

Digital technology

Figure 14: Access to connectivity and devices

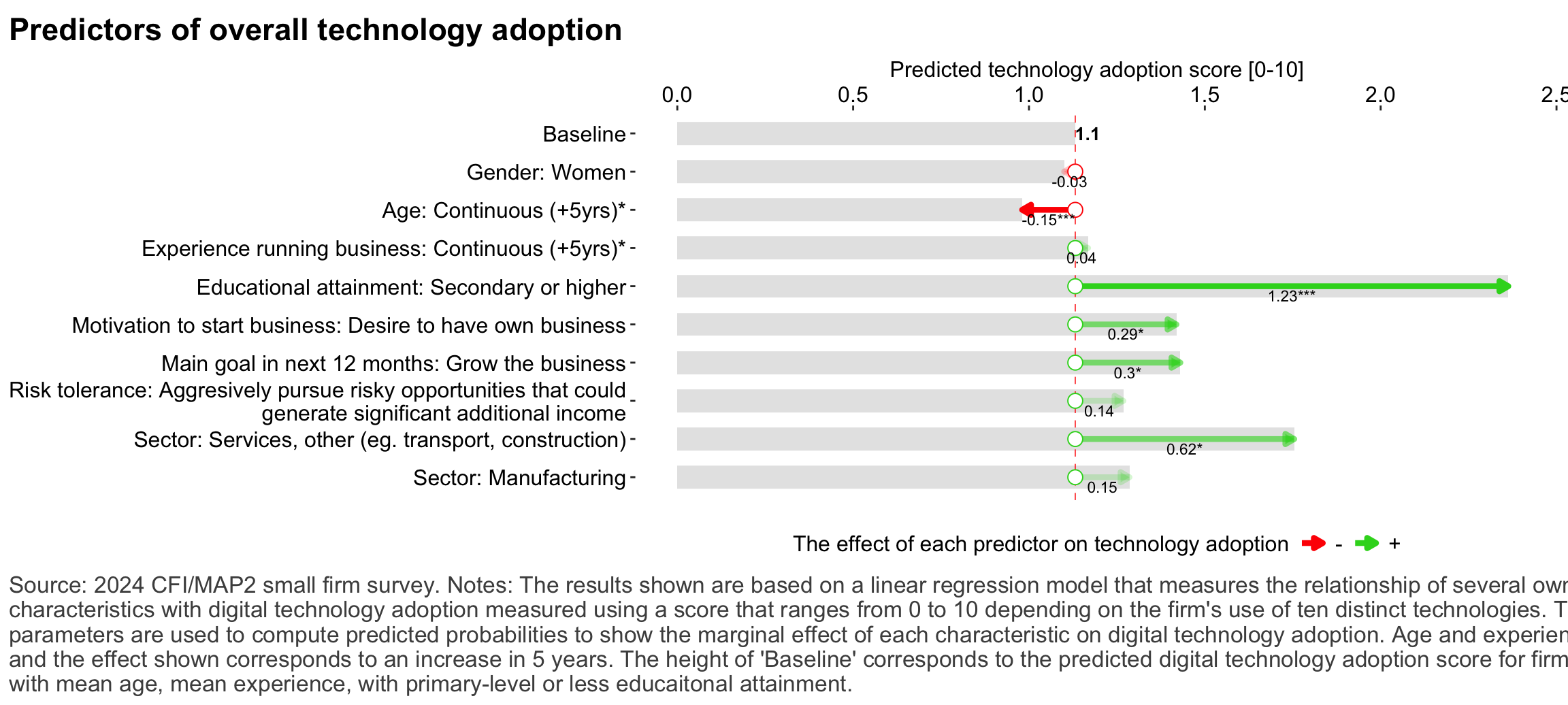

Figure 15: Predictors of digital technology adoption

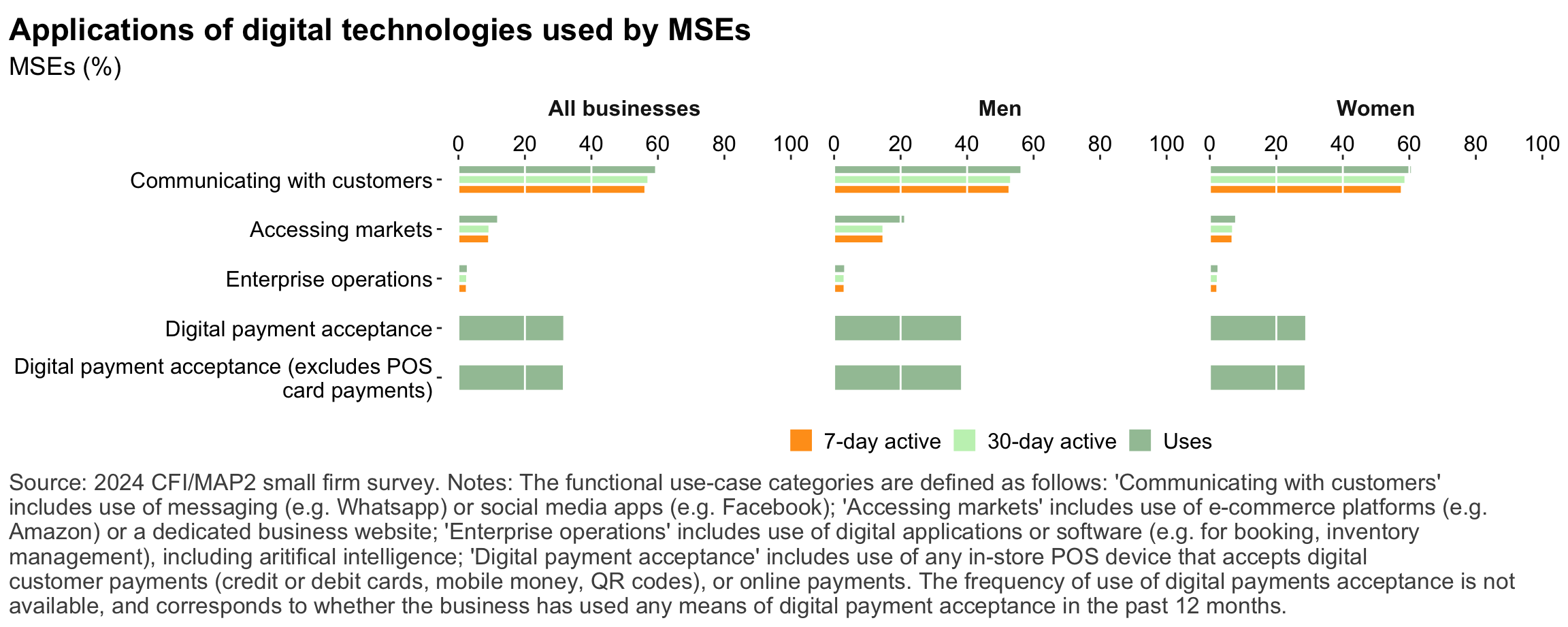

Figure 16: Digital technology adoption by use case

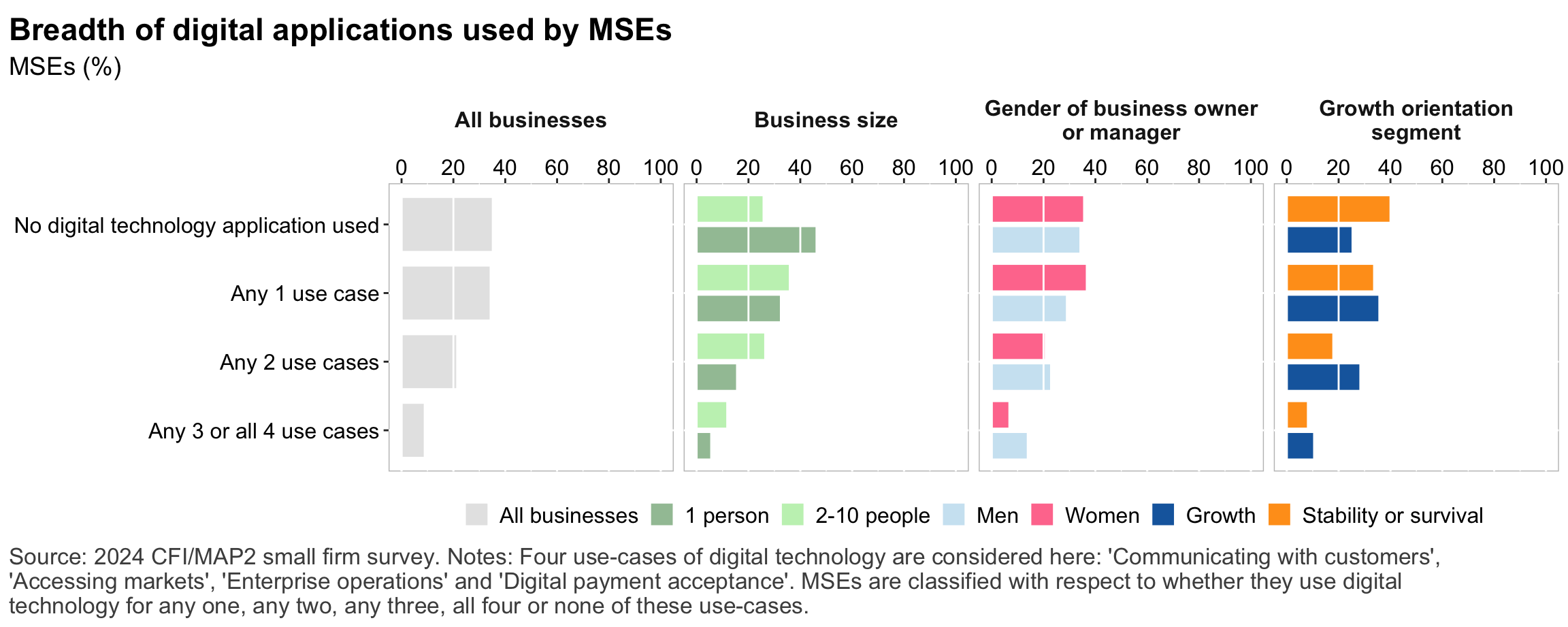

Figure 17: Depth of digital technology adoption

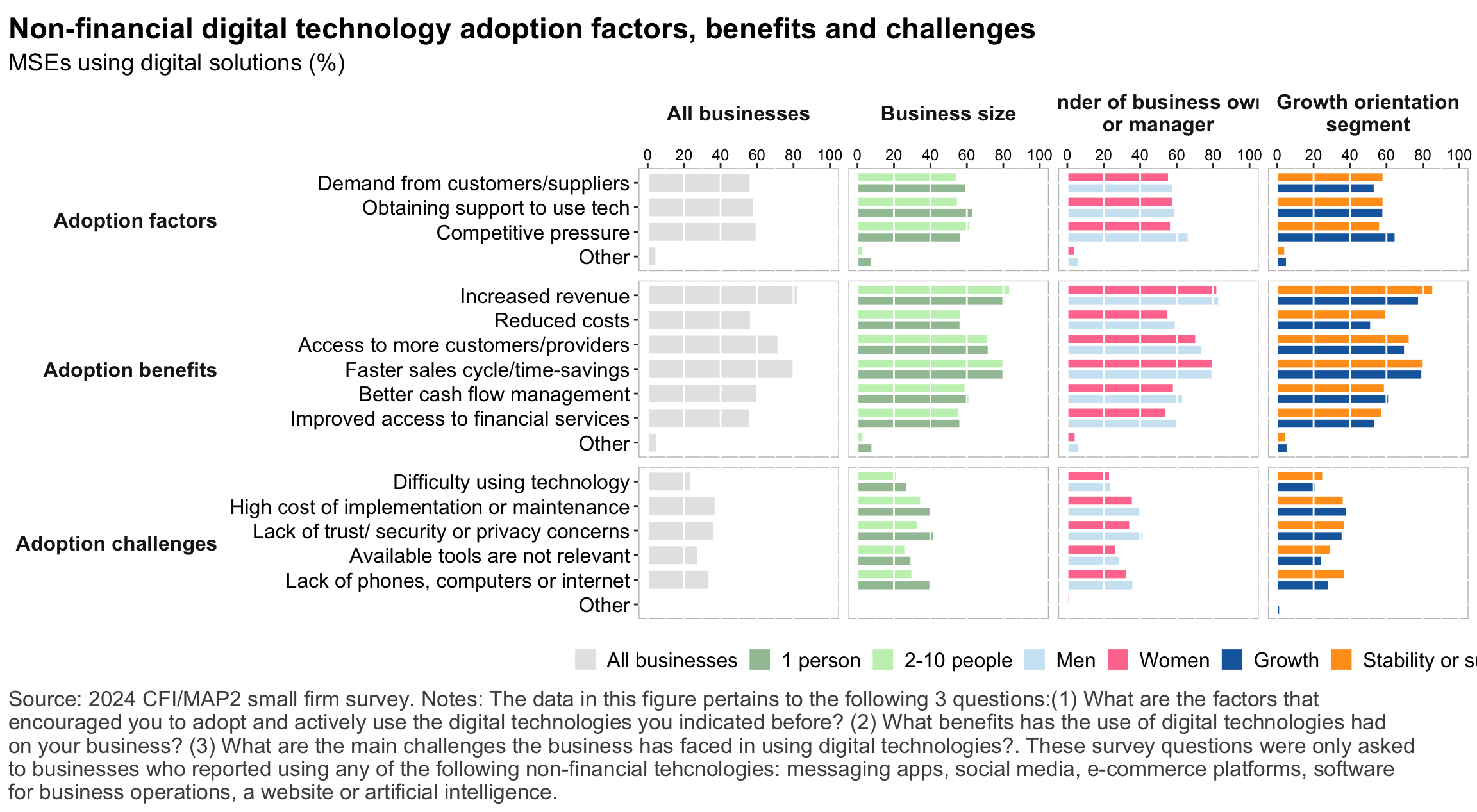

Figure 18: Digital technology adoption factors

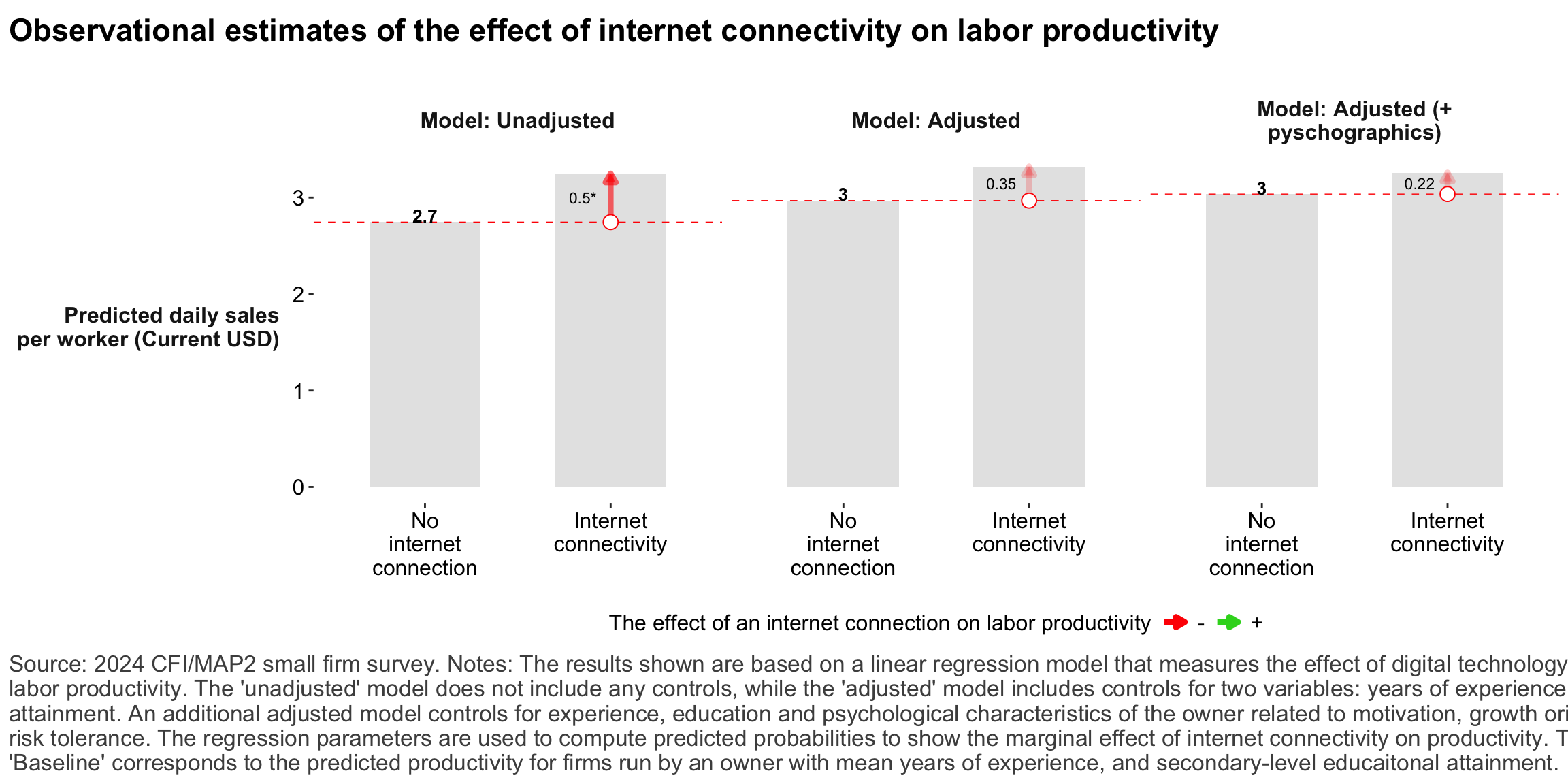

Figure 19: Relationship between internet-connectivity and firm-level labor productivity

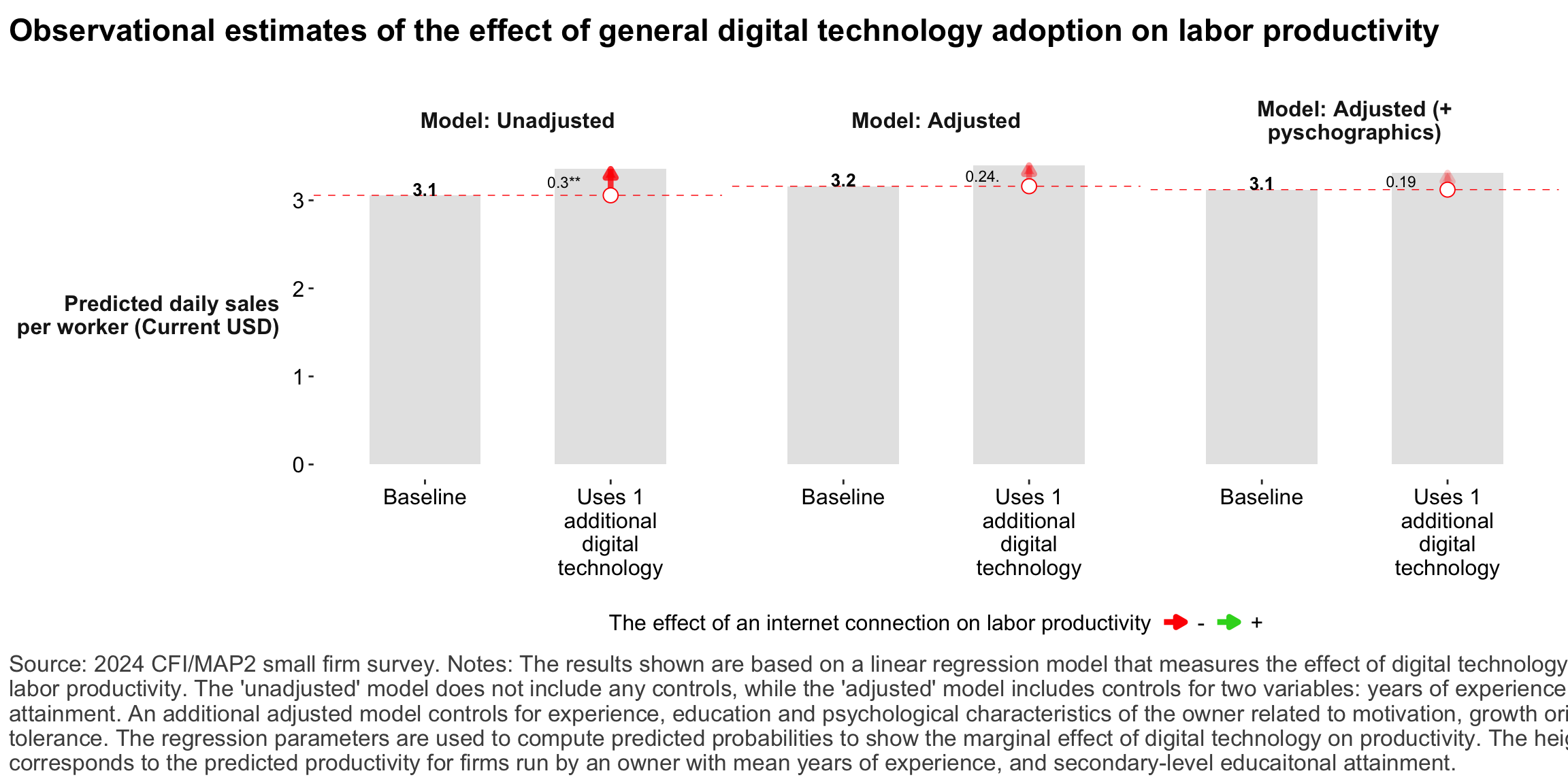

Figure 20: Relationship between digital technology and firm-level labor productivity

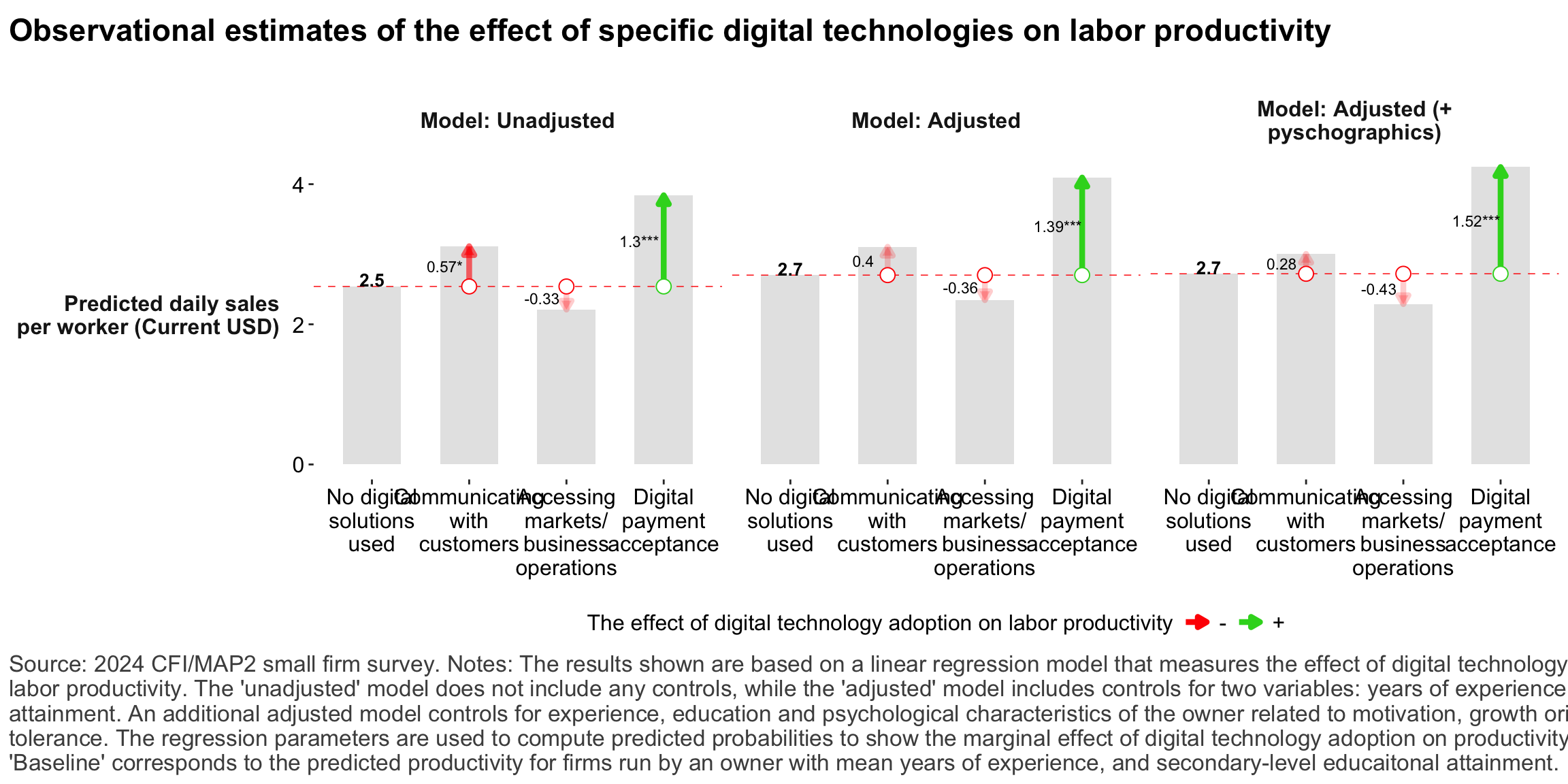

Figure 21: Relationship between digital technology adoption and firm-level labor productivity

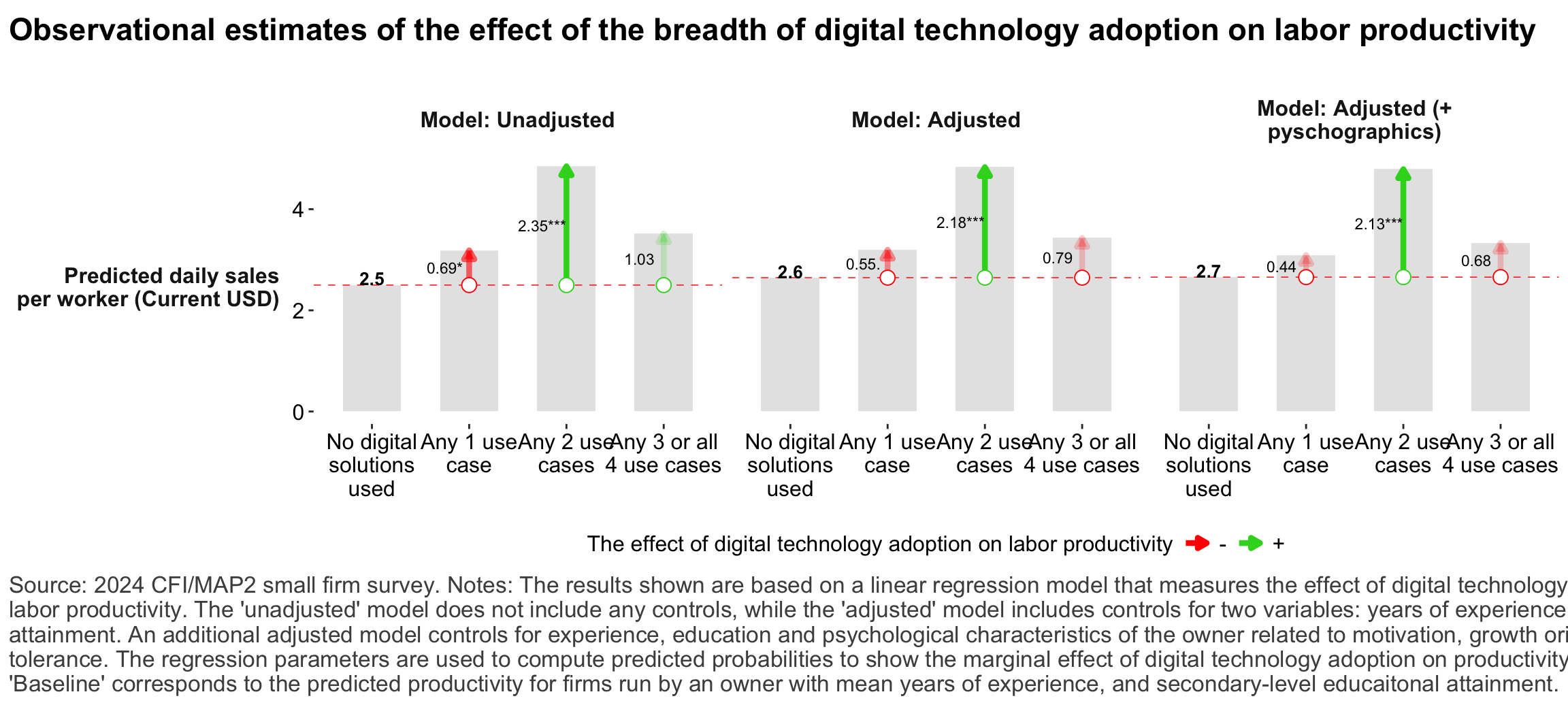

Figure 22: Relationship between breadth of digital technology adoption and firm-level labor productivity

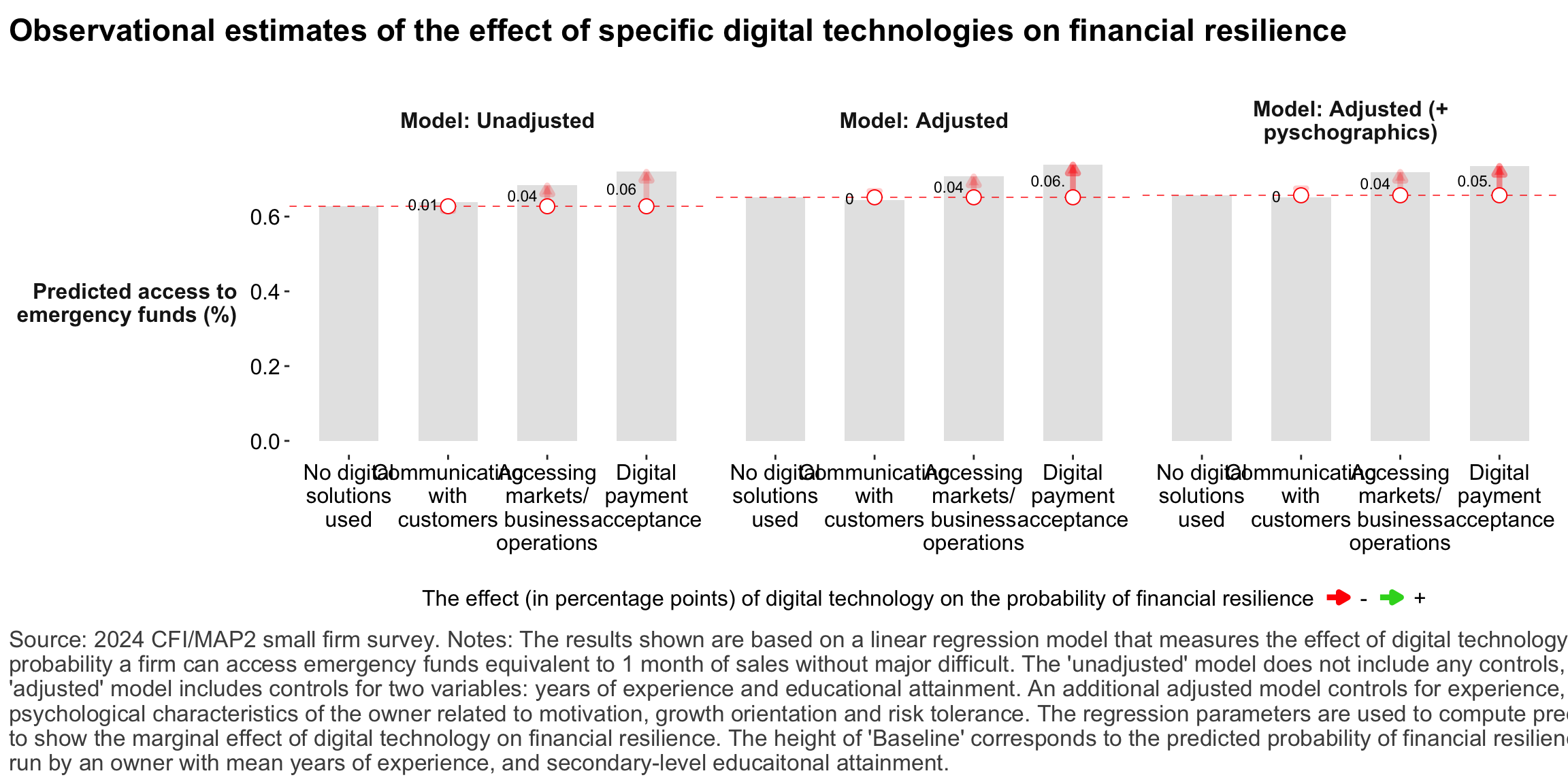

Figure 23: Relationship between digital technology and financial resilience

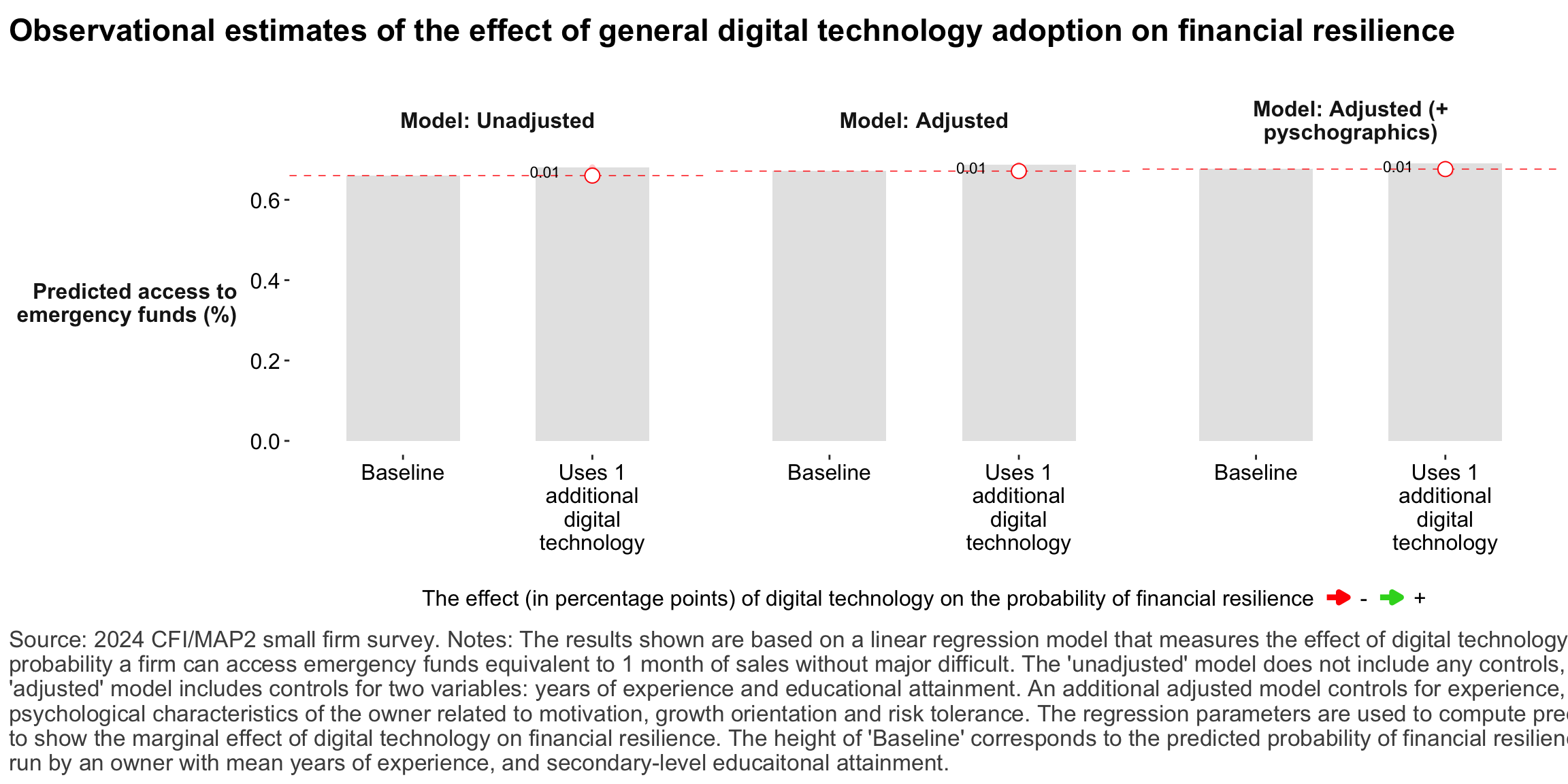

Figure 24: Relationship between digital technology adoption and financial resilience

Financial services

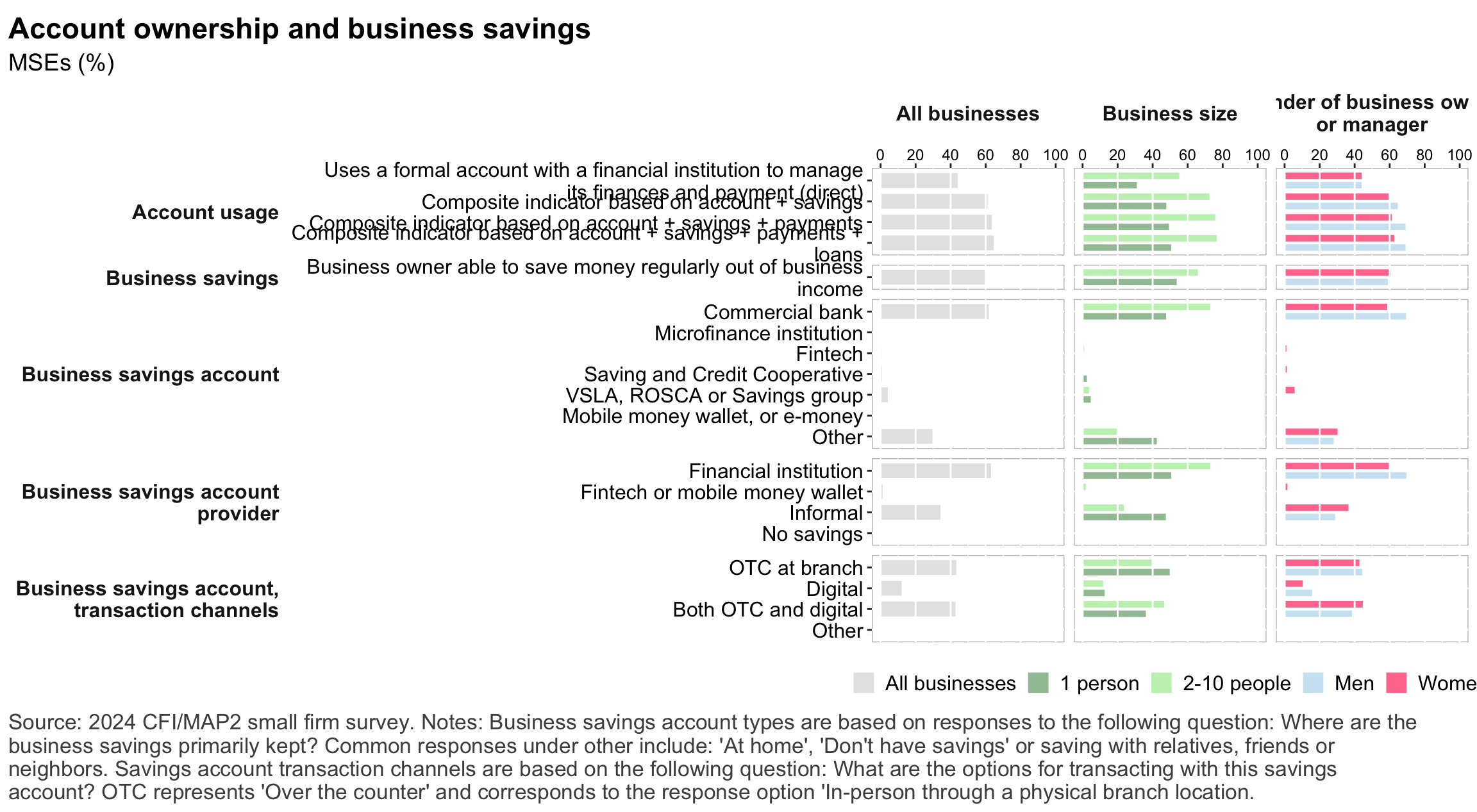

Figure 25: Financical accounts and savings

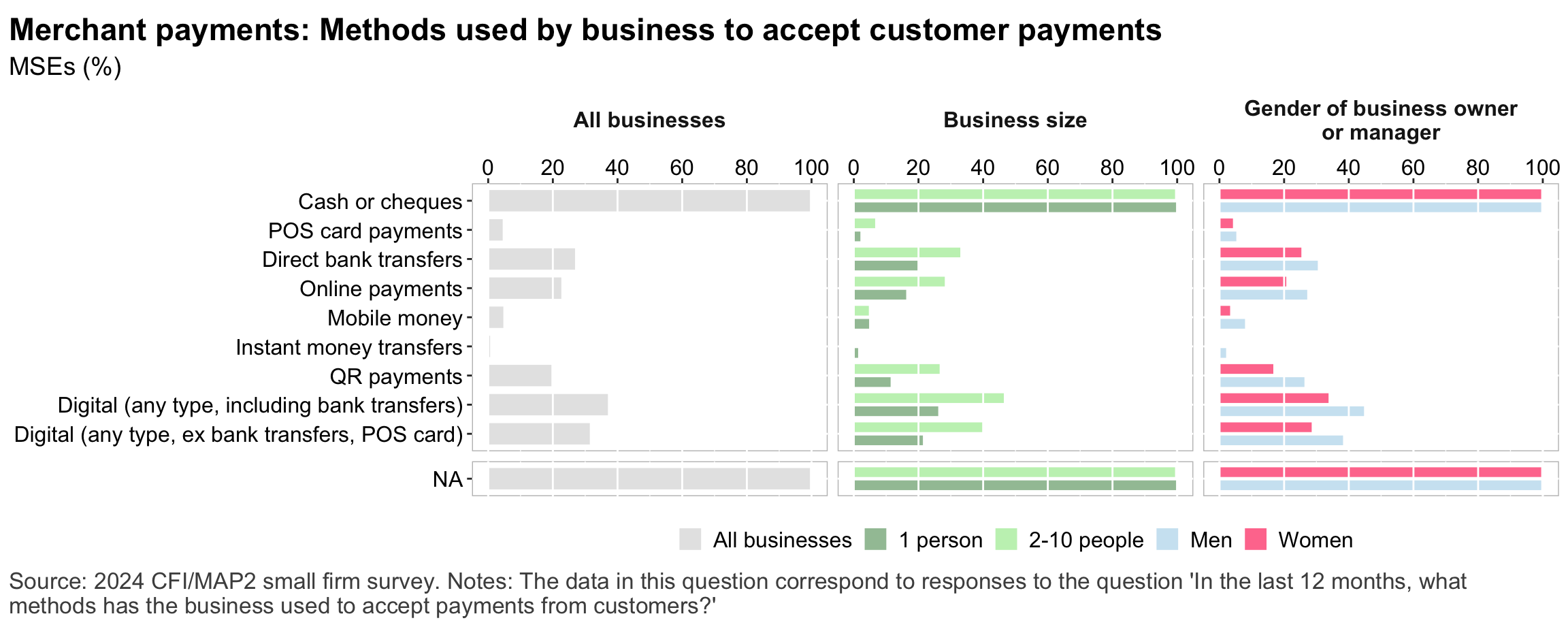

Figure 26: Merchant payments

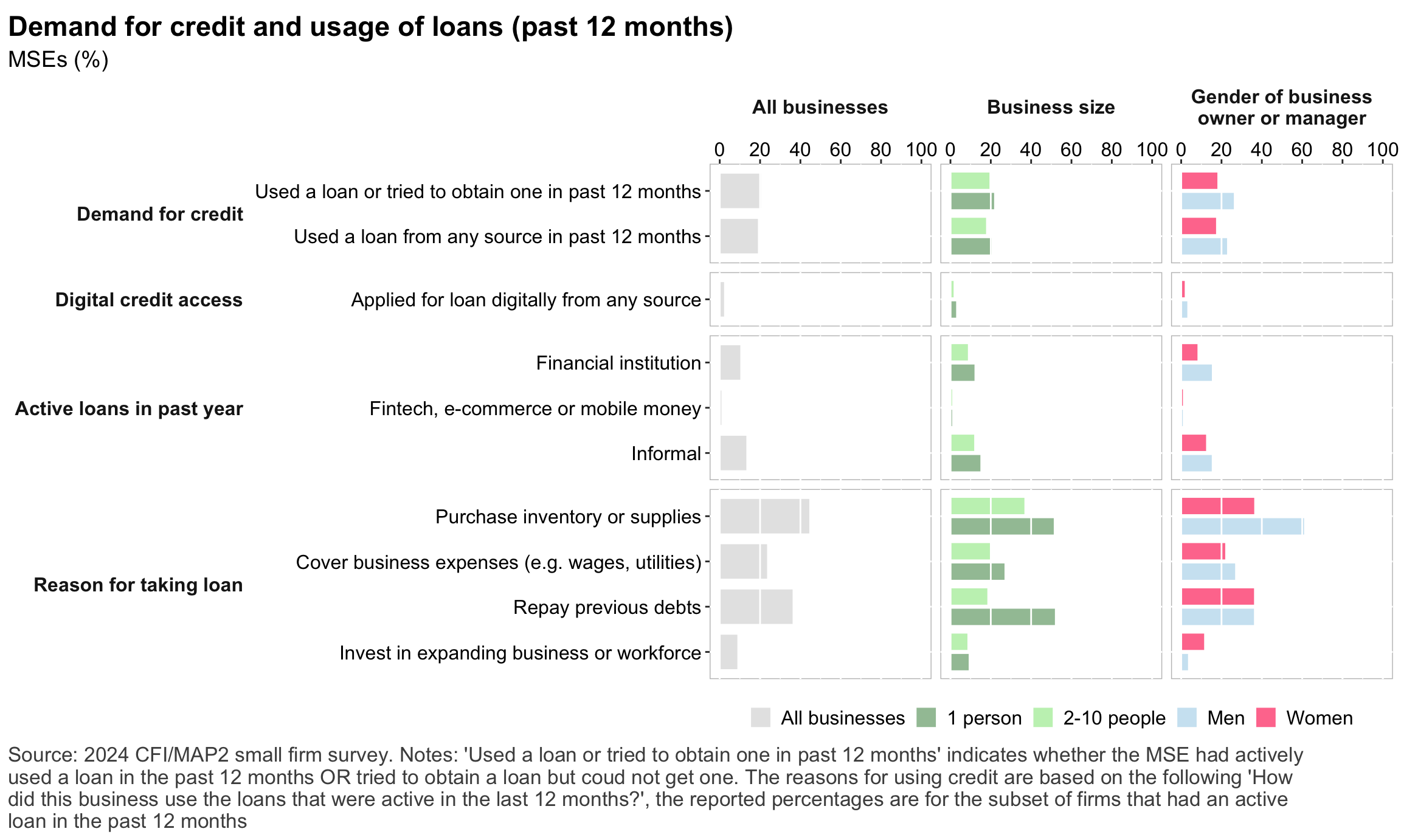

Figure 27: Demand for credit

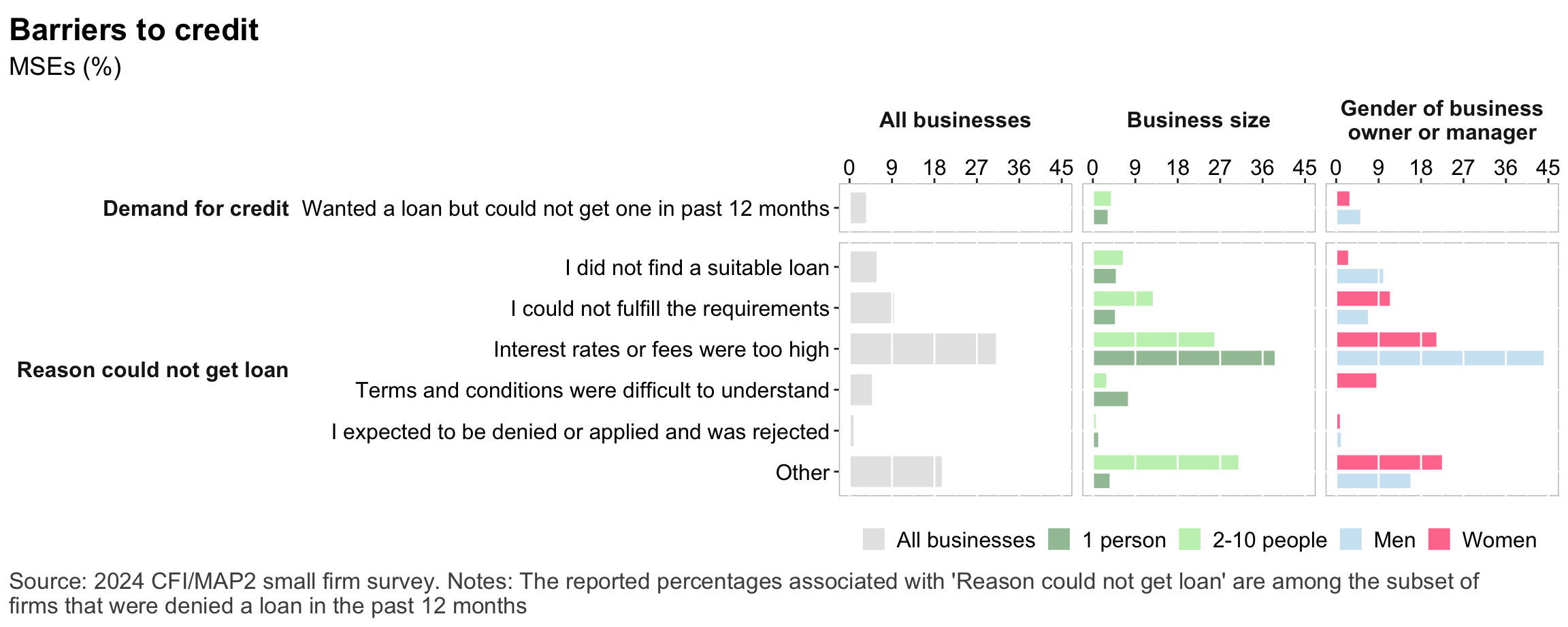

Figure 28: Barriers to credit

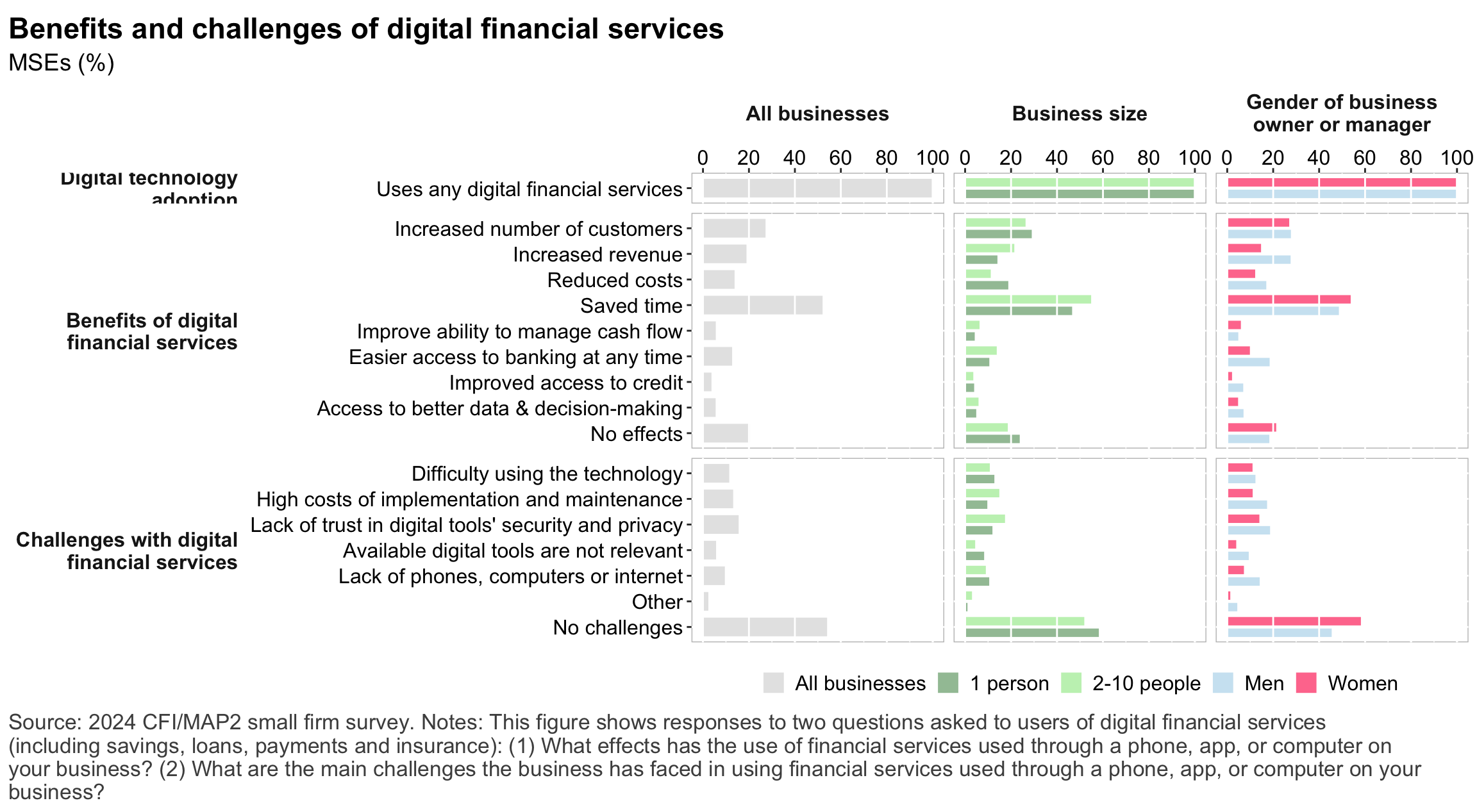

Figure 29: Impacts of digital financial services

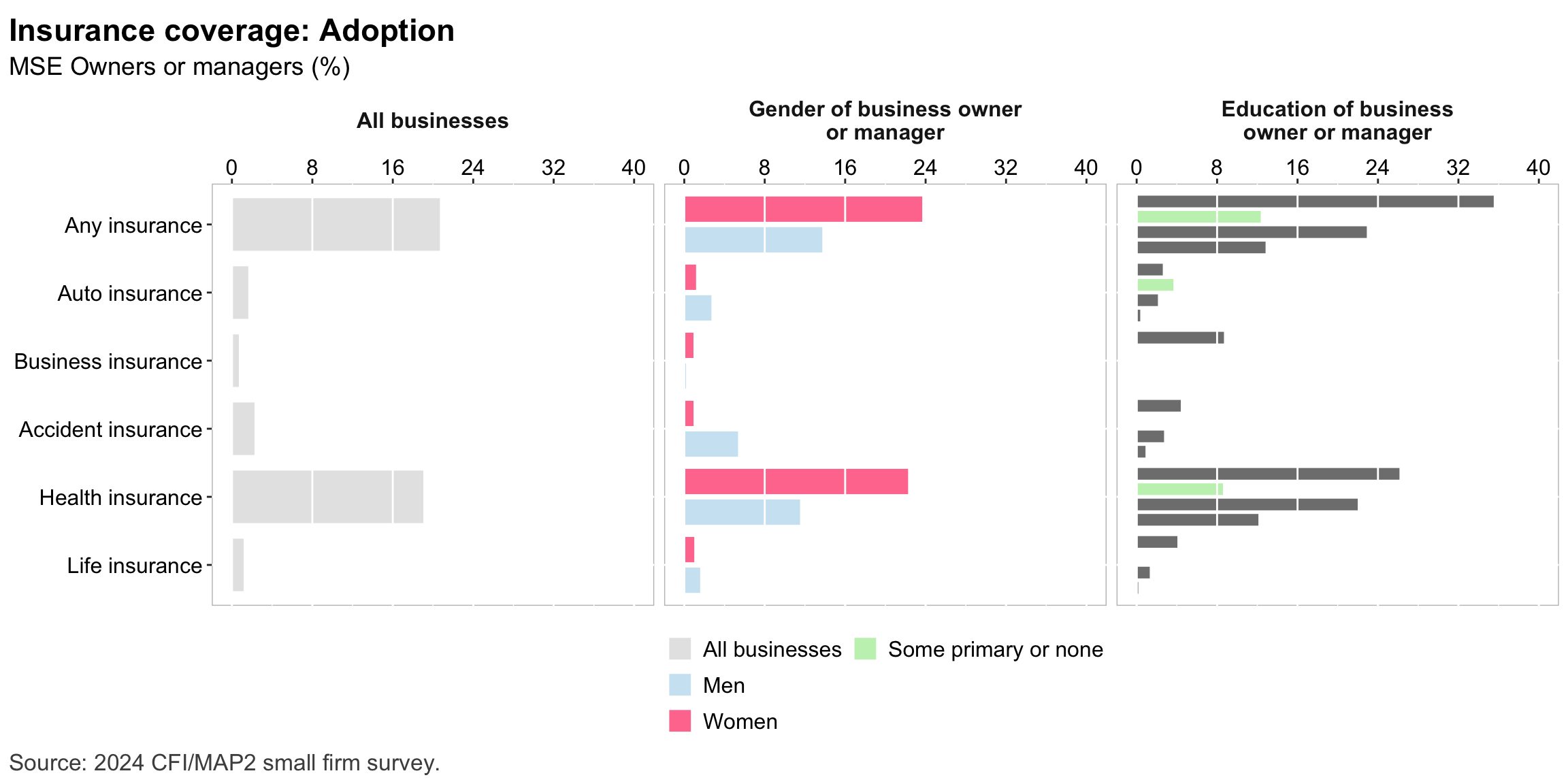

Figure 30: Insurance usage

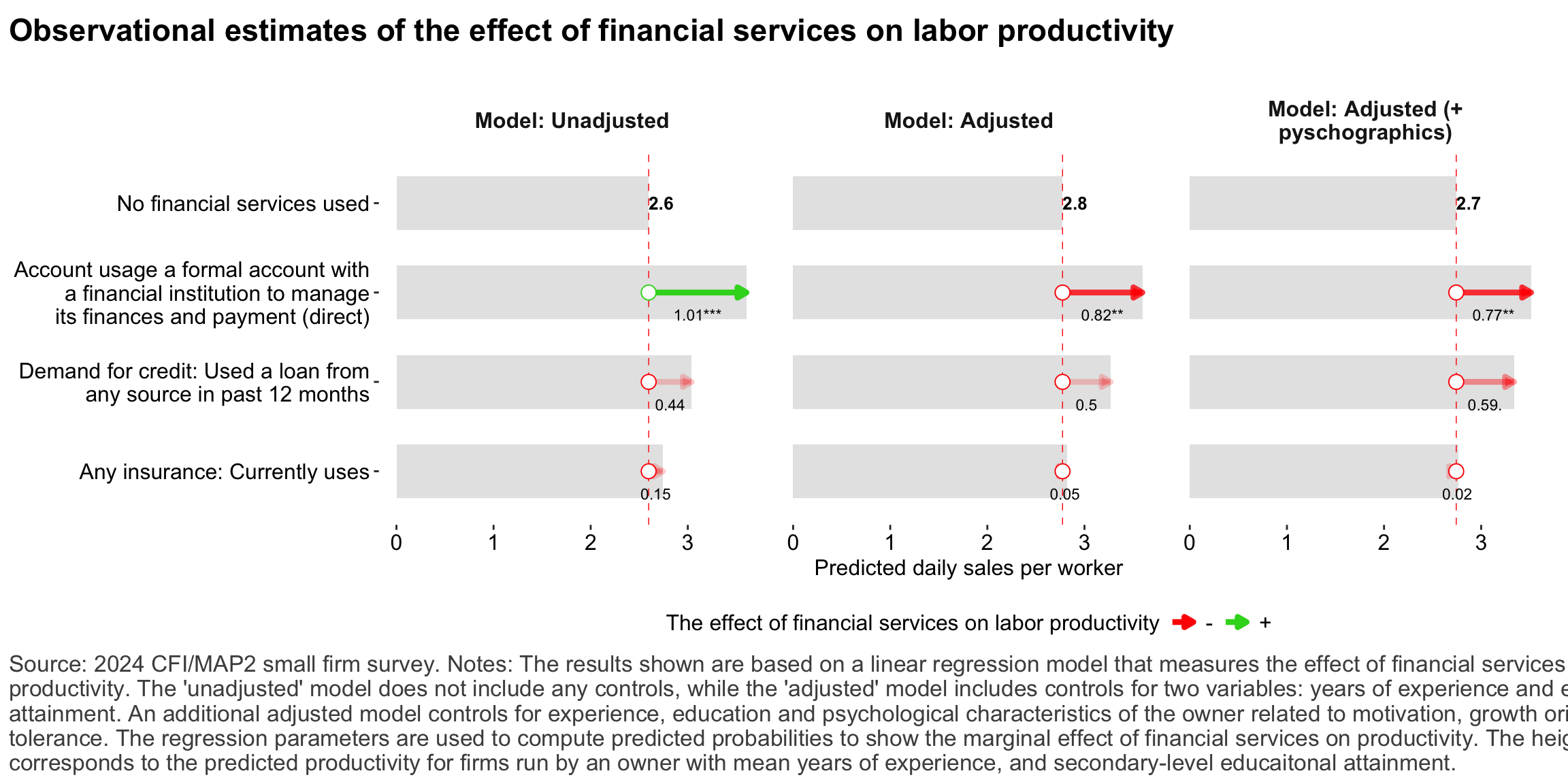

Figure 31: Relationship between financial services and firm-level labor productivity

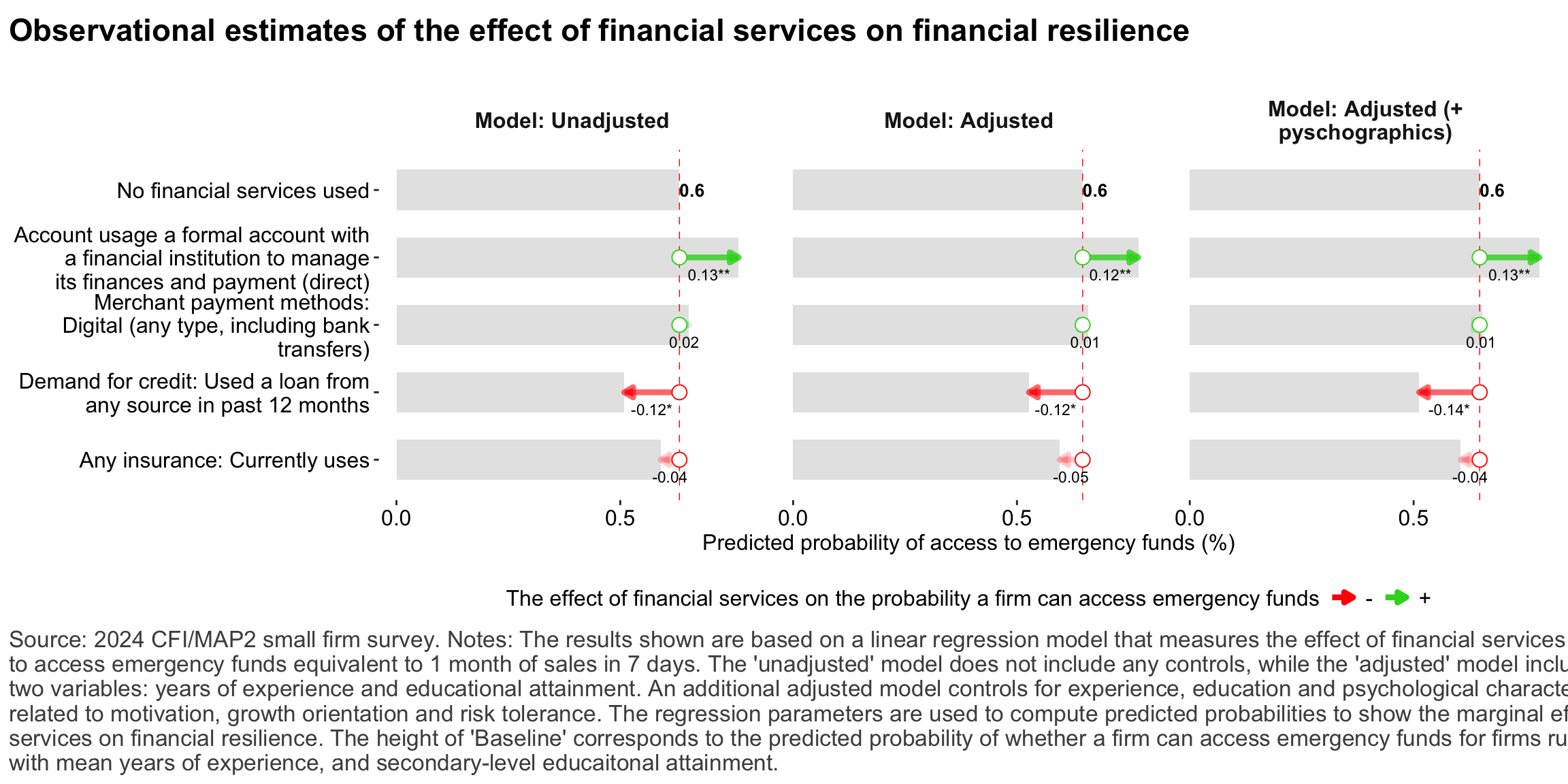

Figure 32: Relationship between financial services and financial resilience

Consumer protection

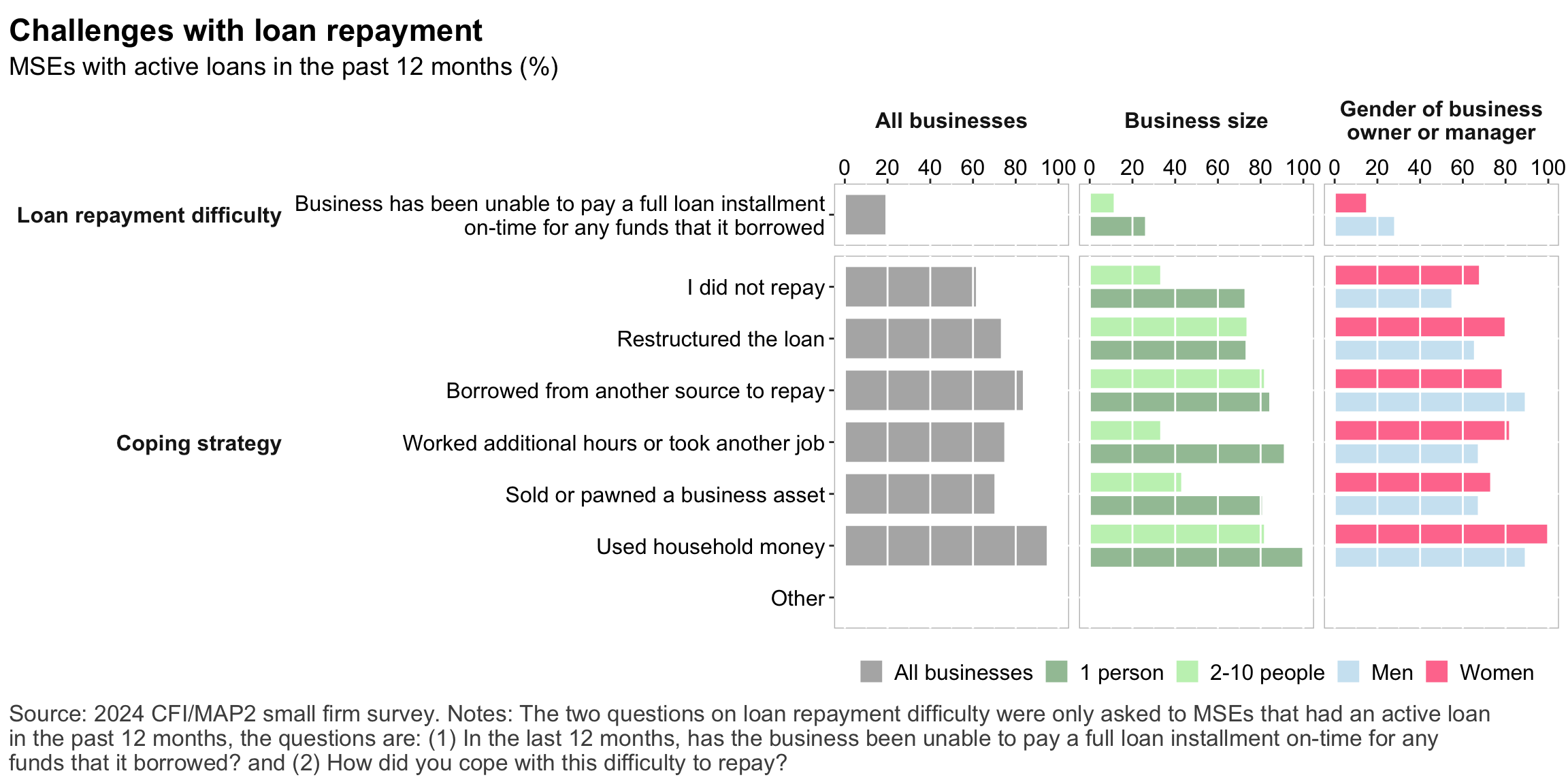

Figure 33: Challenges with loan repayment

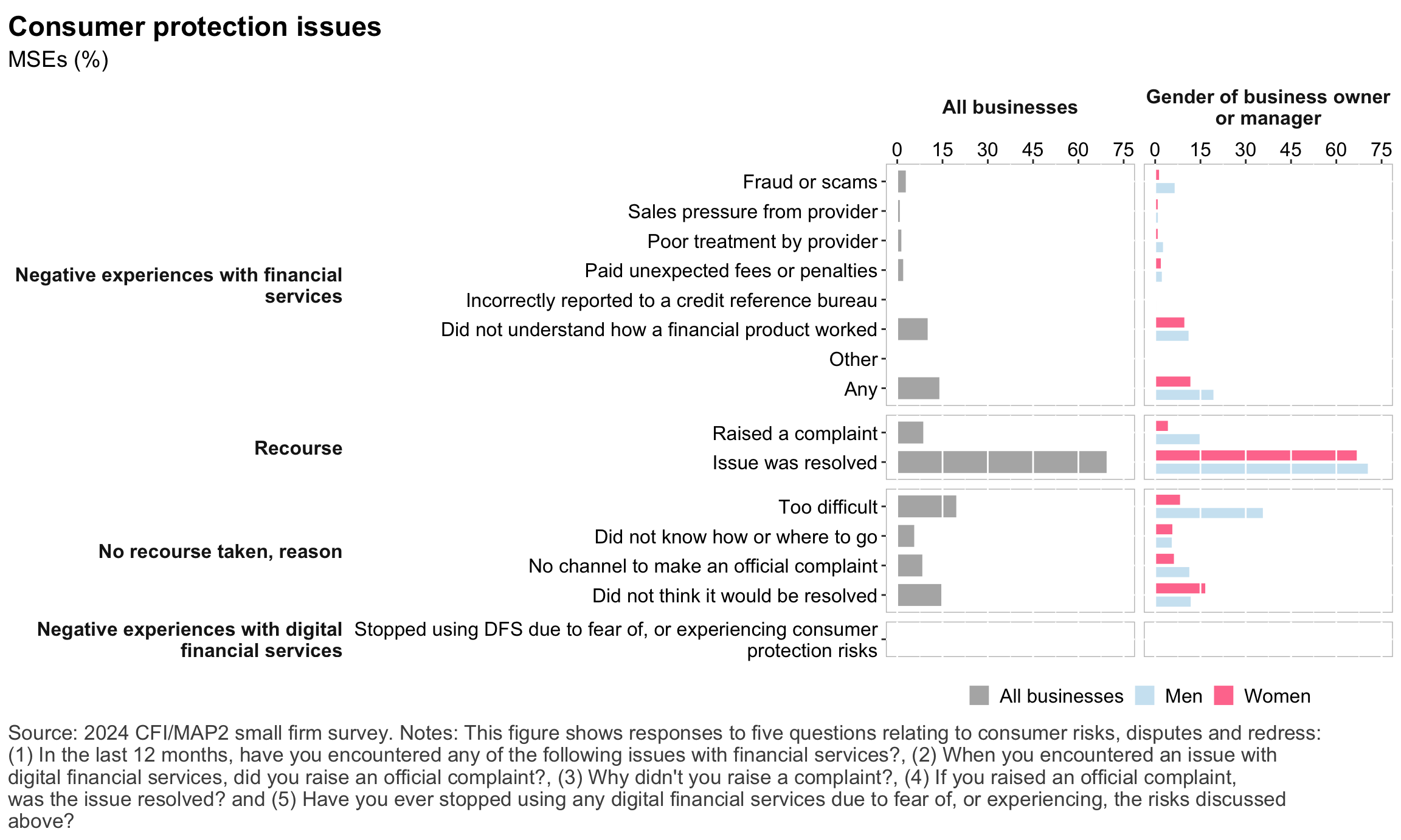

Figure 34: Consumer protection issues

Risks and Resilience

Figure 35: Risks: General

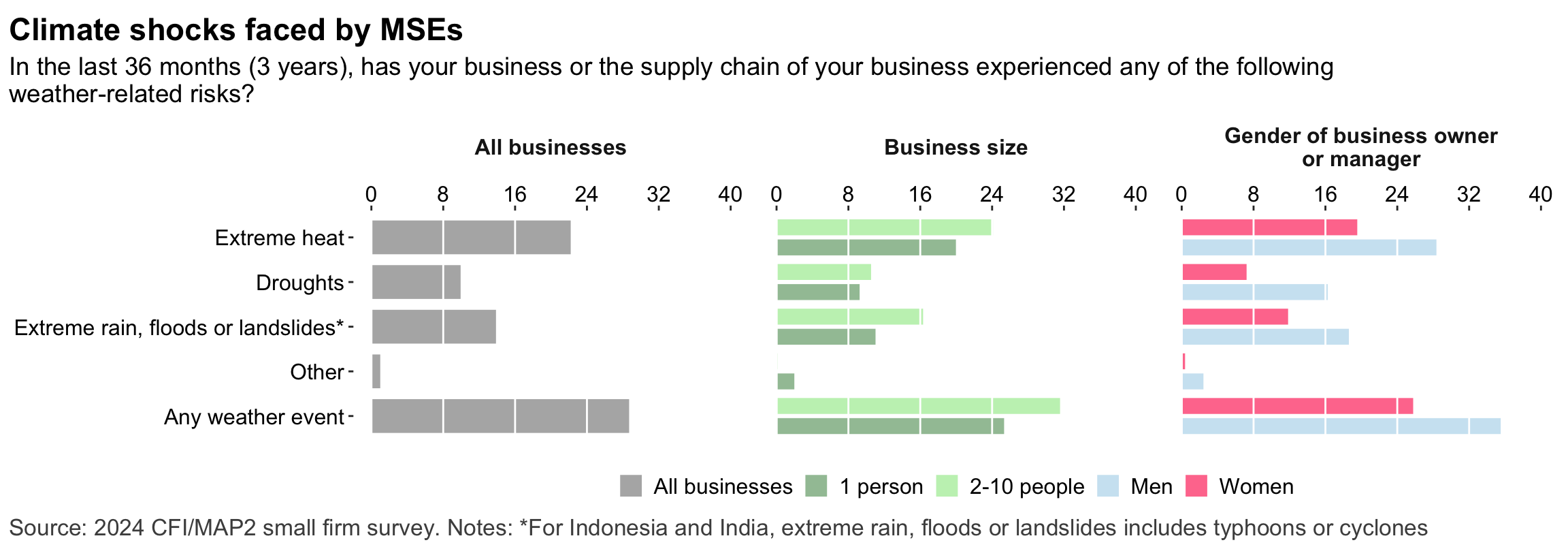

Figure 36: Risks: Climate

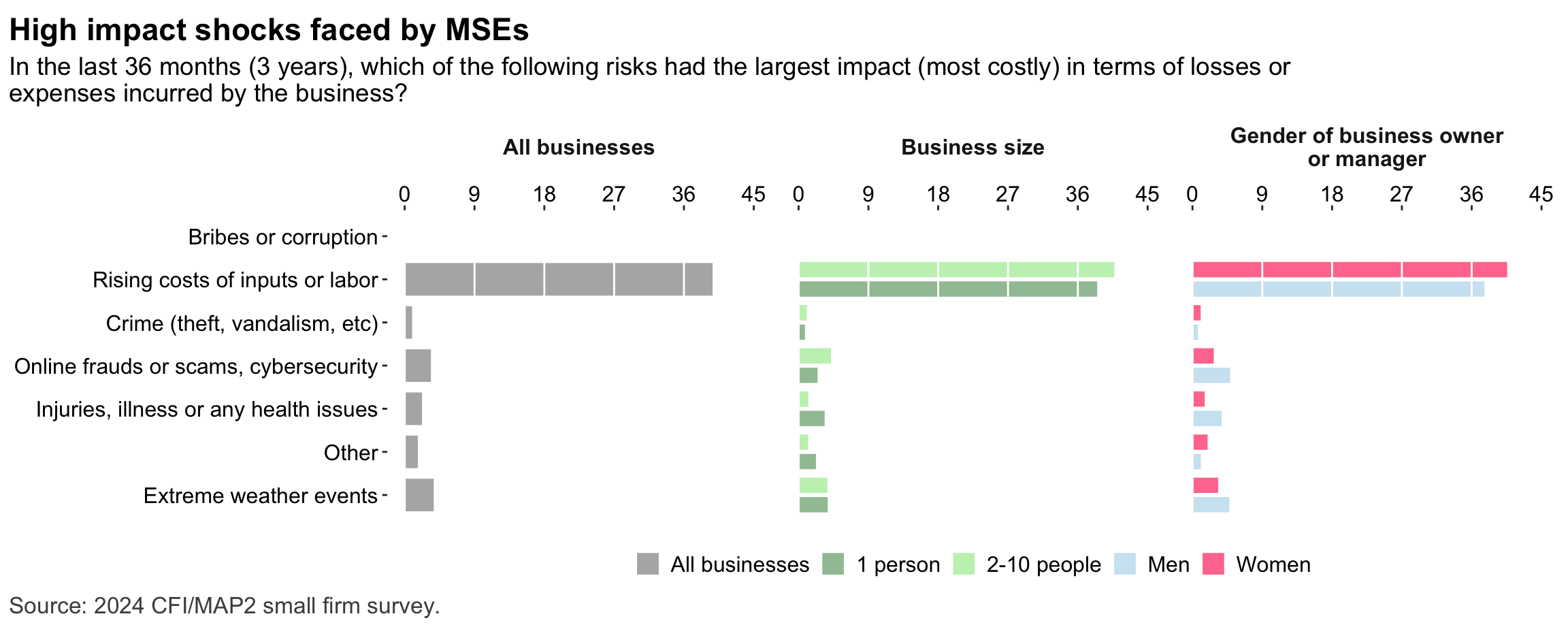

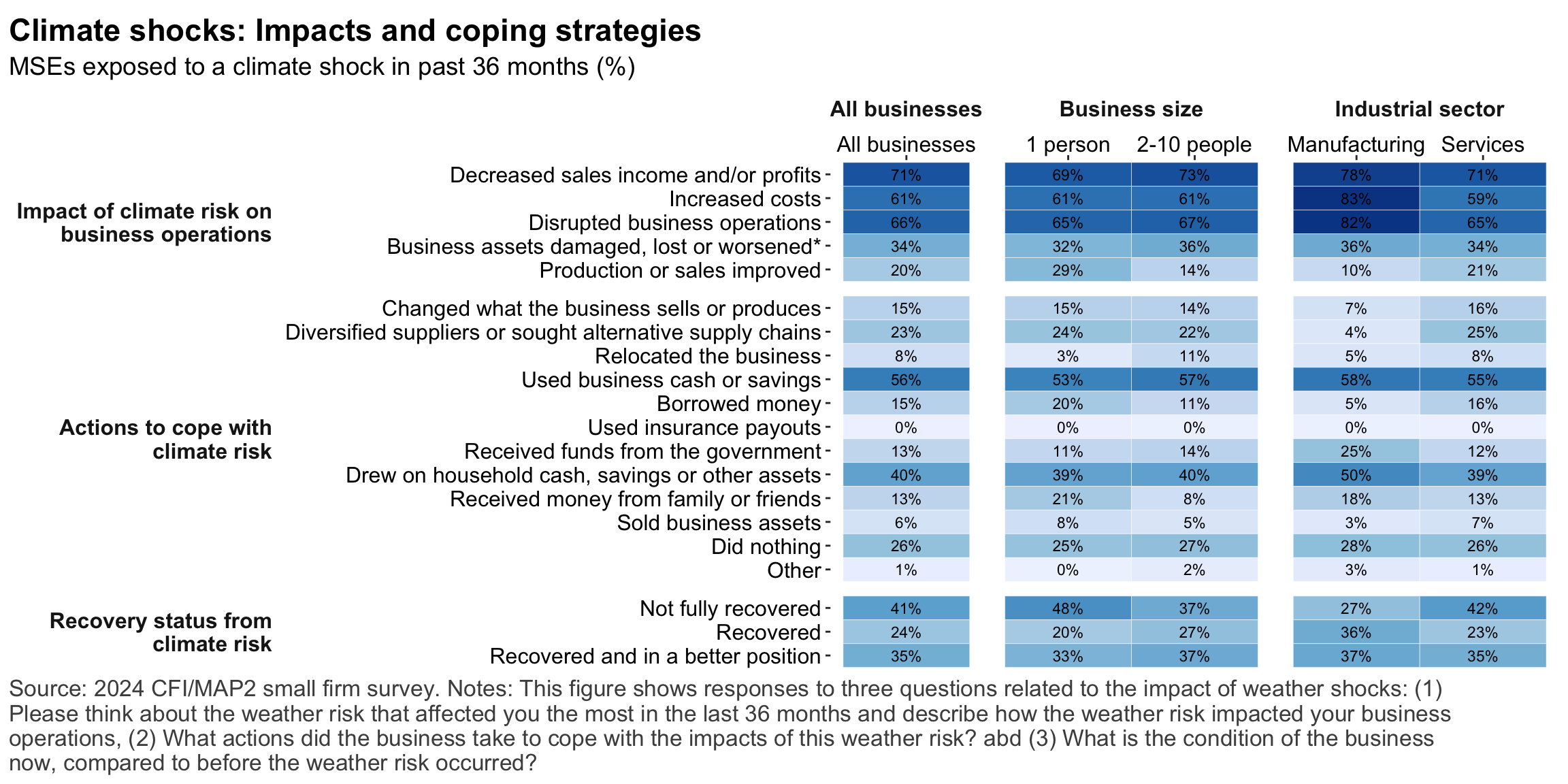

Figure 37: Risks: Impacts

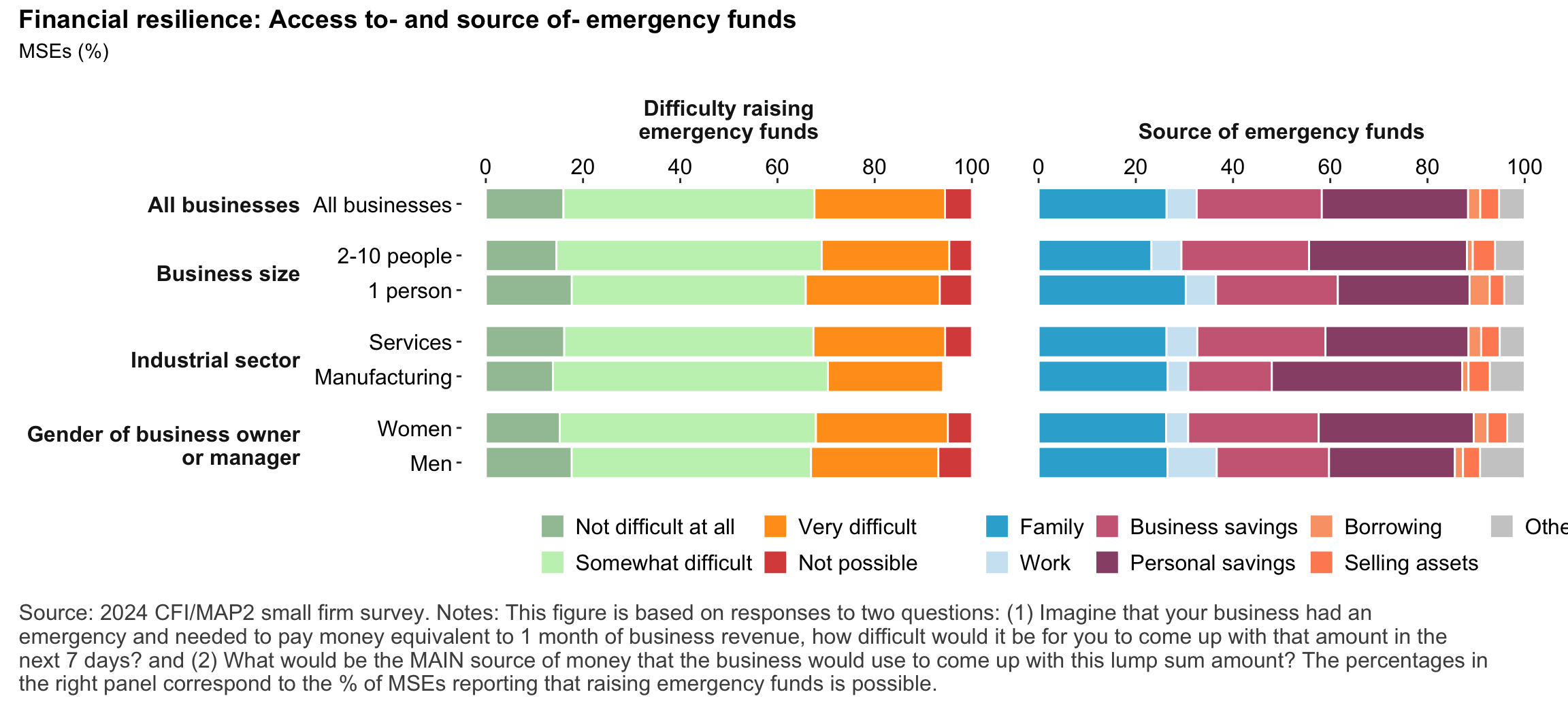

Figure 38: Financial resilience

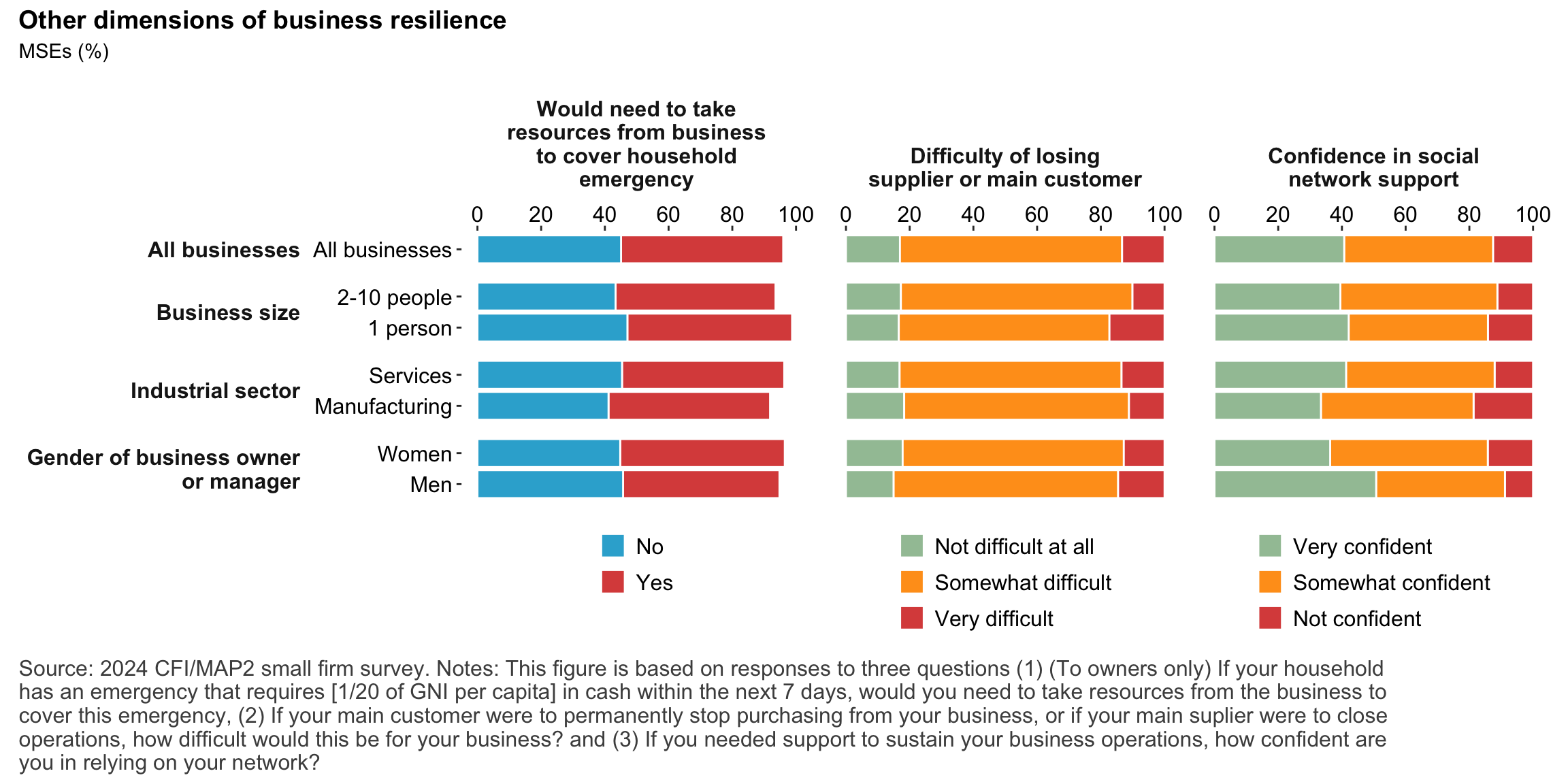

Figure 39: Other dimensions of business resilience

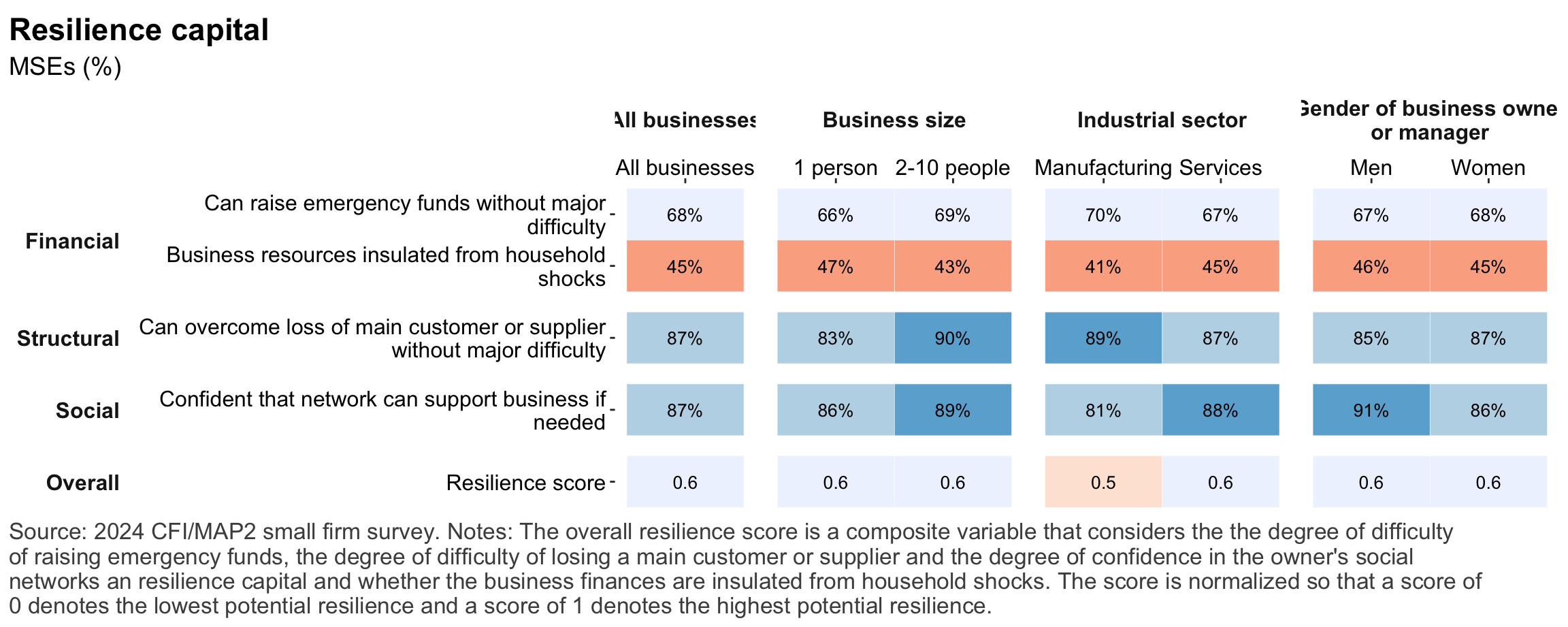

Figure 40: Resilience capital

Figure 1: Geographic distribution of enumerated blocksFigure 2: Estimated business population by size and sectorFigure 3: MSE sample characteristicsFigure 4: MSEs by sector of productionFigure 5: MSE revenues and productivityFigure 6: Changes in MSE outcomes in past yearFigure 7: Gender composition of MSEs by sise and sectorFigure 8: MSE owner characteristicsFigure 9: Pyschographic characrteristics of SME owners or managers, by genderFigure 10: Correlation between owner’s motivations, goals and attitudes to riskFigure 11: Correlation between owner’s motivations, goals and attitudes to riskFigure 12: Relationship between owner’s gender and motivations, goals and attitudes to riskFigure 13: MSEs and codependence with owner’s householdFigure 14: Access to connectivity and devicesFigure 15: Predictors of digital technology adoptionFigure 16: Digital technology adoption by use caseFigure 17: Depth of digital technology adoptionFigure 18: Digital technology adoption factorsFigure 19: Relationship between internet-connectivity and firm-level labor productivityFigure 20: Relationship between digital technology and firm-level labor productivityFigure 21: Relationship between digital technology adoption and firm-level labor productivityFigure 22: Relationship between breadth of digital technology adoption and firm-level labor productivityFigure 23: Relationship between digital technology and financial resilienceFigure 24: Relationship between digital technology adoption and financial resilienceFigure 25: Financical accounts and savingsFigure 26: Merchant paymentsFigure 27: Demand for creditFigure 28: Barriers to creditFigure 29: Impacts of digital financial servicesFigure 30: Insurance usageFigure 31: Relationship between financial services and firm-level labor productivityFigure 32: Relationship between financial services and financial resilienceFigure 33: Challenges with loan repaymentFigure 34: Consumer protection issuesFigure 35: Risks: GeneralFigure 36: Risks: ClimateFigure 37: Risks: ImpactsFigure 38: Financial resilienceFigure 39: Other dimensions of business resilienceFigure 40: Resilience capital