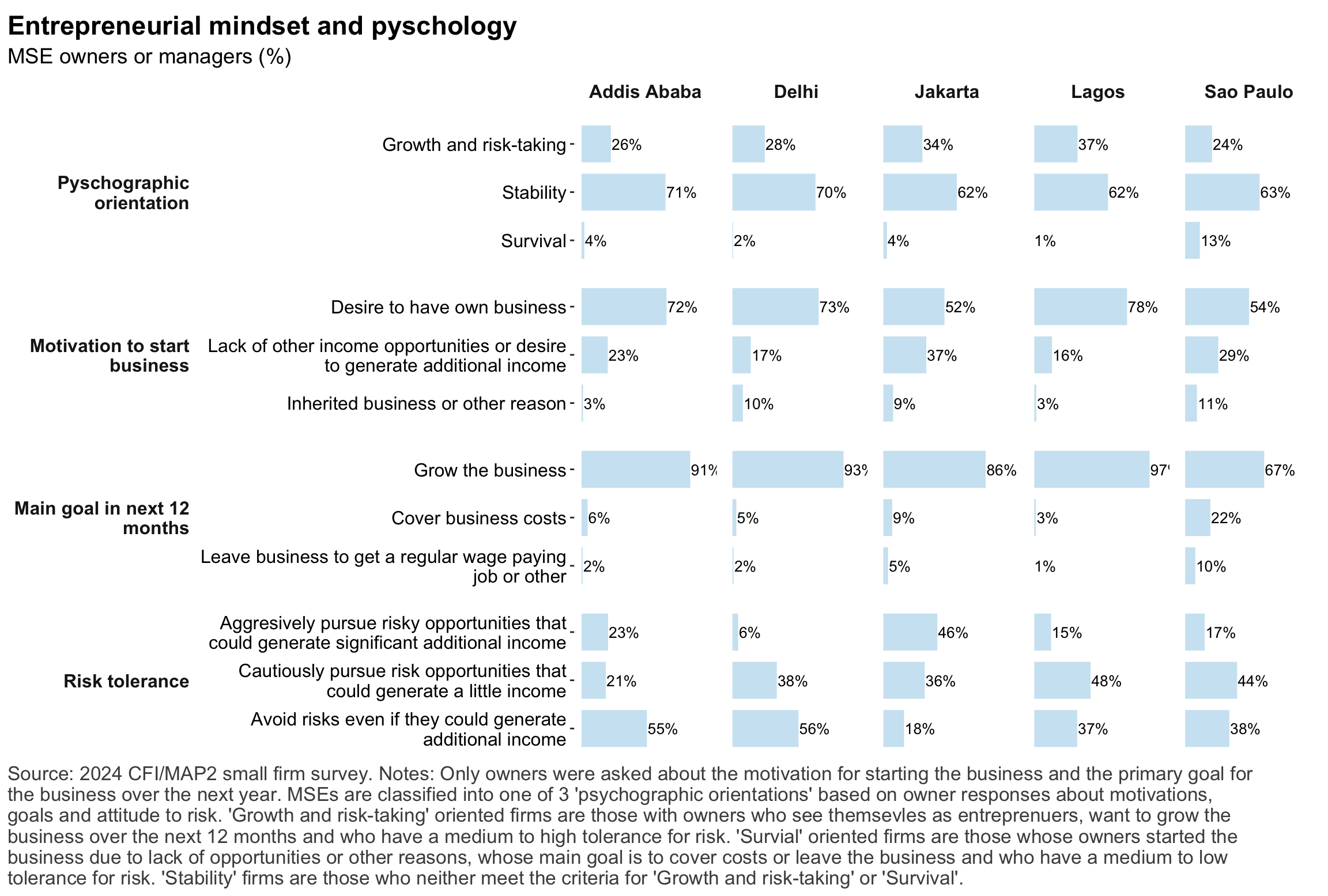

Figure 9: Pyschographic characrteristics of SME owners or managers, by gender

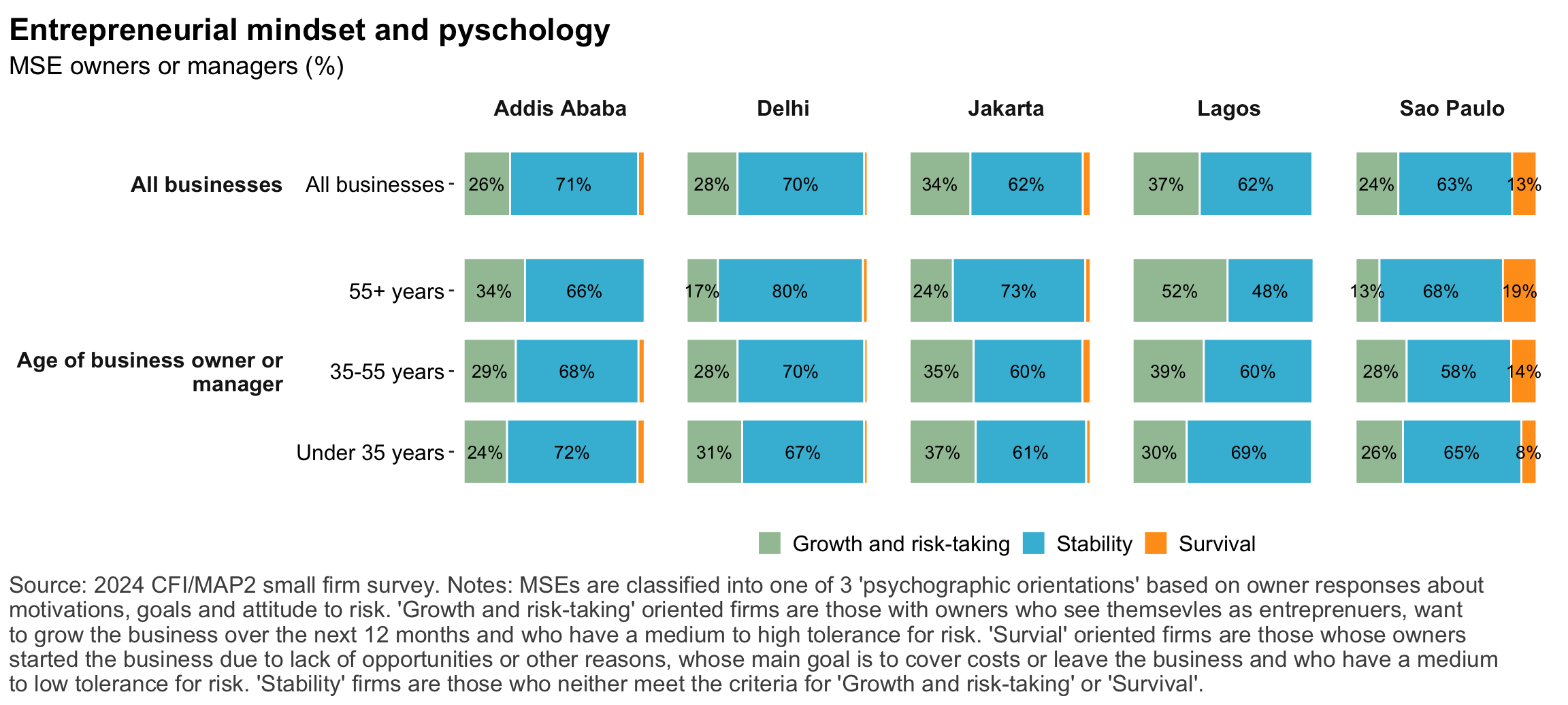

Figure 10: Pyschographic characrteristics of SME owners or managers, by gender

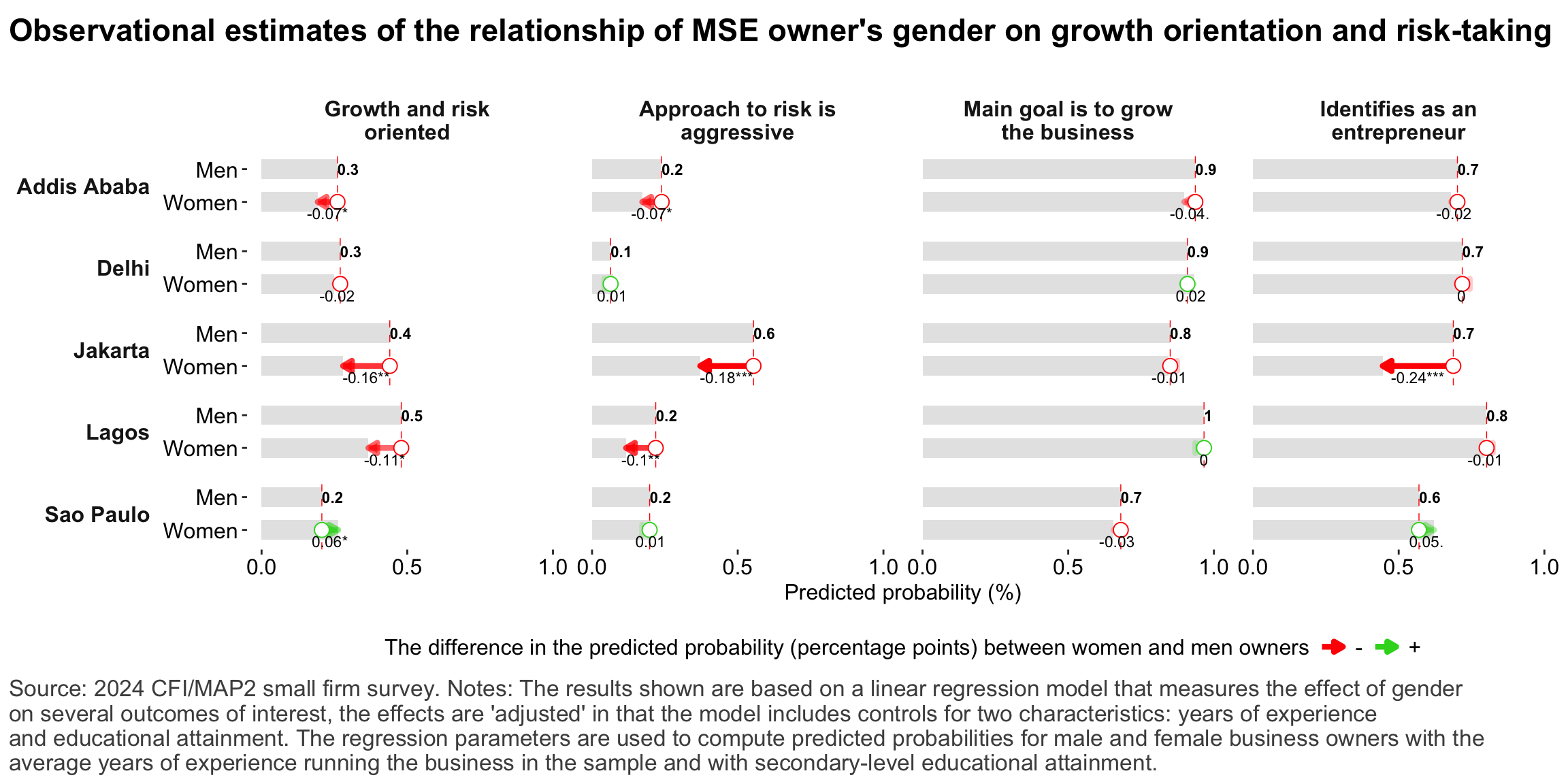

Figure 11: Correlation between owner’s motivations, goals and attitudes to risk

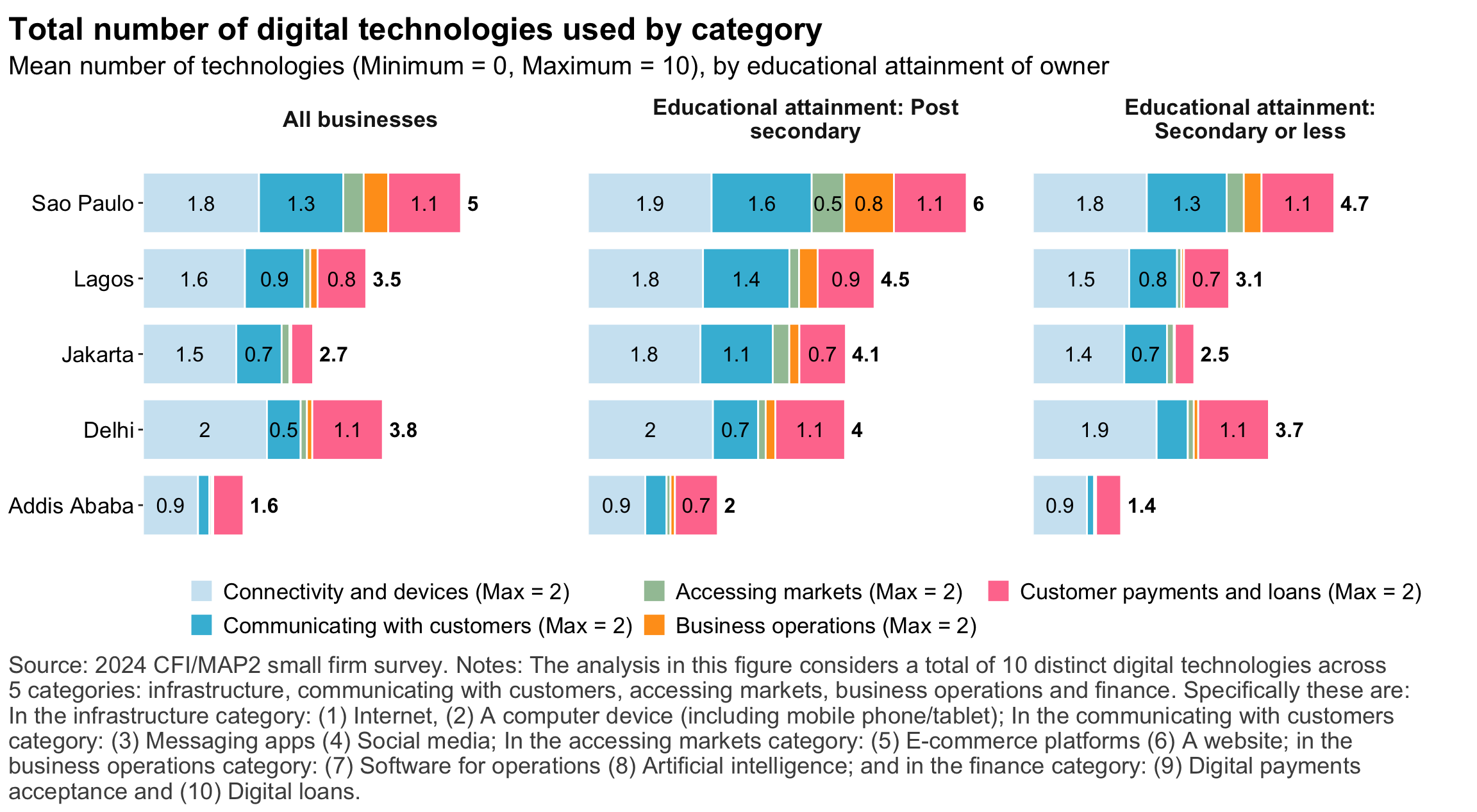

Digital technology strands

Figure 12: Summary measures of financial access

Digital technology

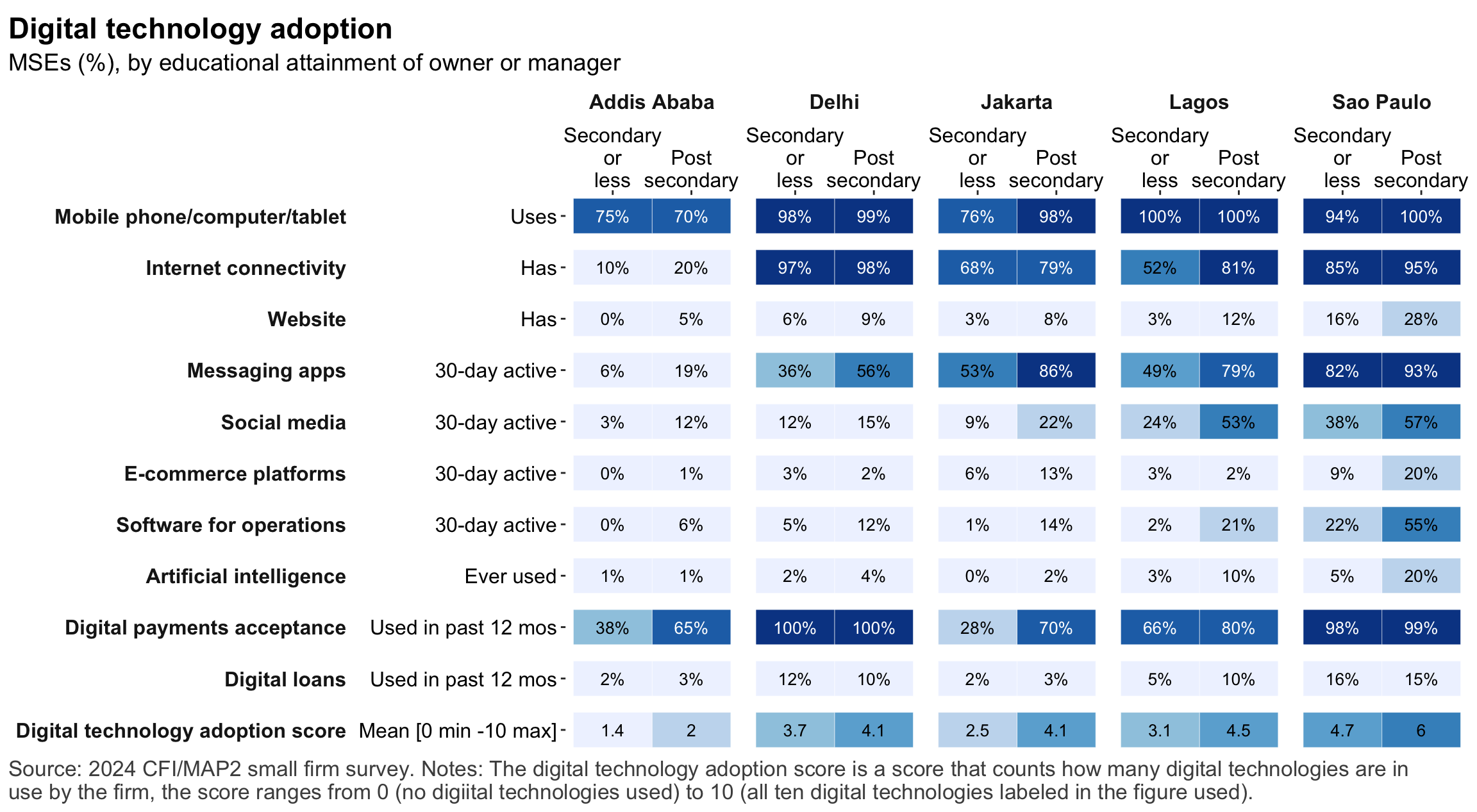

Figure 13: Access to connectivity and devices

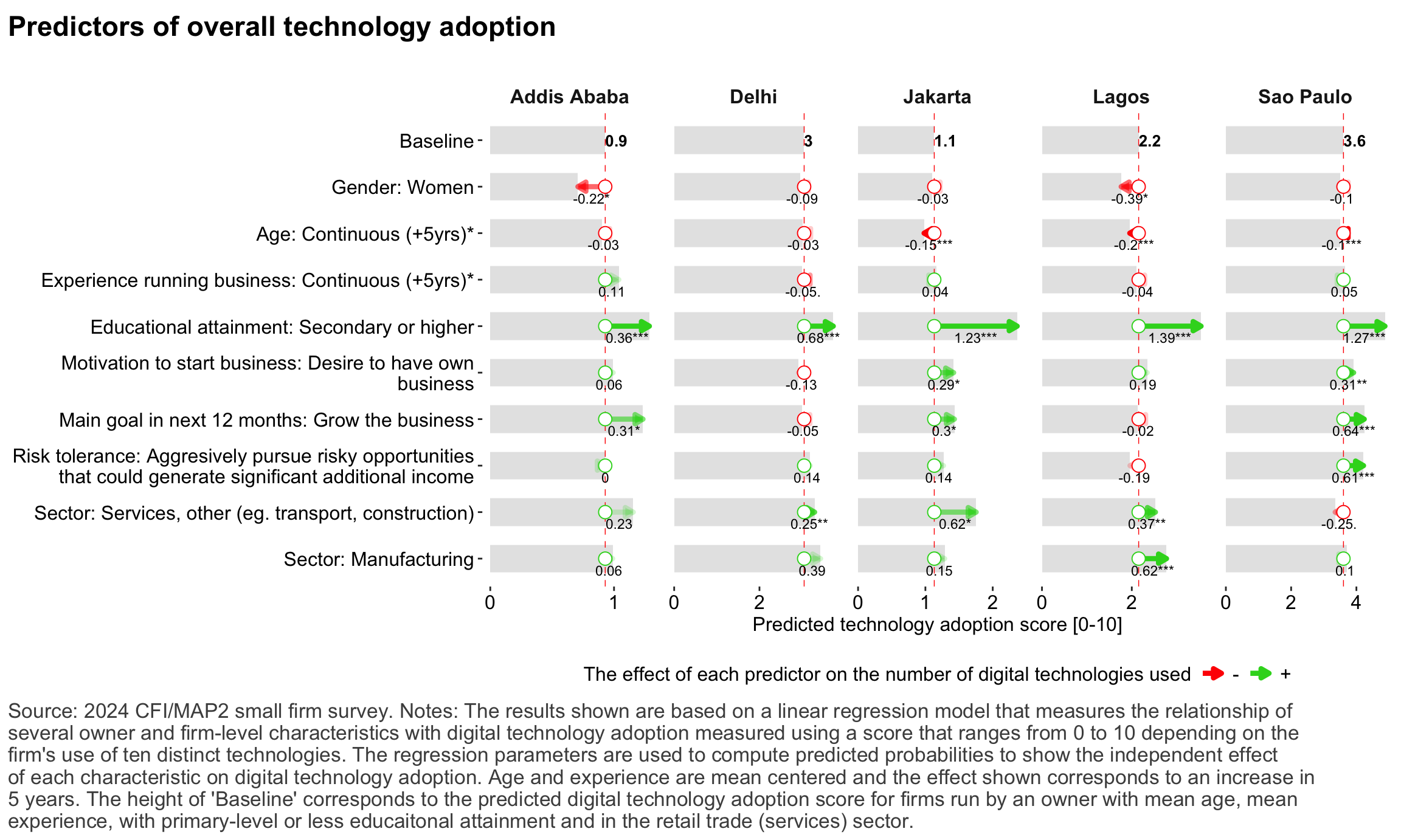

Figure 14: Drivers of overall technology adoption

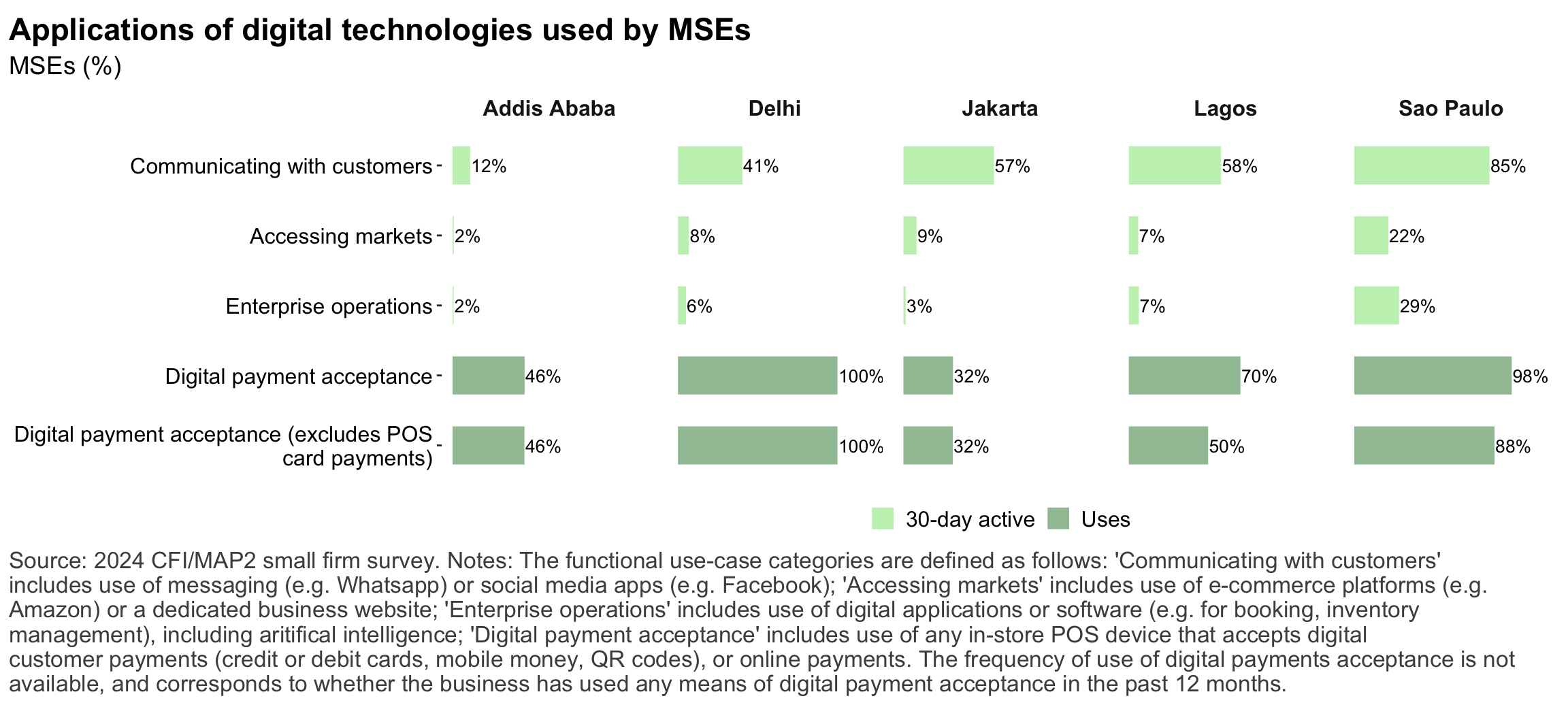

Figure 15: Applications of digital technology

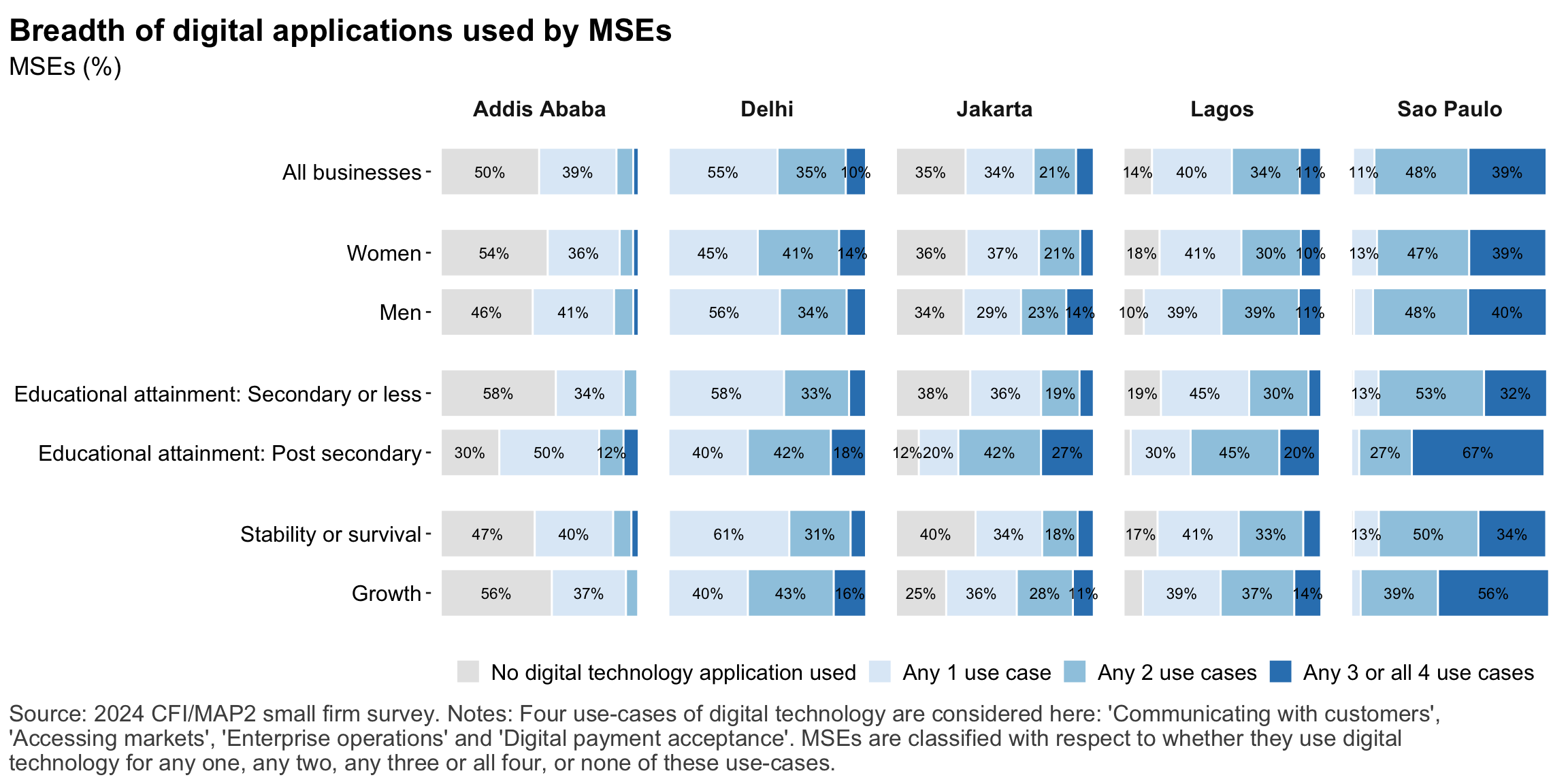

Figure 16: Depth of digital technology adoption

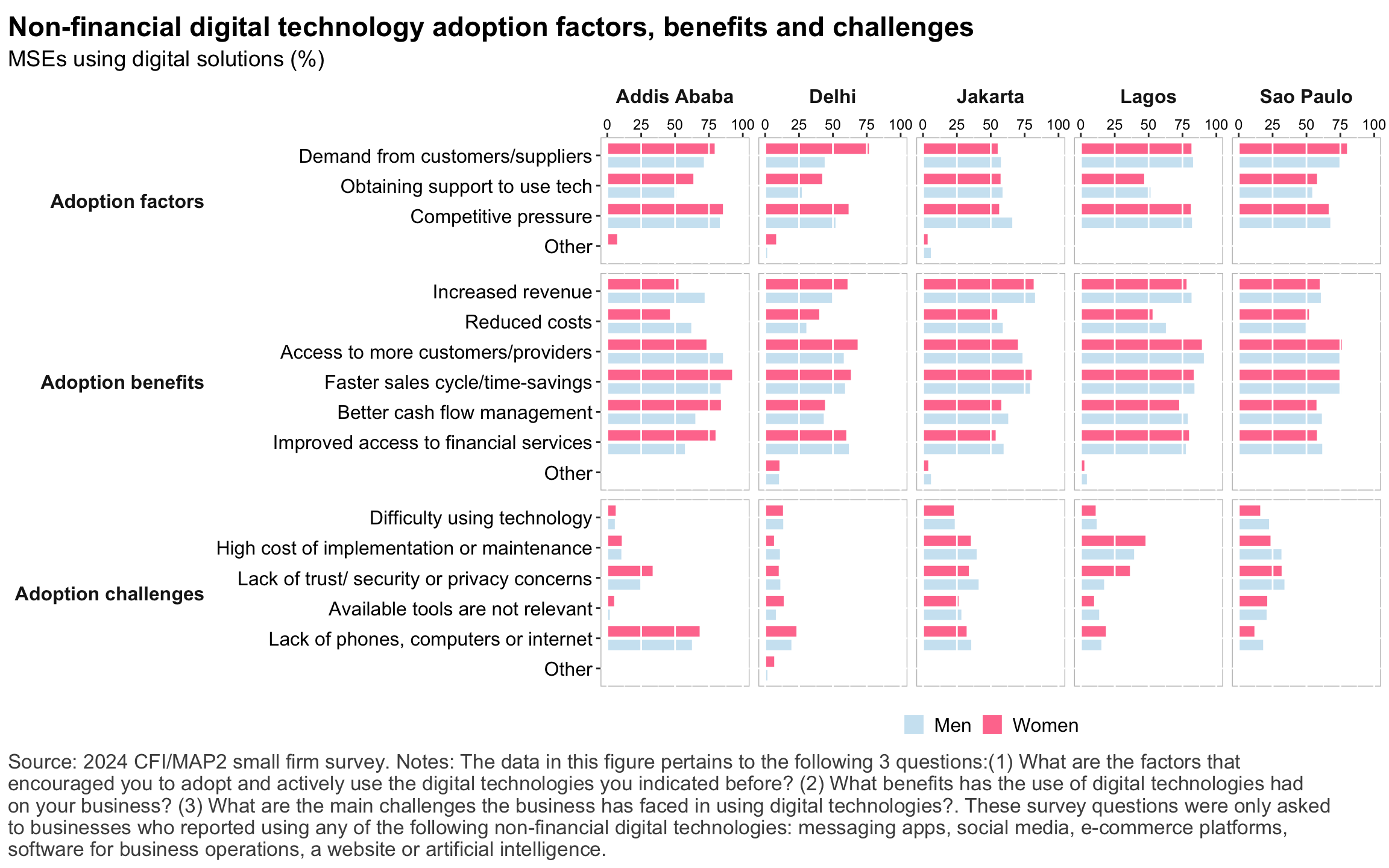

Figure 17: Non-financial digital technology adoption factors

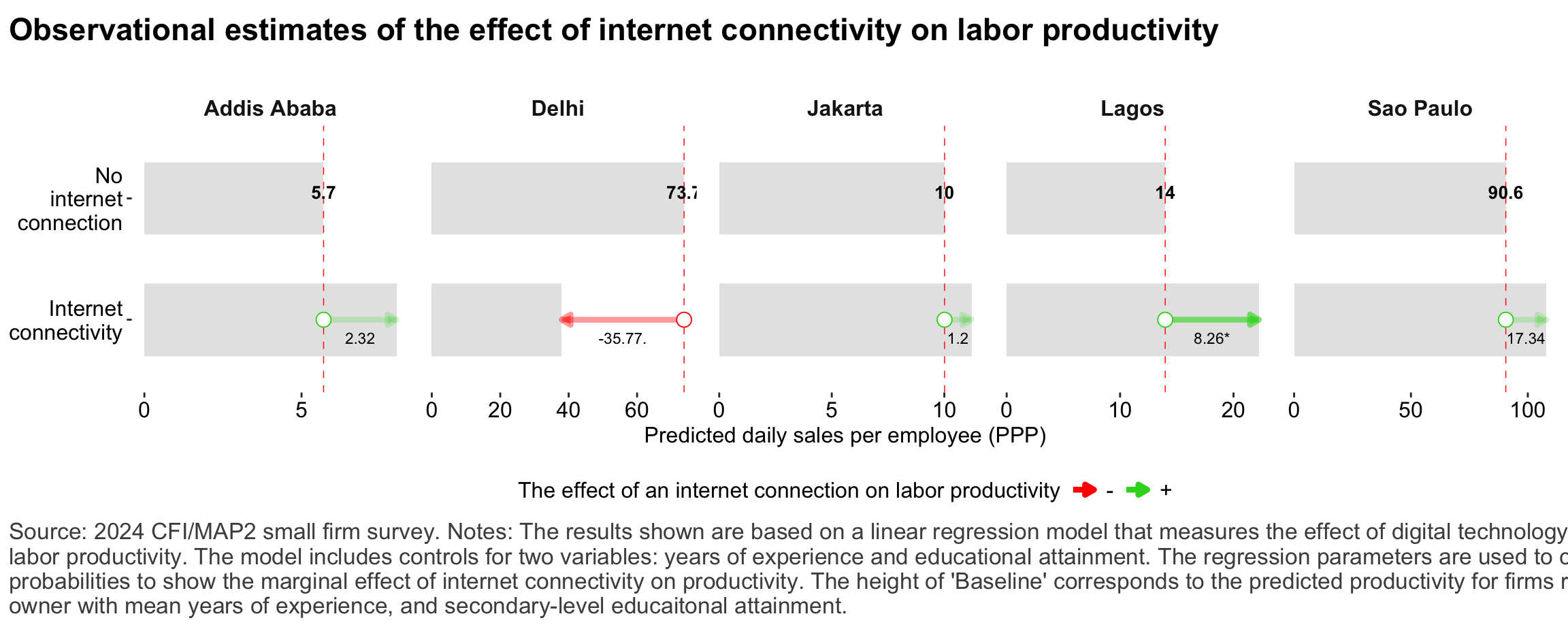

Figure 18: Relationship between internet-connectivity and firm-level labor productivity

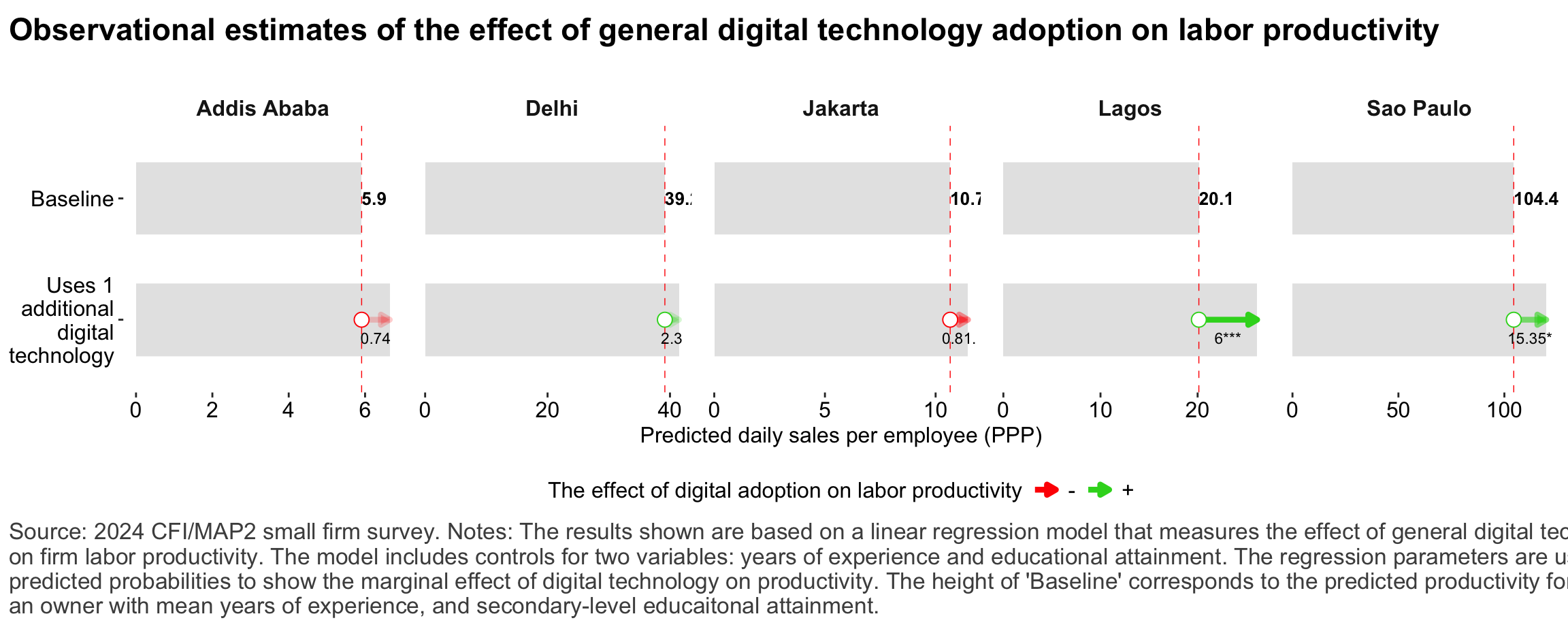

Figure 19: Relationship between digital technology and firm-level labor productivity

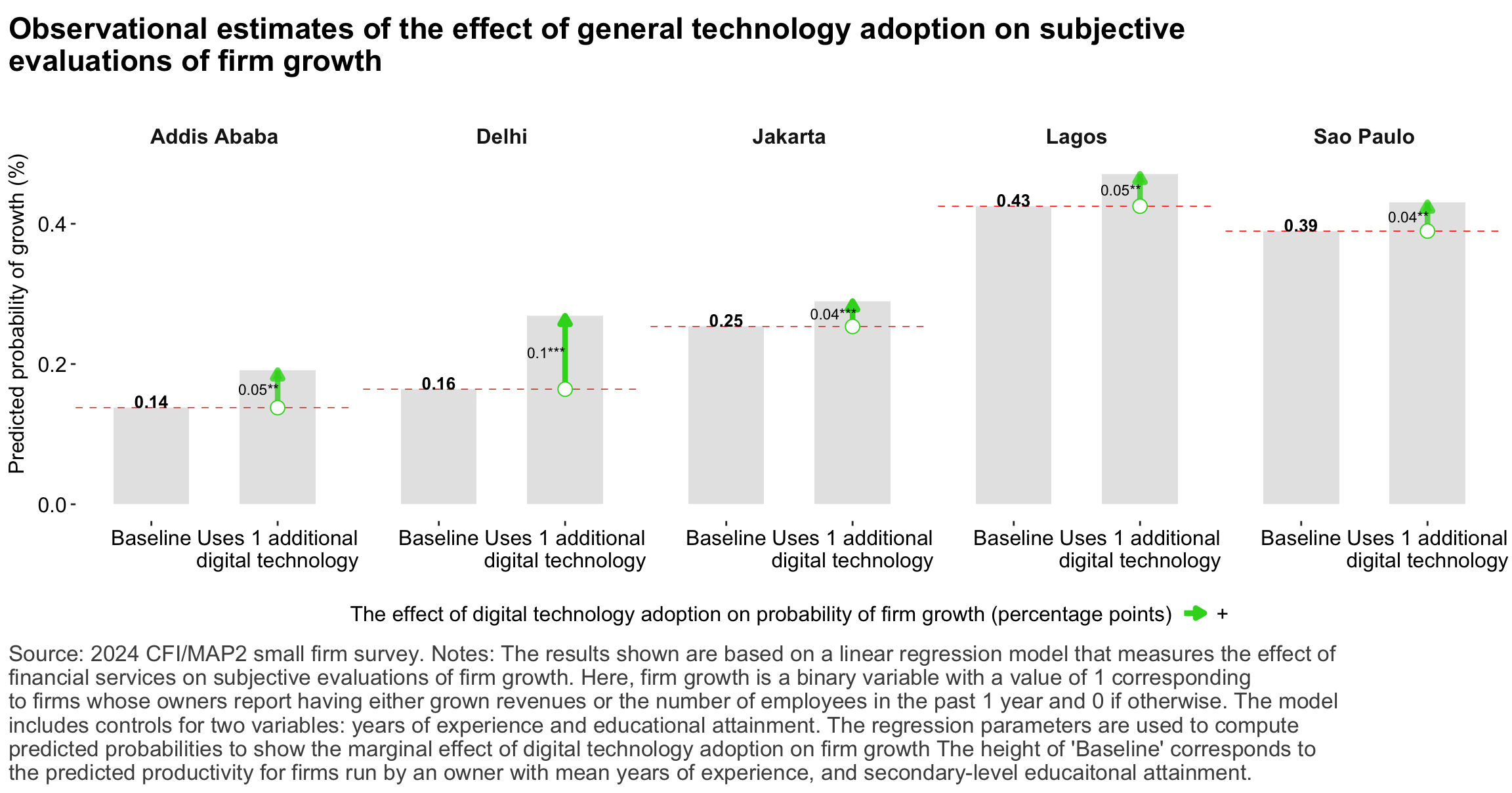

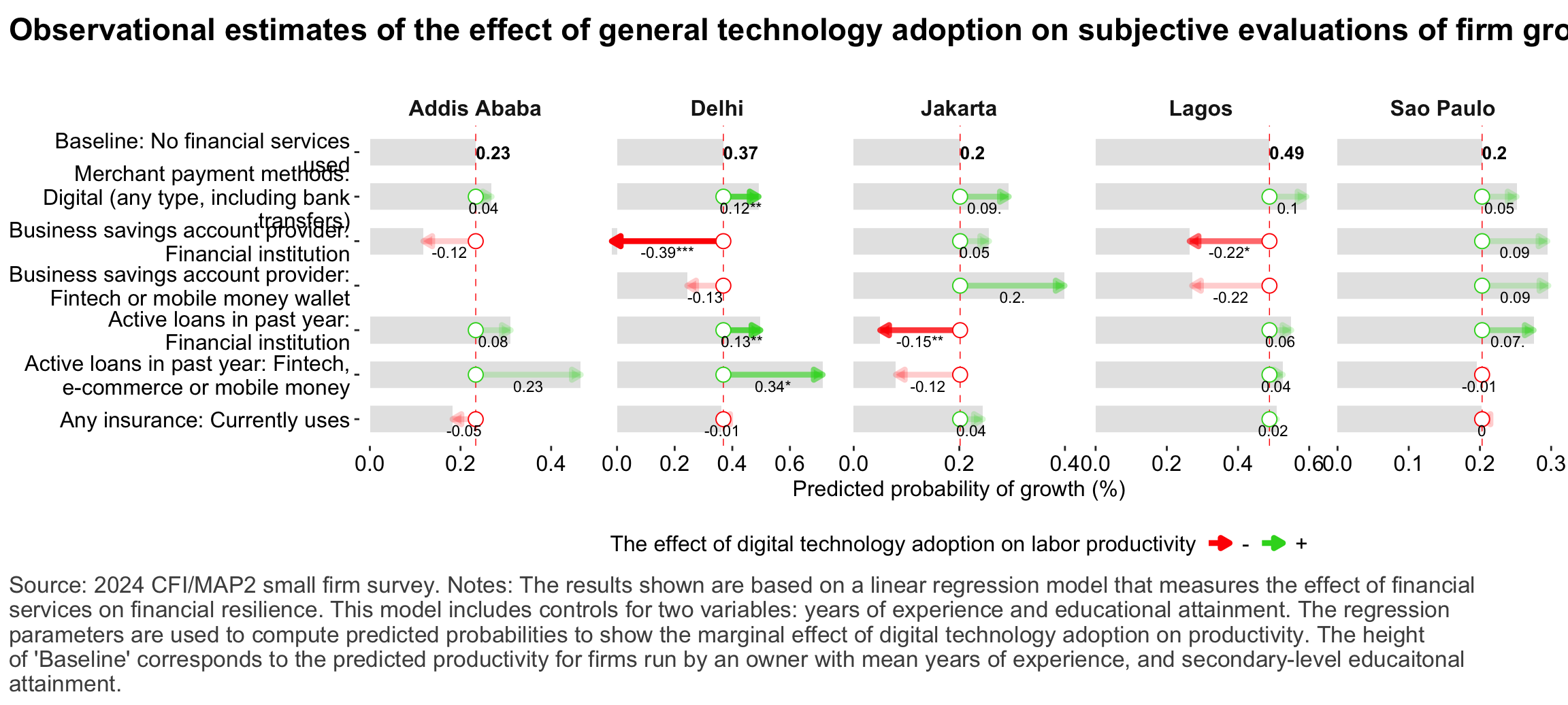

Figure 20: Relationship between general digital technology adoption and subjective growth

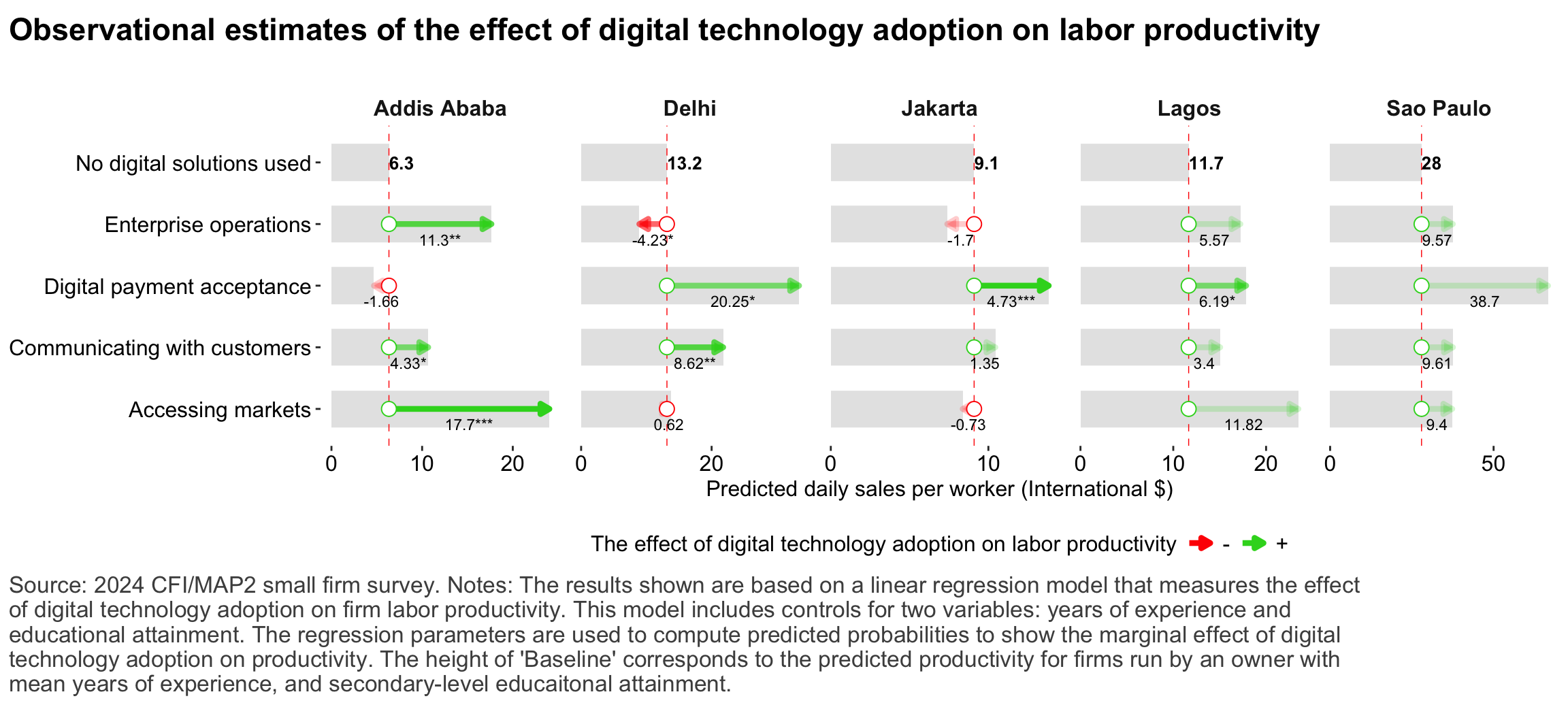

Figure 21: Relationship between digital technology adoption and firm-level labor productivity

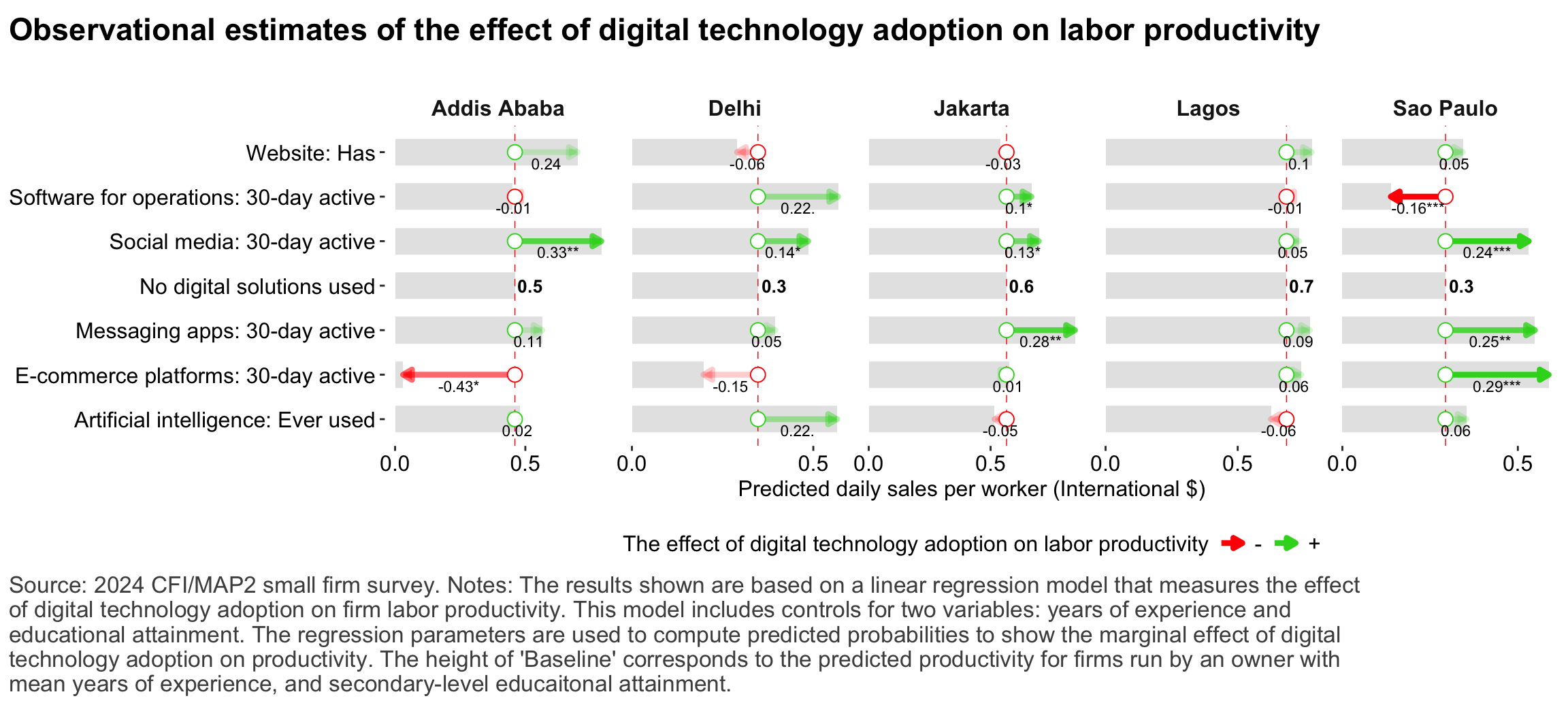

Figure 22: Relationship between digital technology adoption and firm-level labor productivity

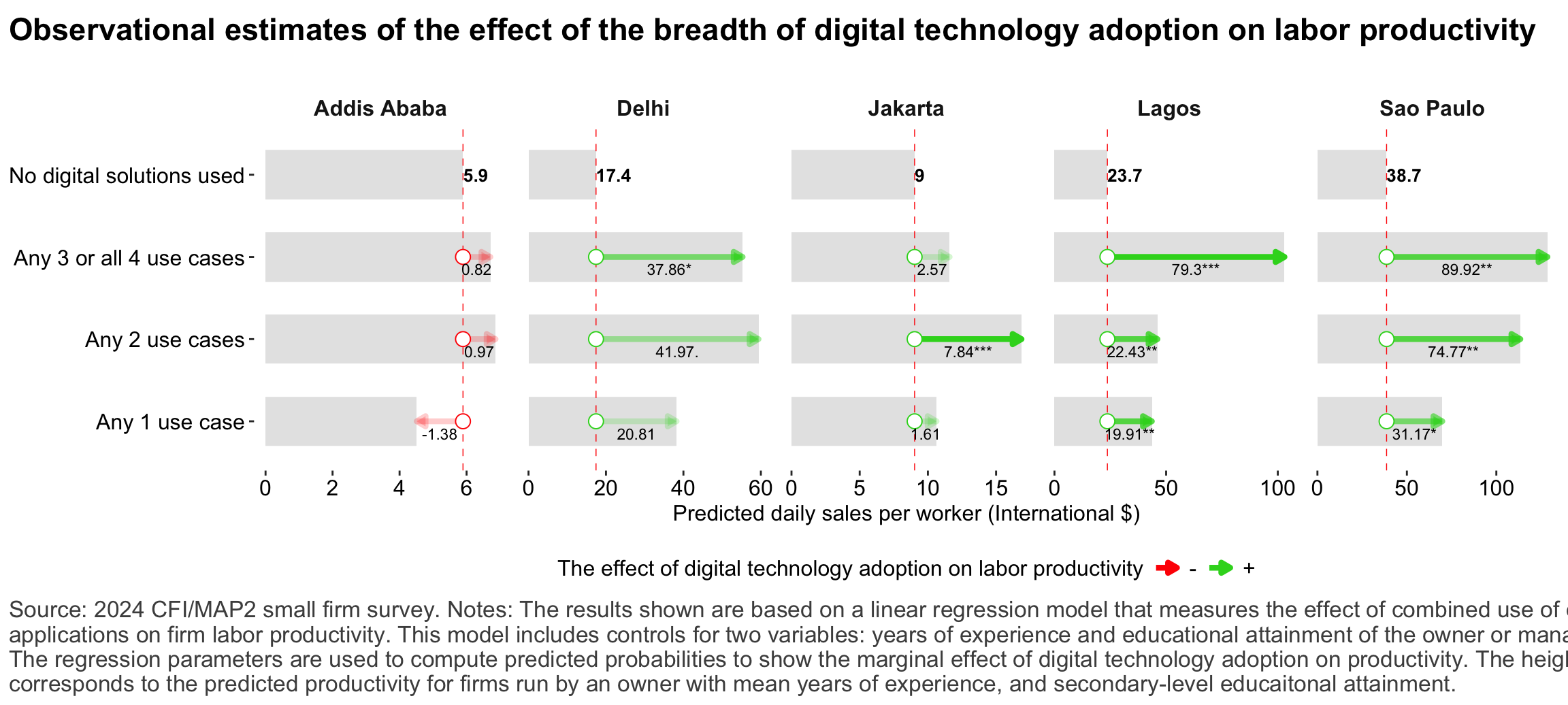

Figure 23: Relationship between depth of digital technology adoption and firm-level labor productivity

Financial services

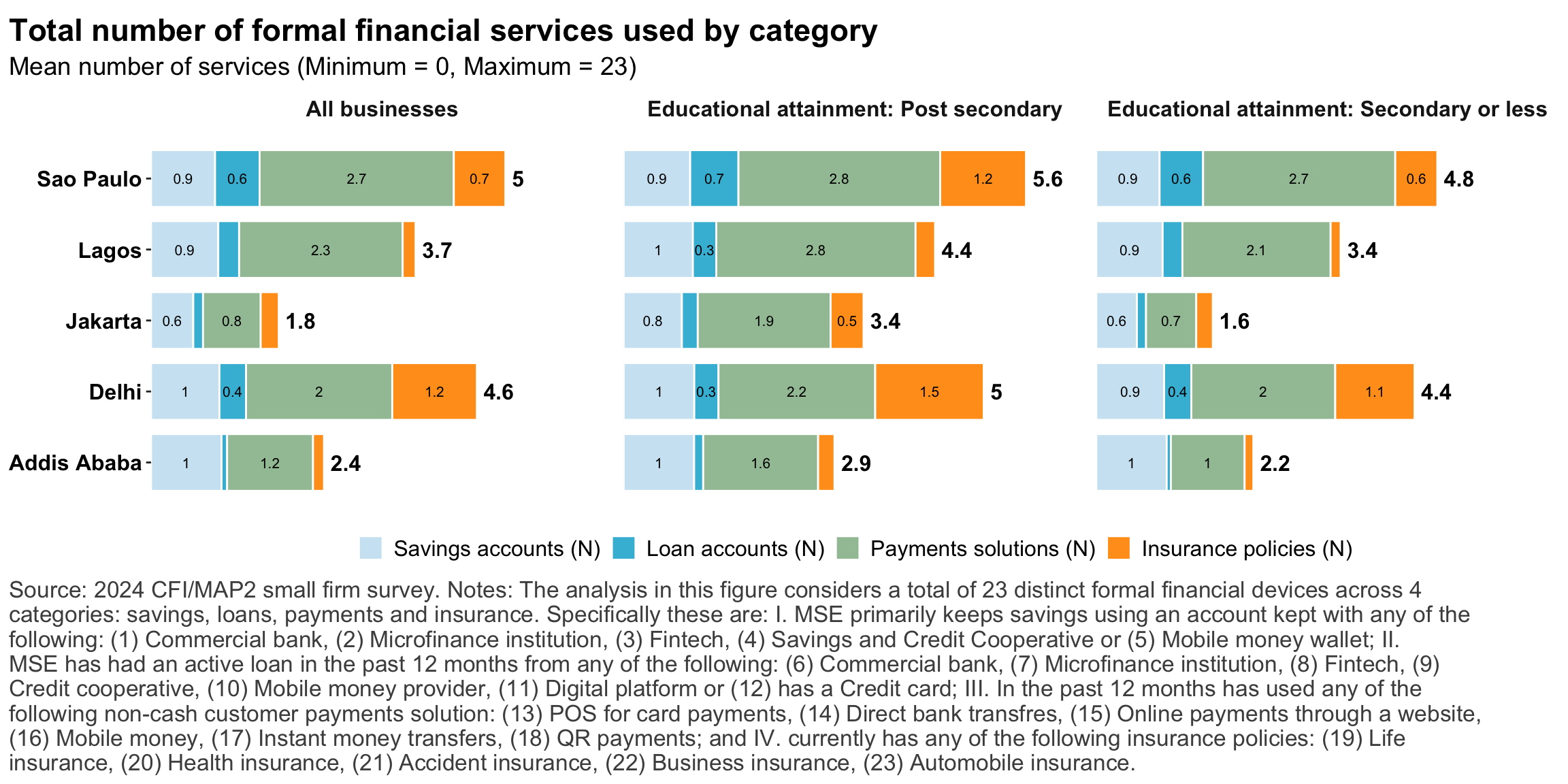

Figure 24: Summary measures of financial access

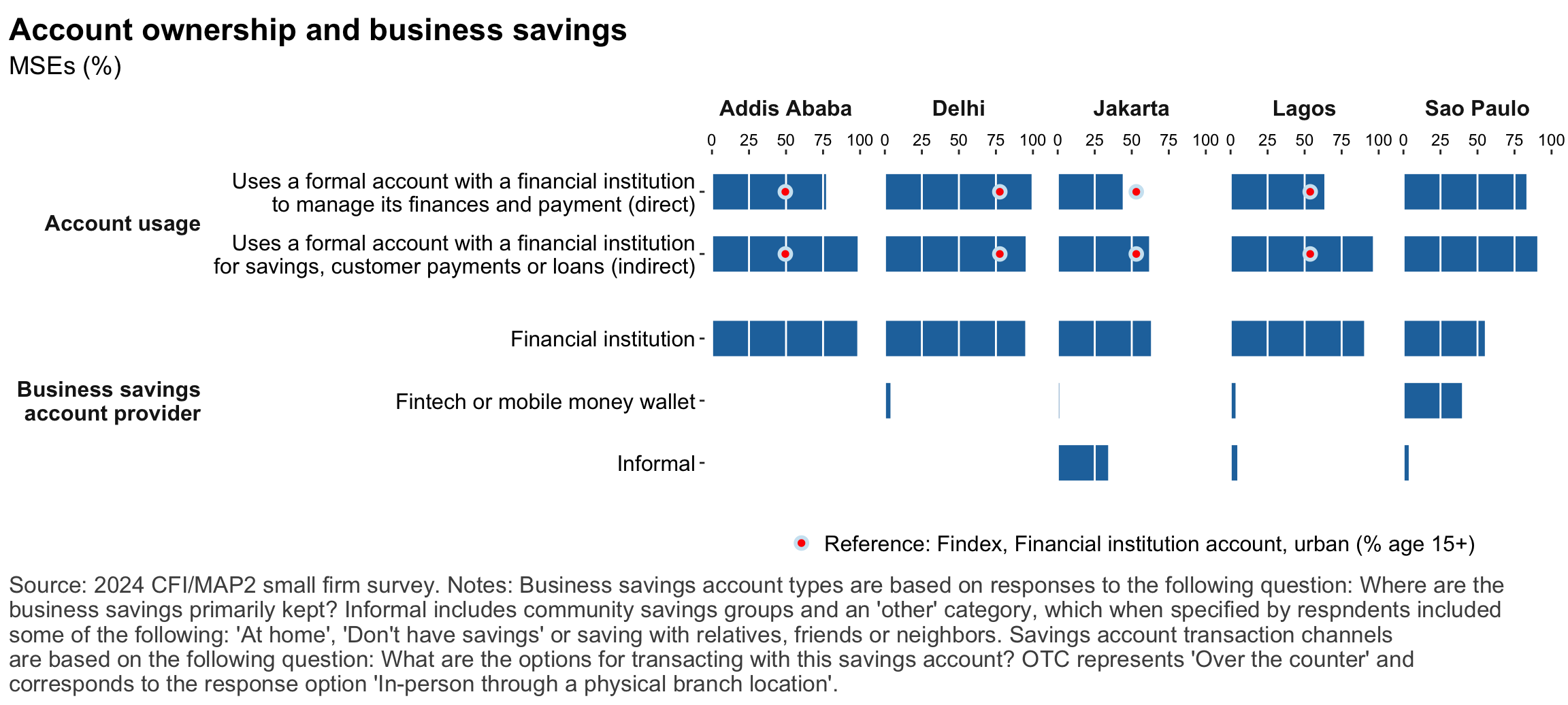

Figure 25: Financical accounts and savings

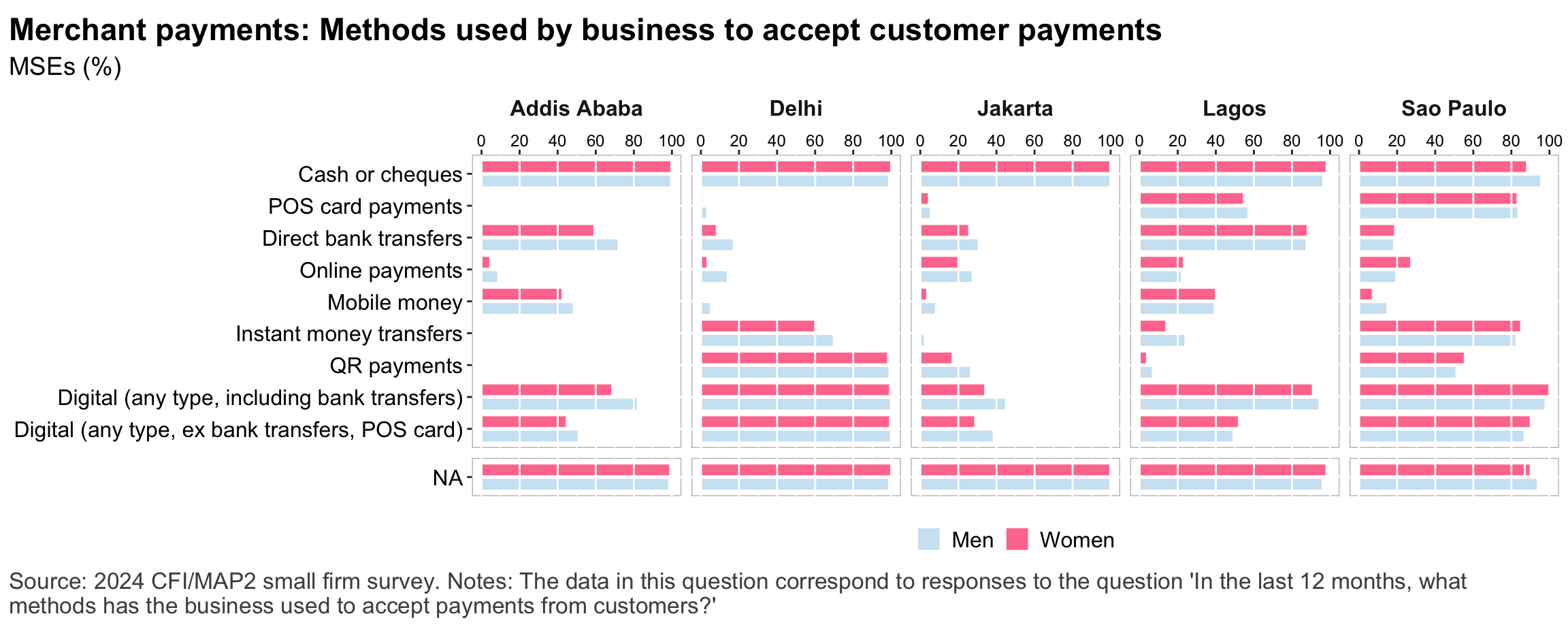

Figure 26: Merchant payments

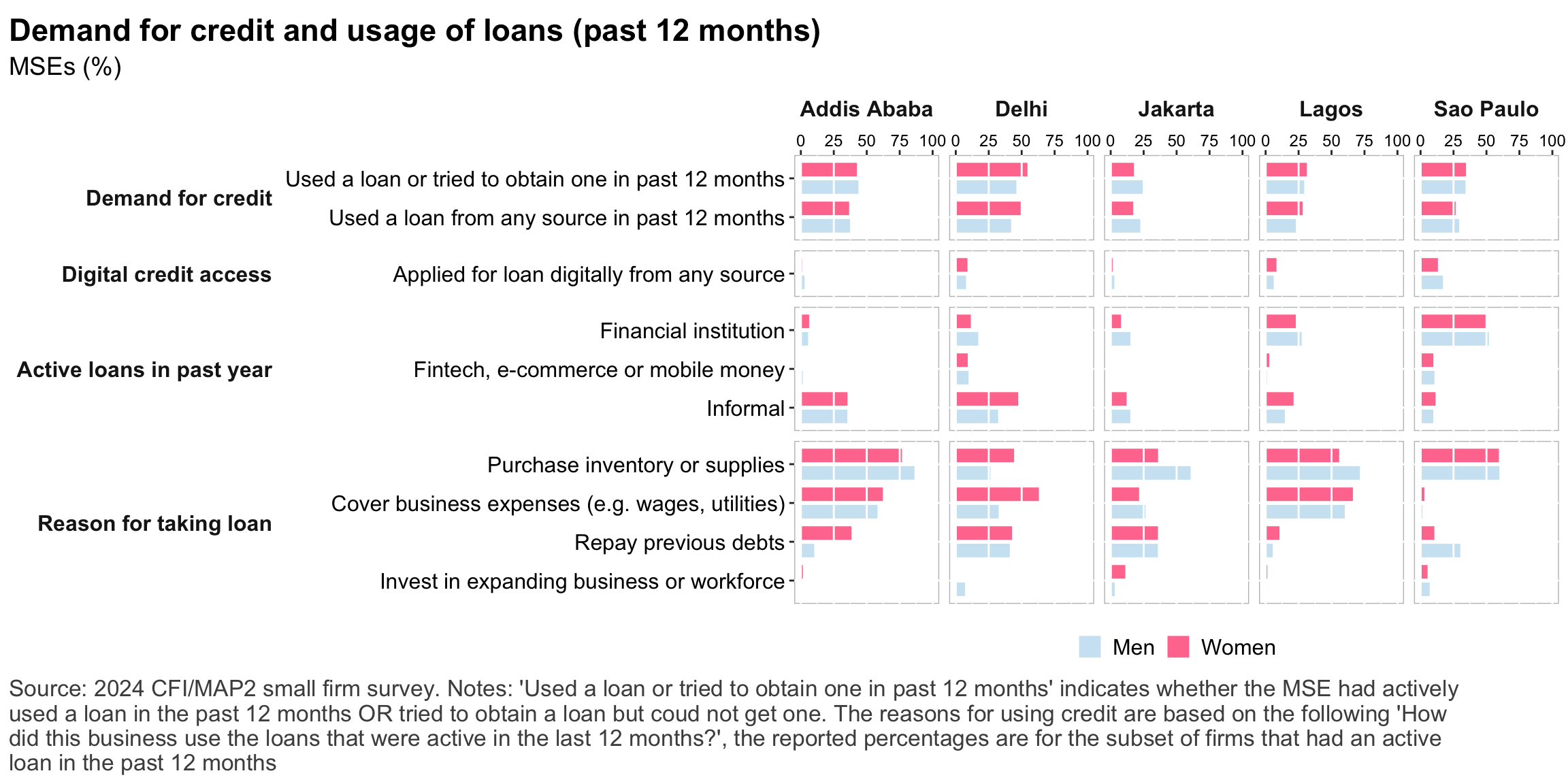

Figure 27: Demand for credit

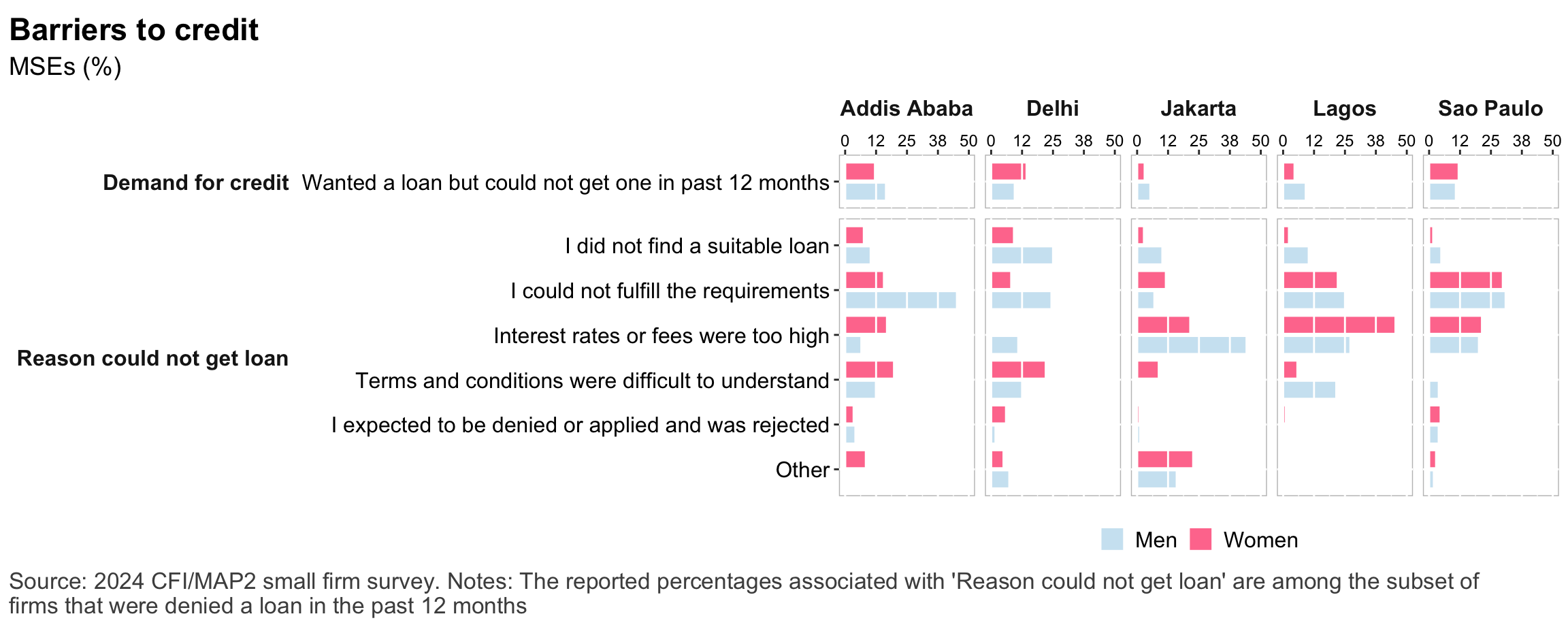

Figure 28: Barriers to credit

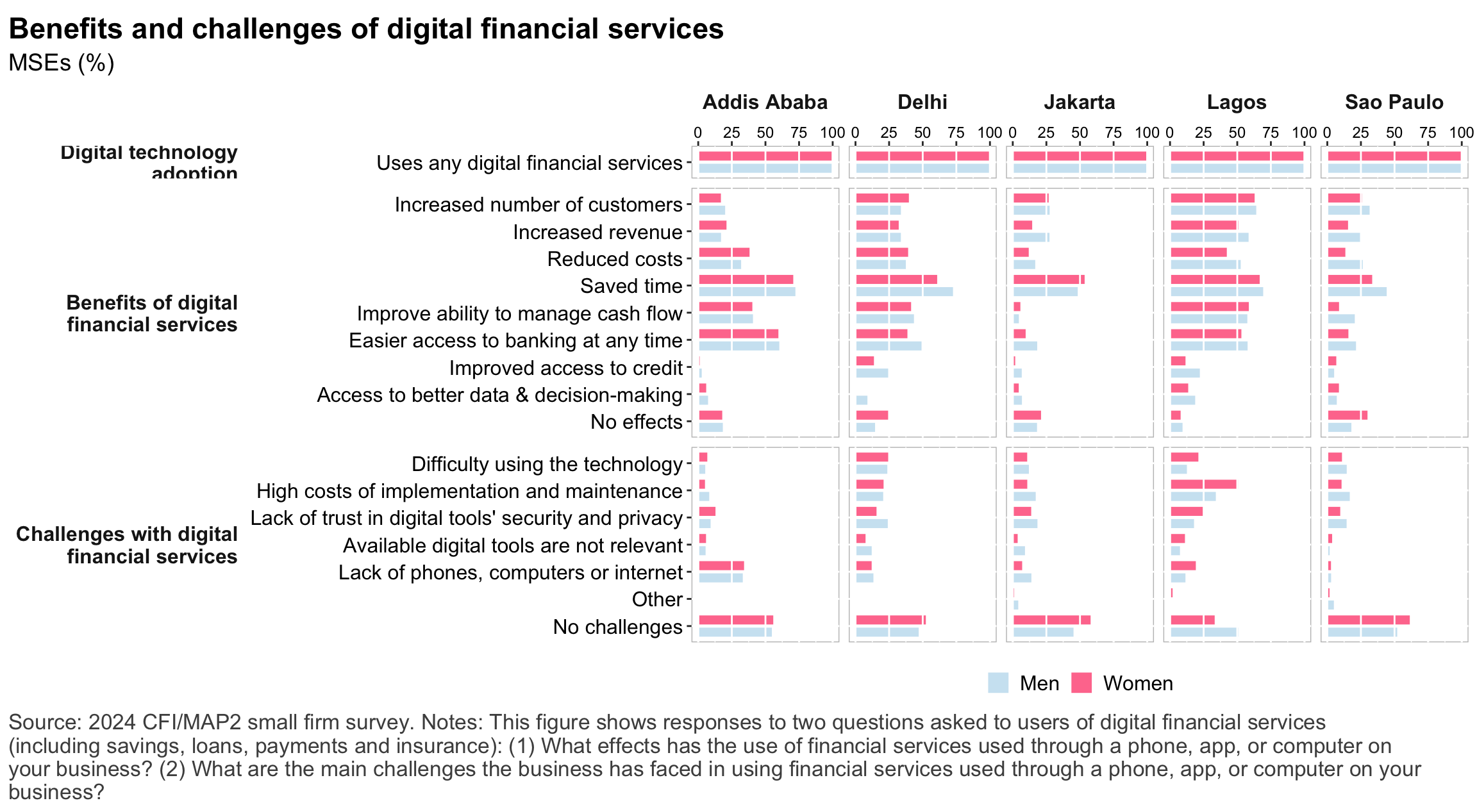

Figure 29: Impacts of digital financial services

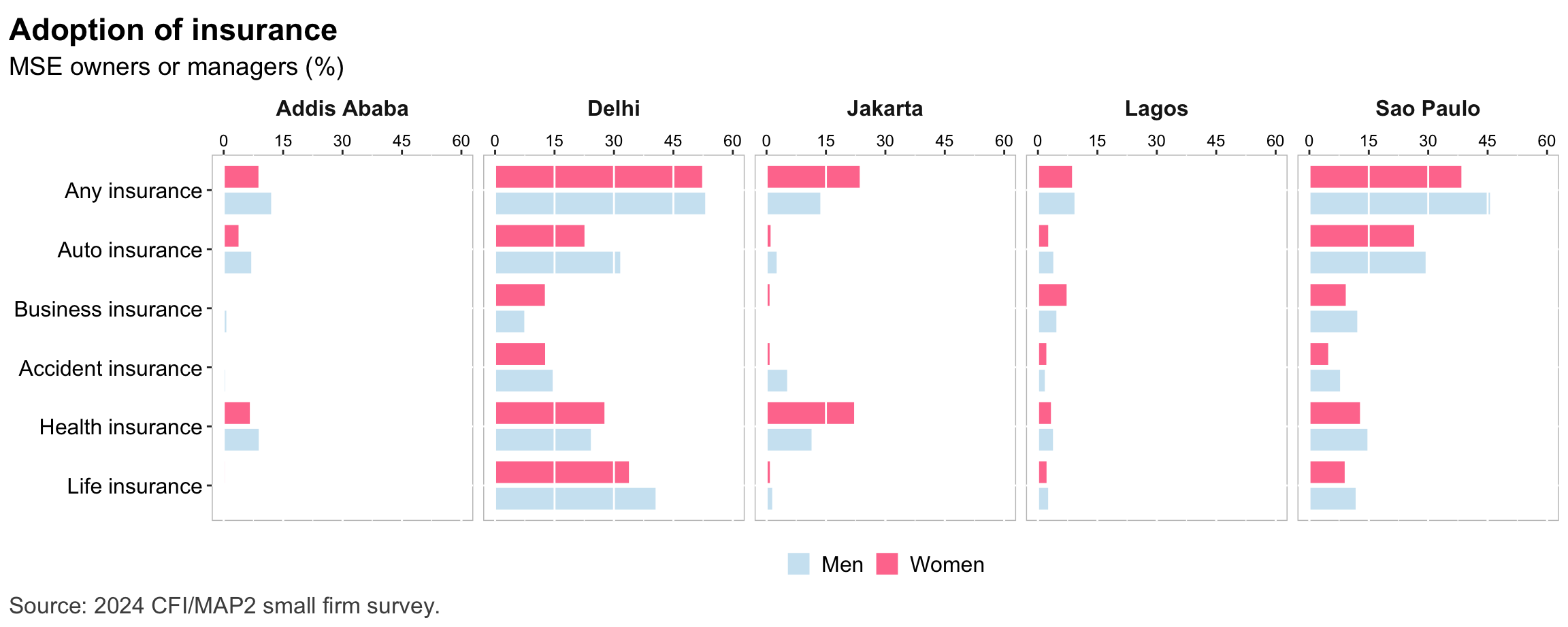

Figure 30: Insurance usage

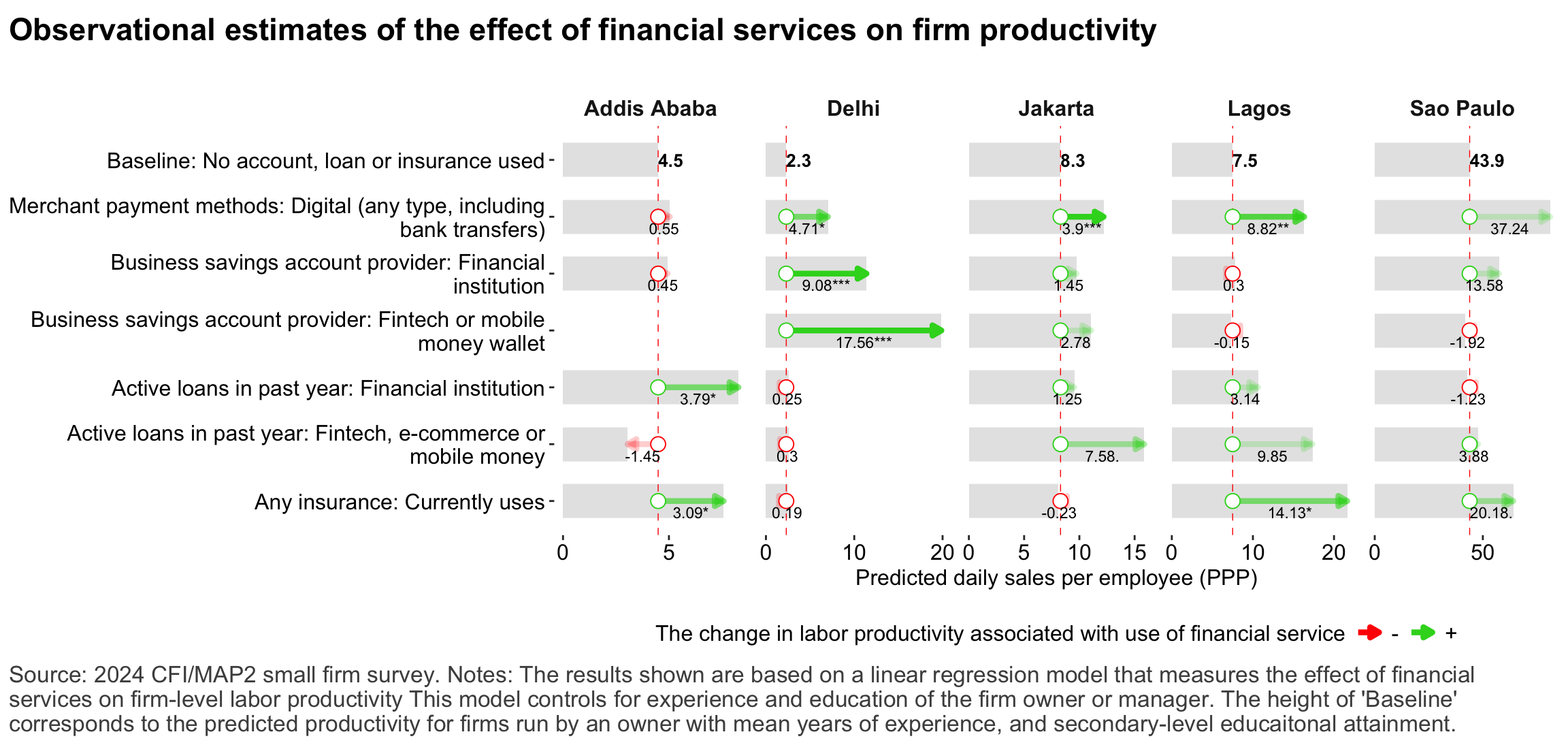

Figure 31: Relationship between financial services and firm-level labor productivity

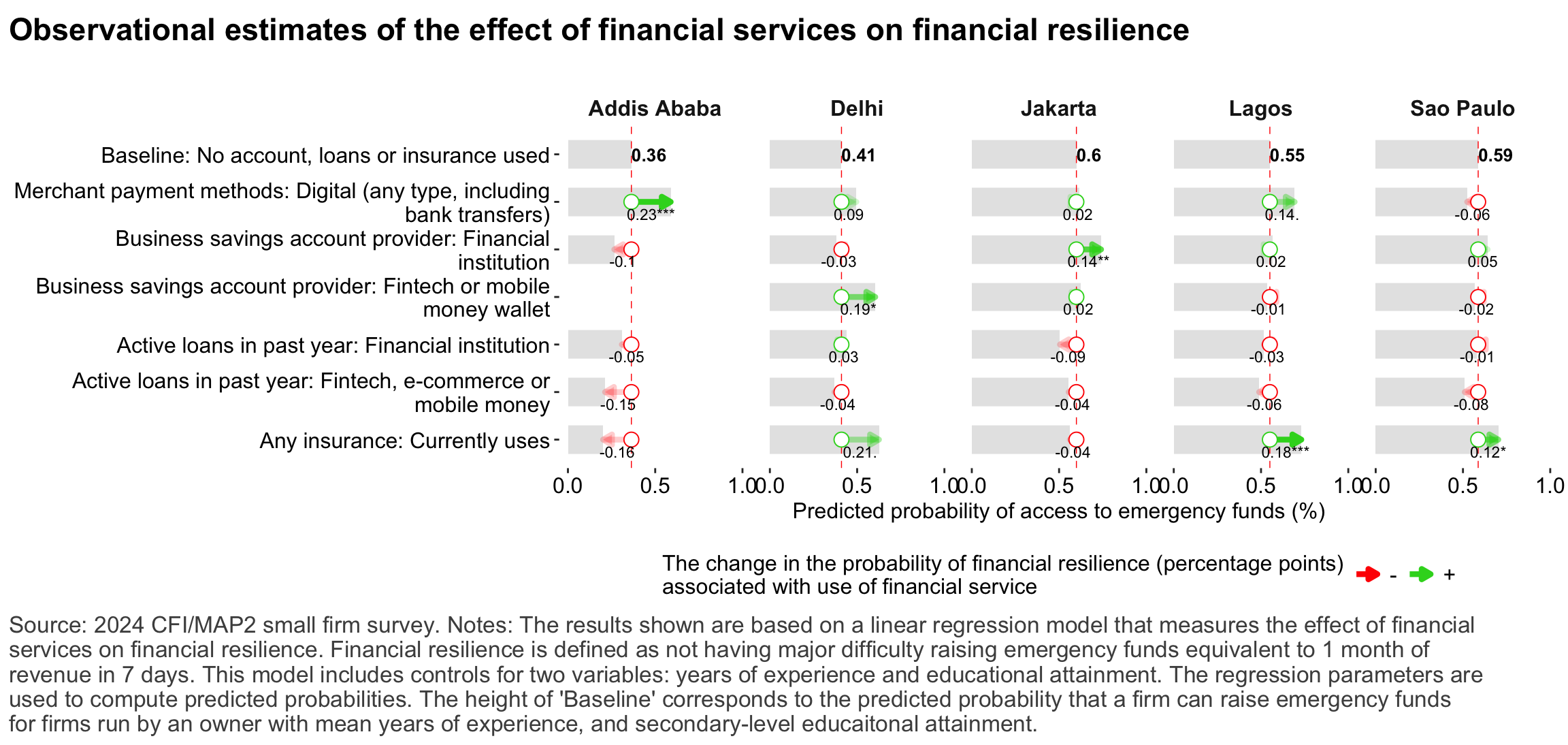

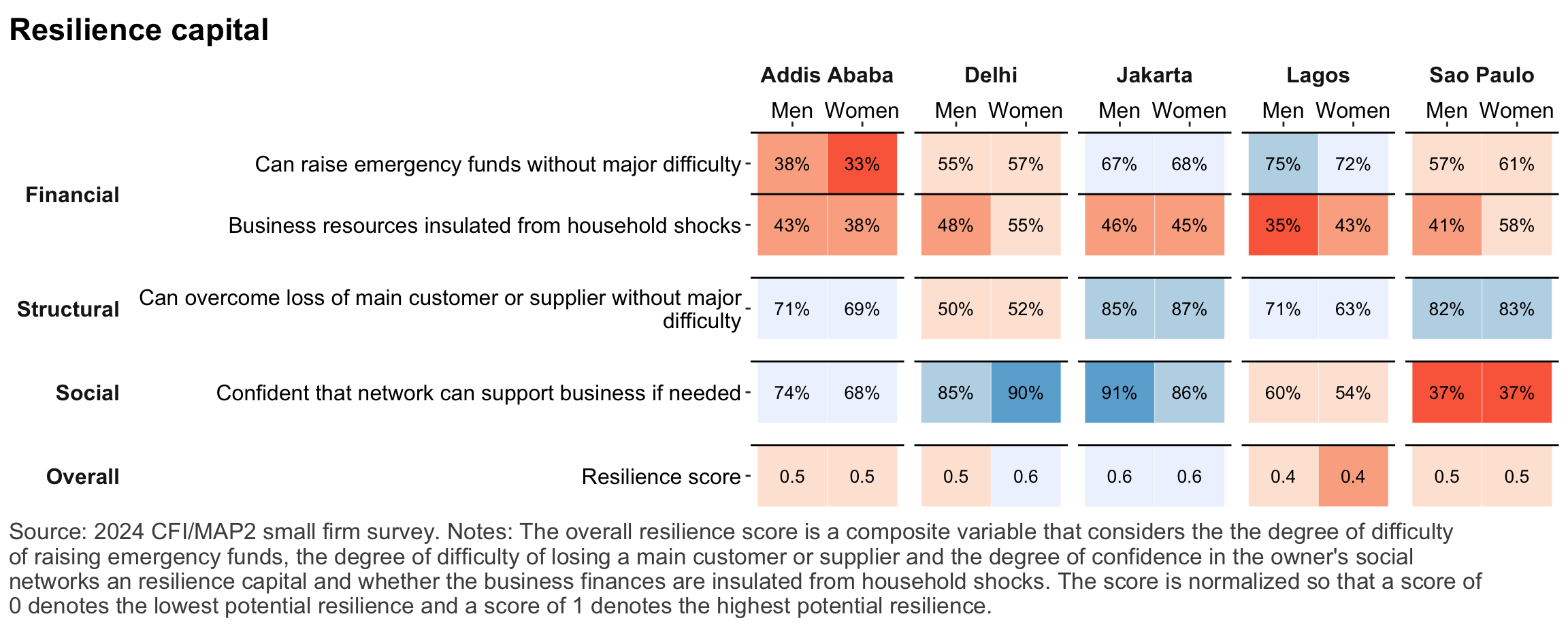

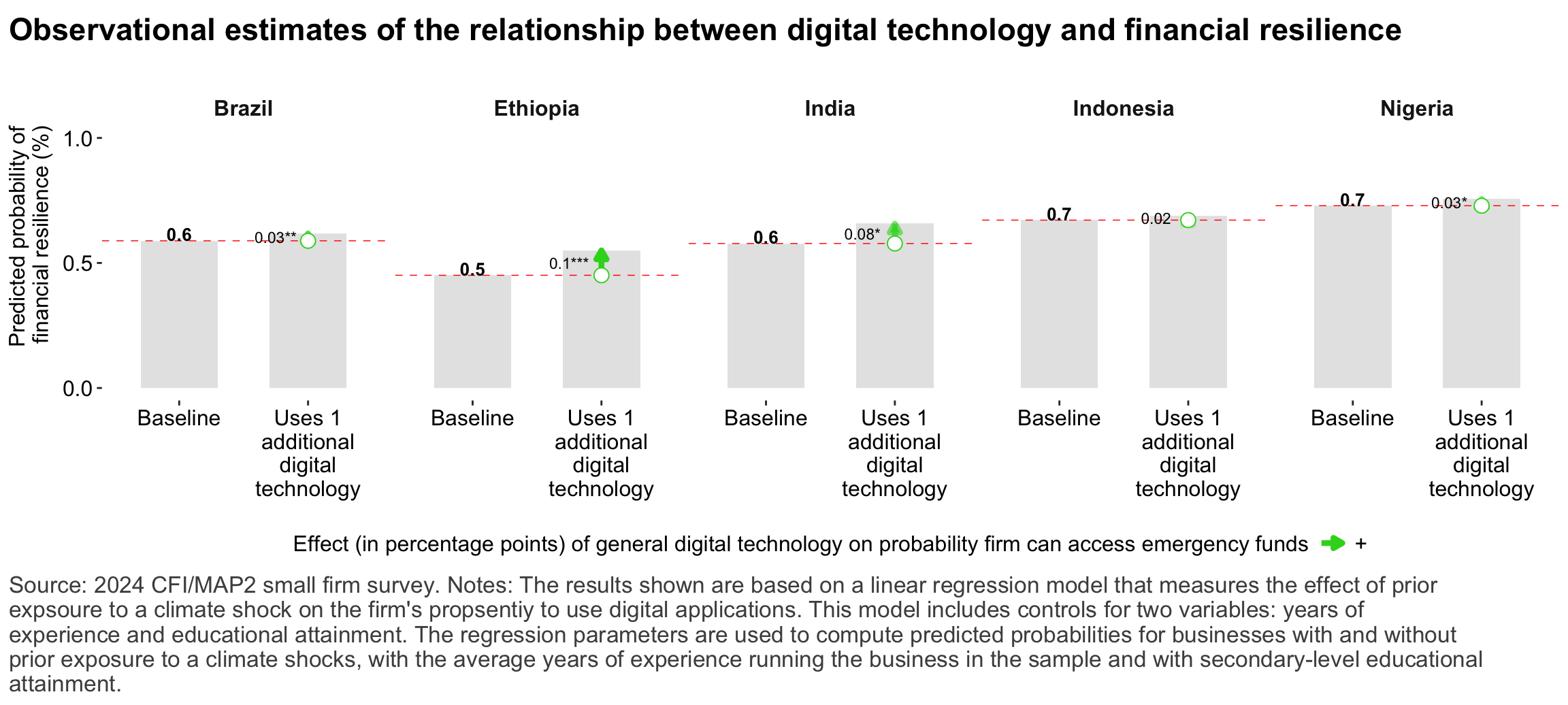

Figure 32: Relationship between financial services and financial resilience

Figure 33: Relationship between financial services and firm growth

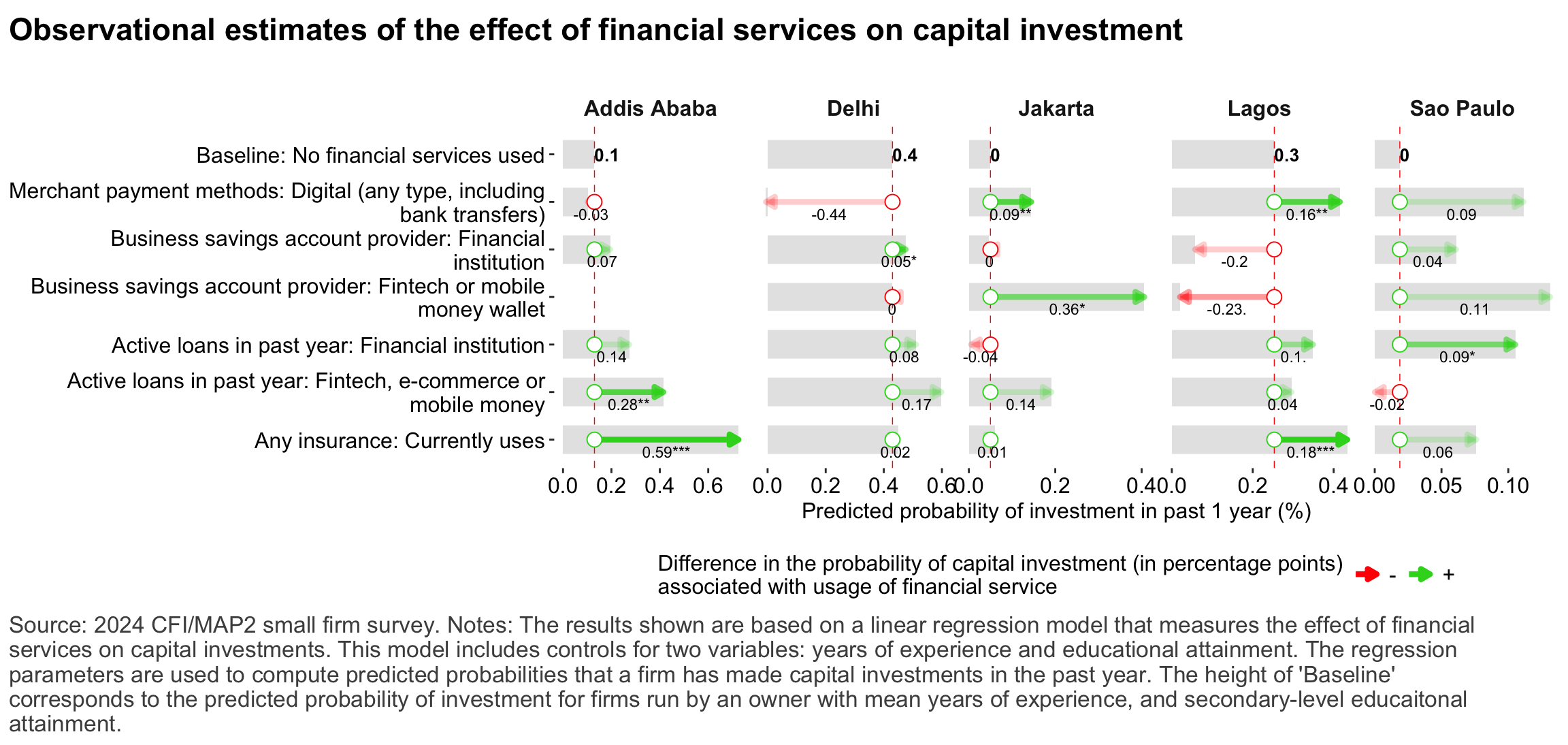

Figure 34: Relationship between financial services and capital investment

Consumer protection

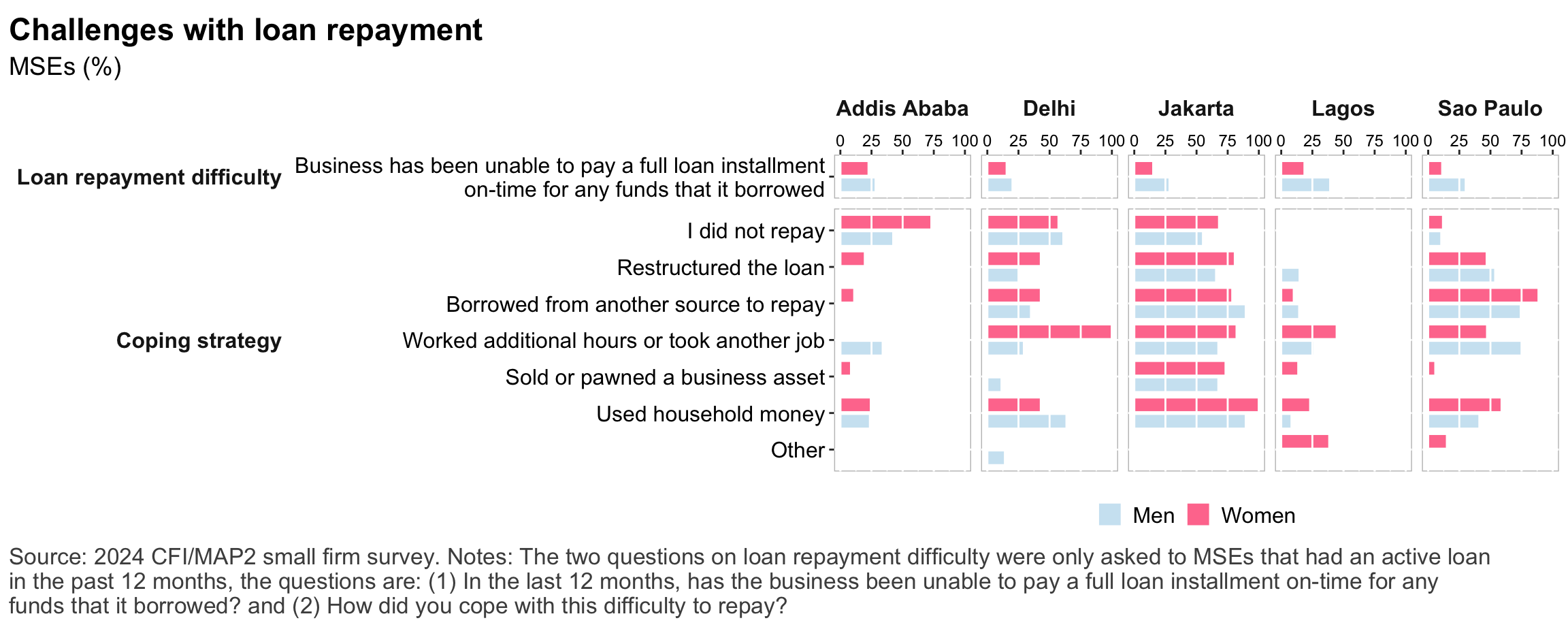

Figure 35: Challenges with loan repayment

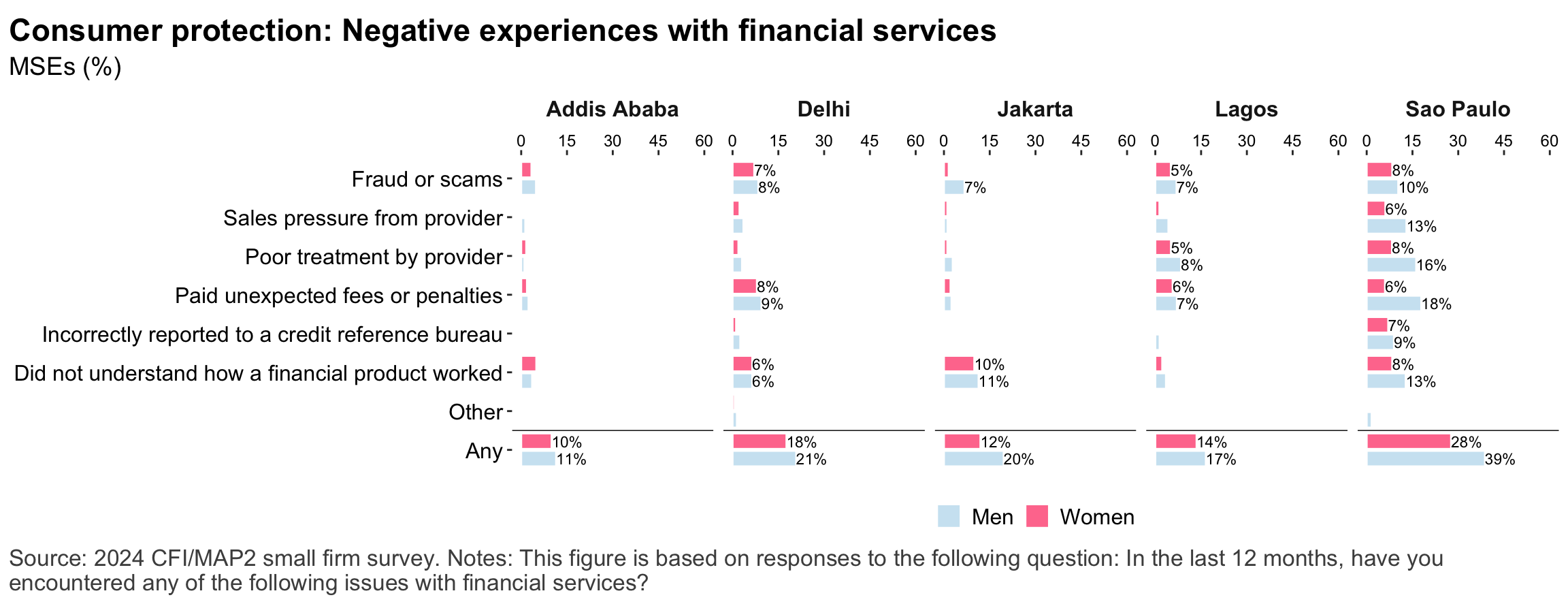

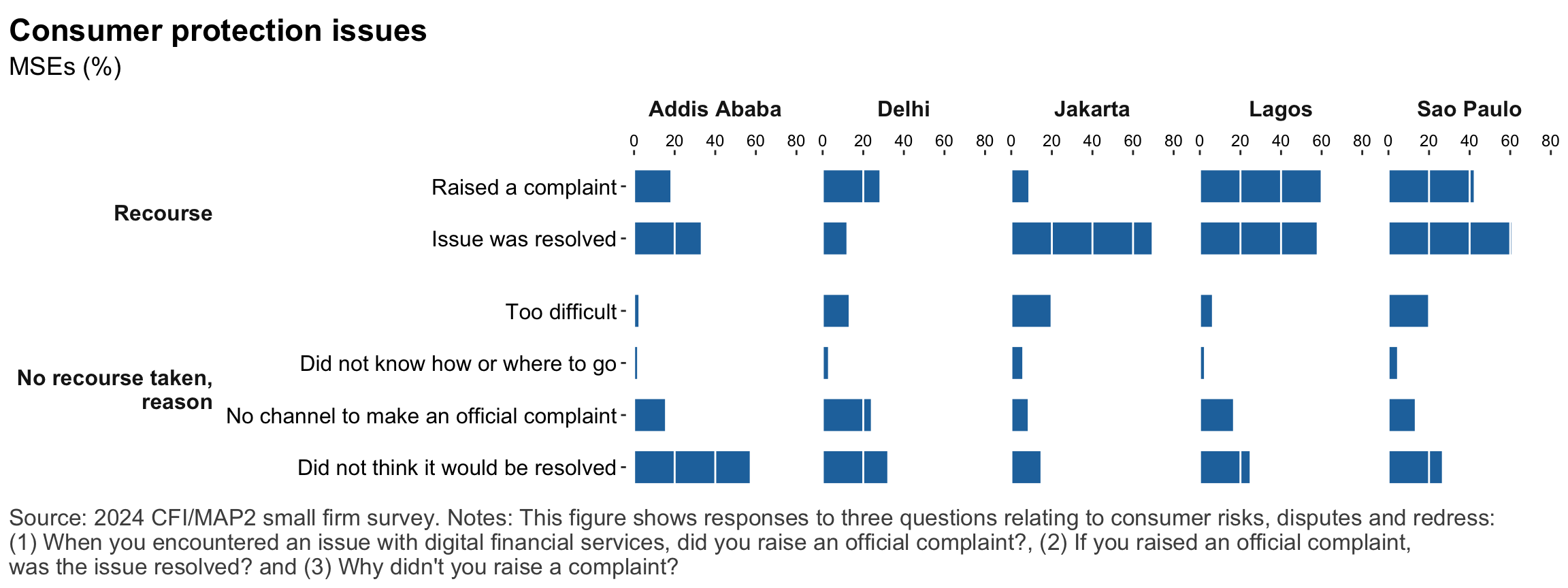

Figure 36: Consumer protection issues

Figure 37: Consumer protection issues

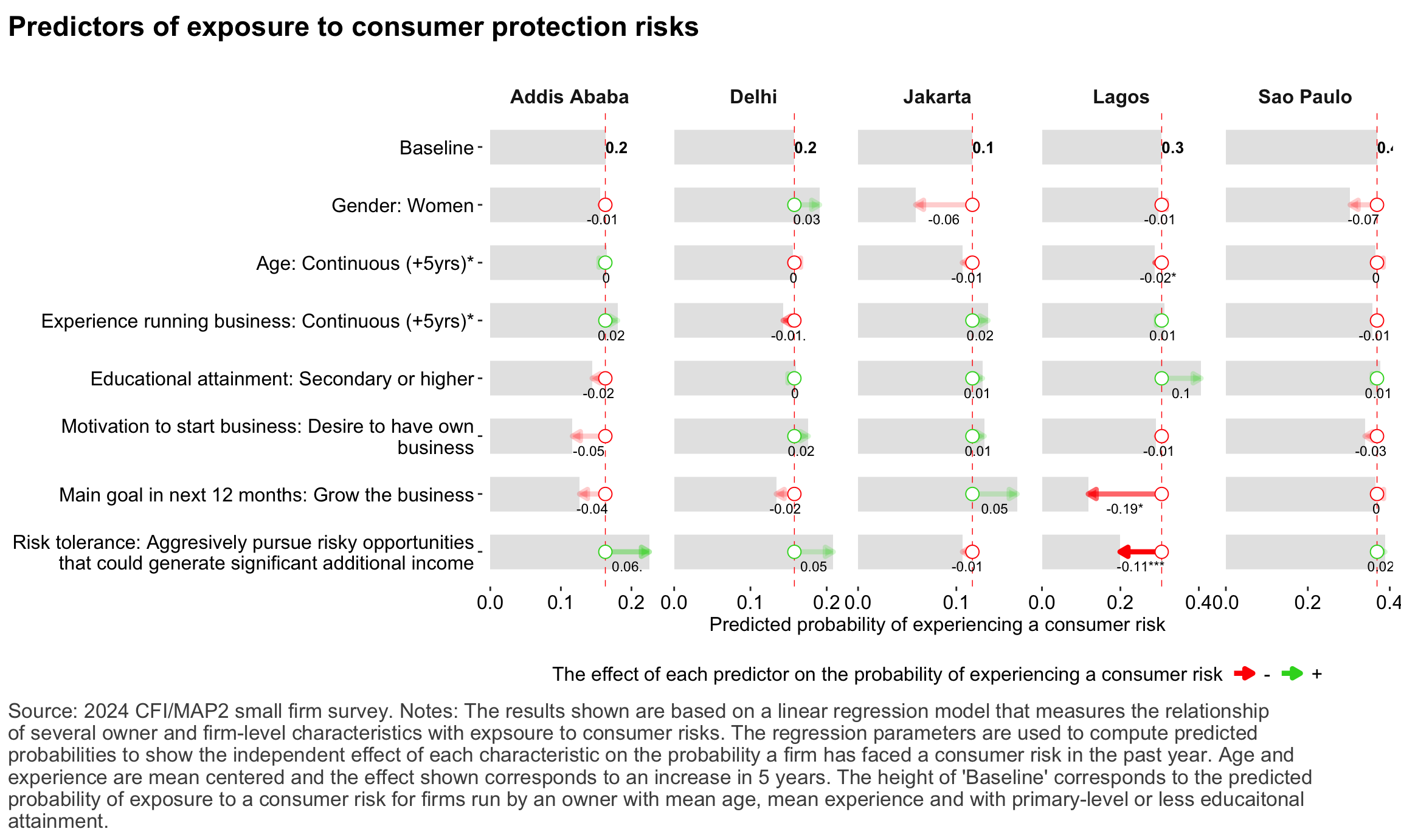

Figure 38: Predictors of consumer protection risks: Demographics

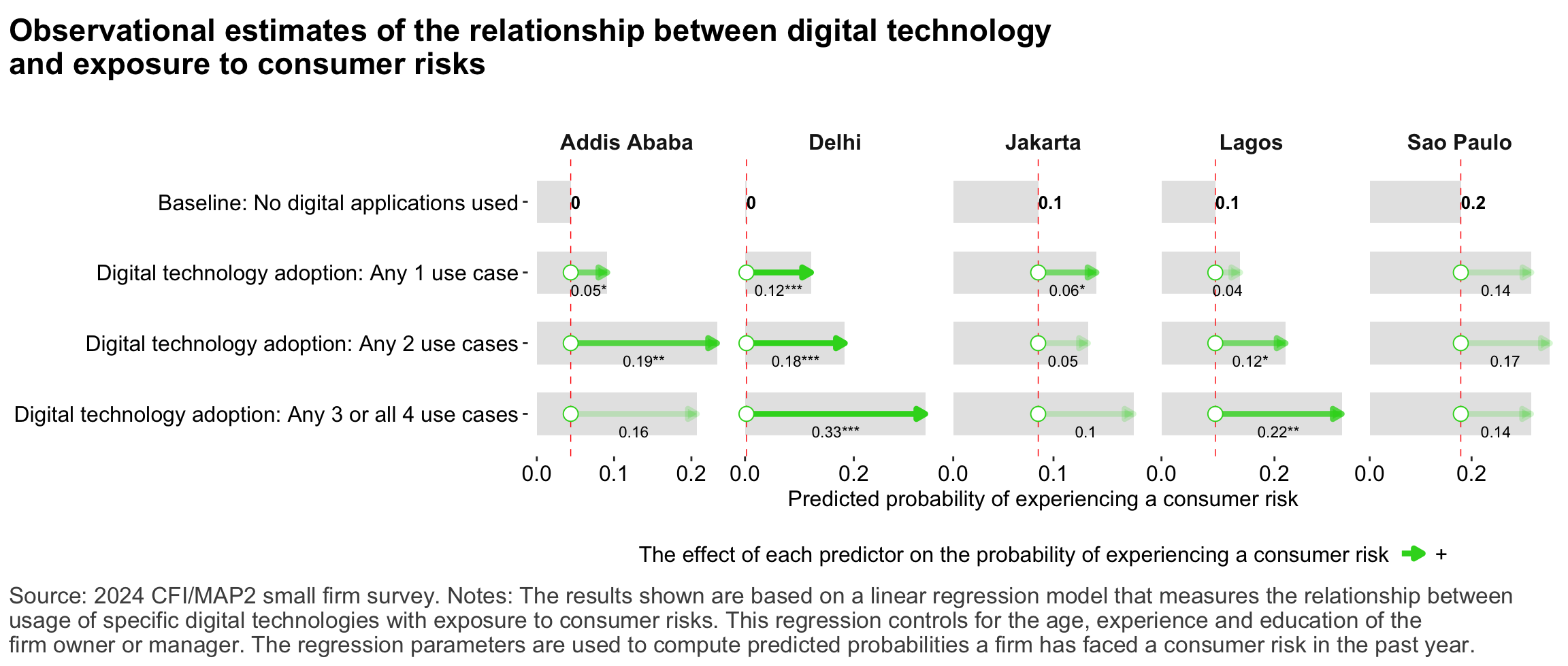

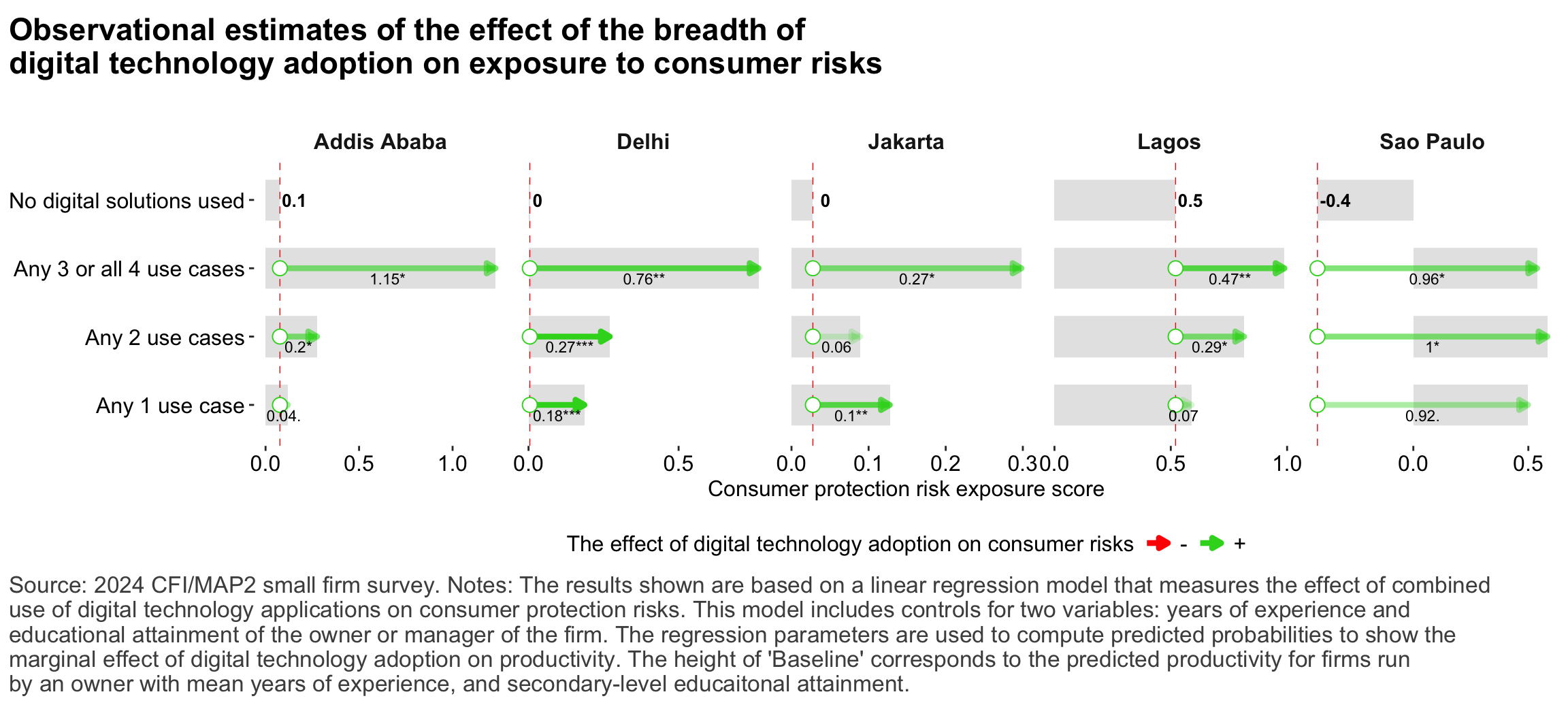

Figure 39: Predictors of exposure to consumer risks: Breadth of digital technologies

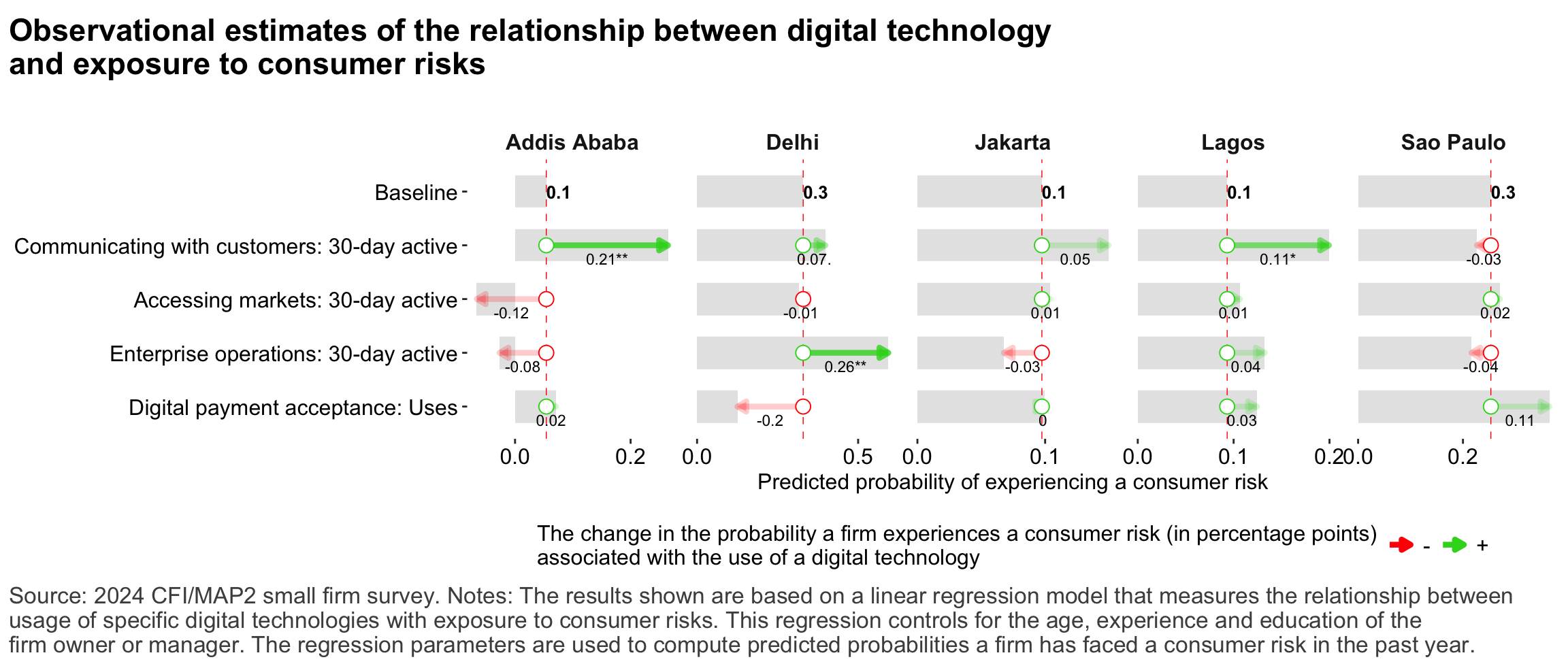

Figure 40: Predictors of exposure to consumer risks: Non-financial digital technologies

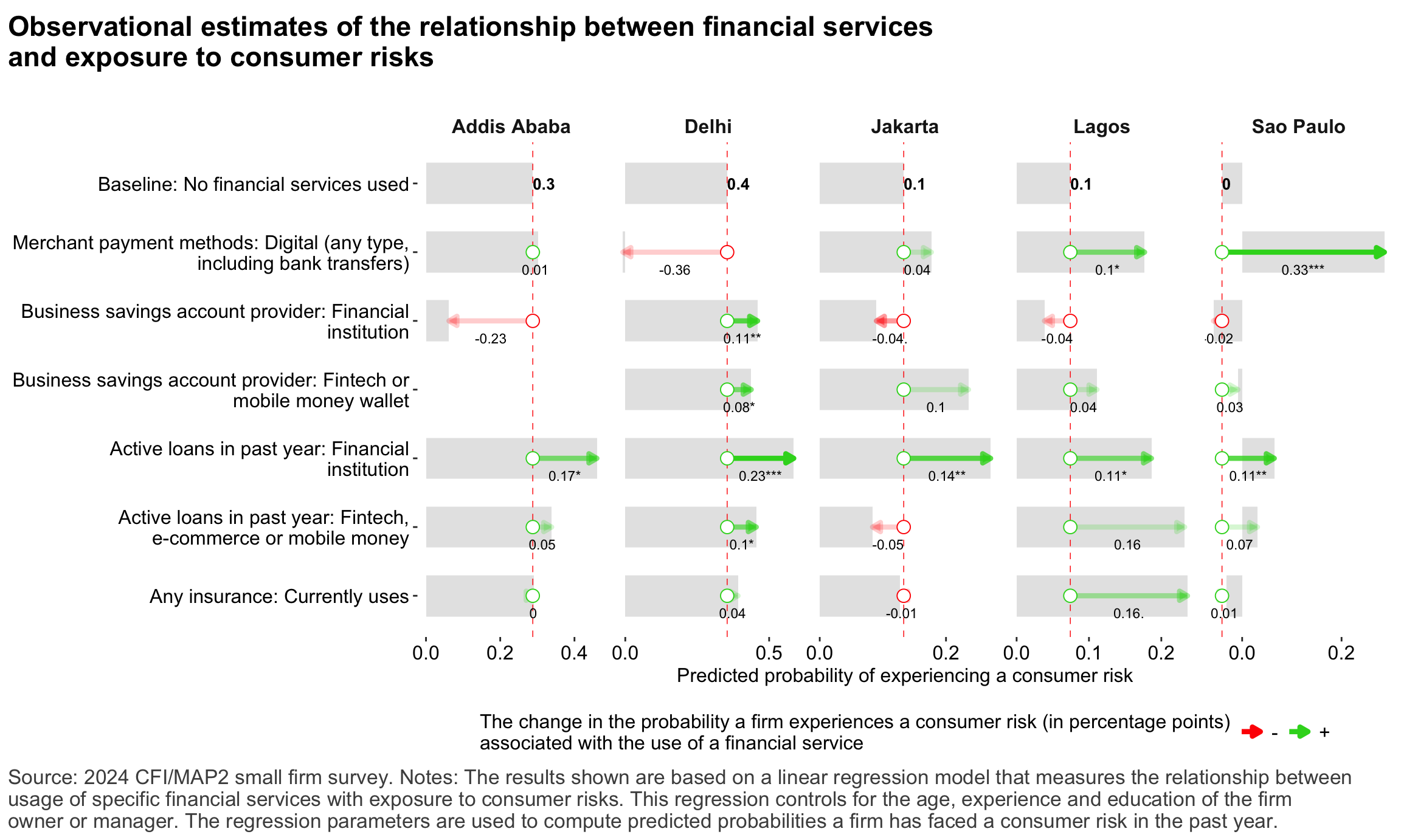

Figure 41: Predictors of exposure to consumer risks: Financial services

Figure 42: Relationship between depth of digital technology adoption and exposure to consumer protection risks

Risks and Resilience

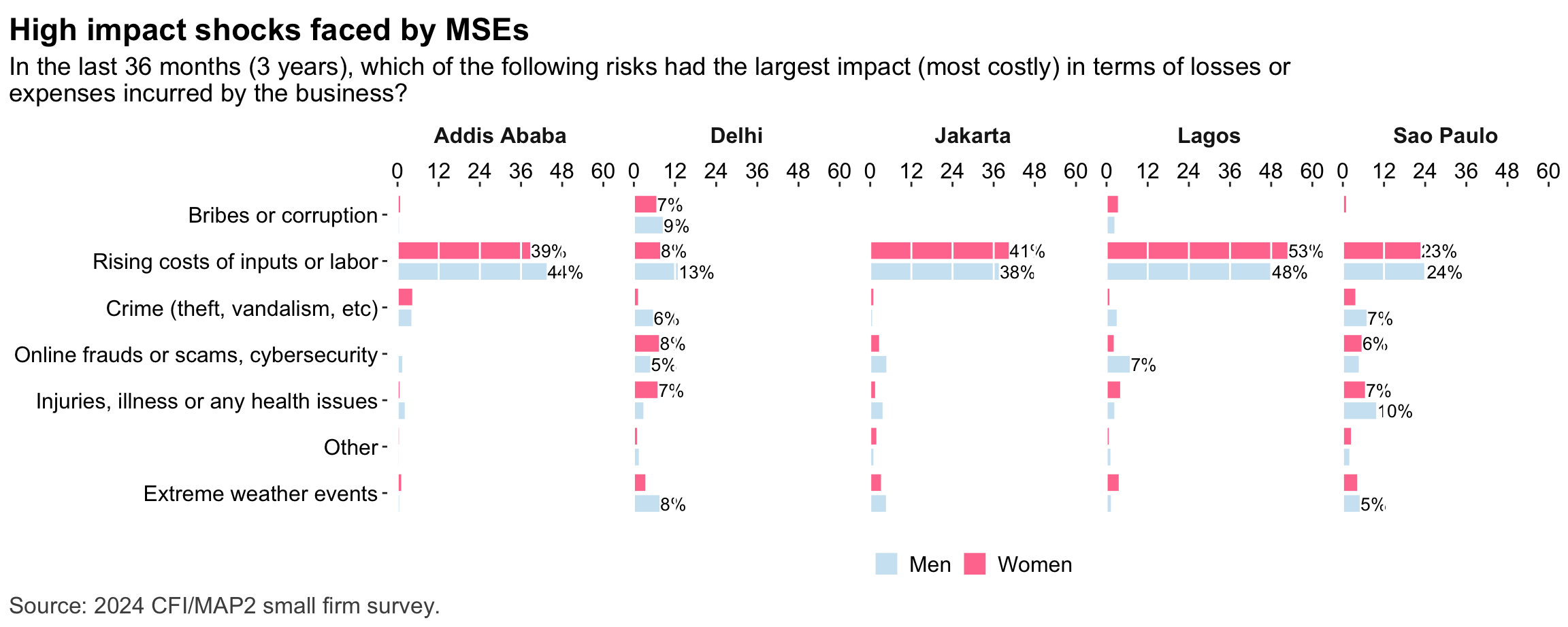

Figure 43: Risks: General

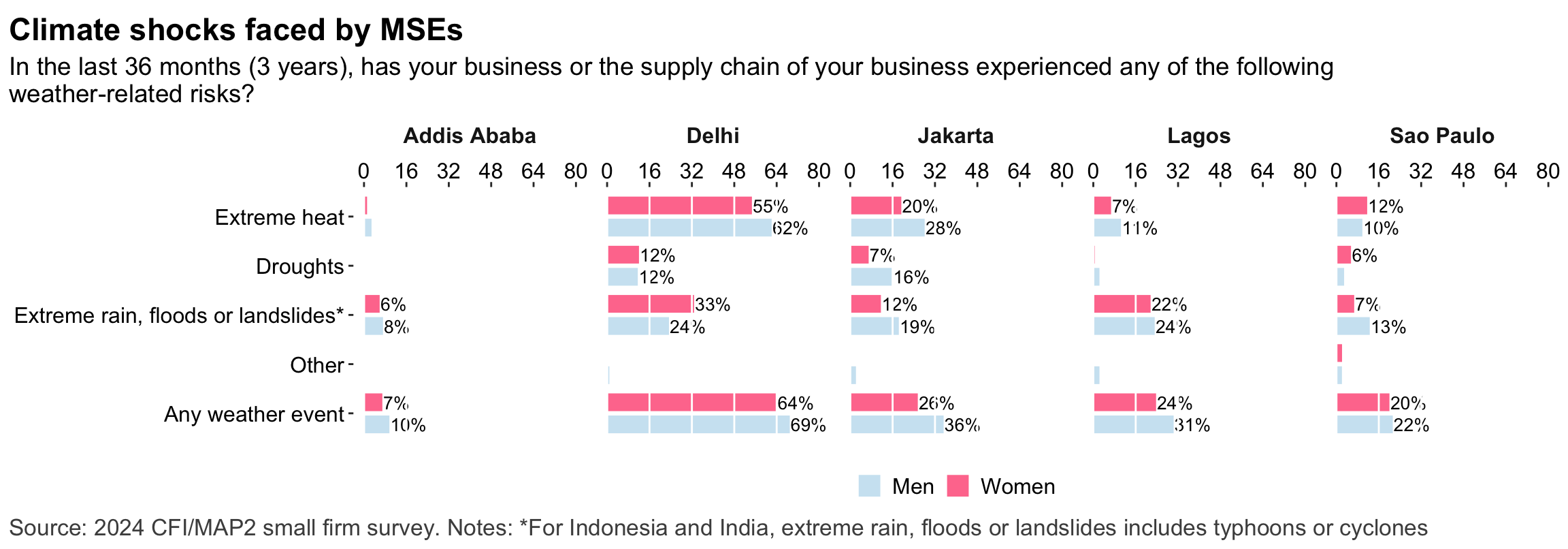

Figure 44: Risks: Climate

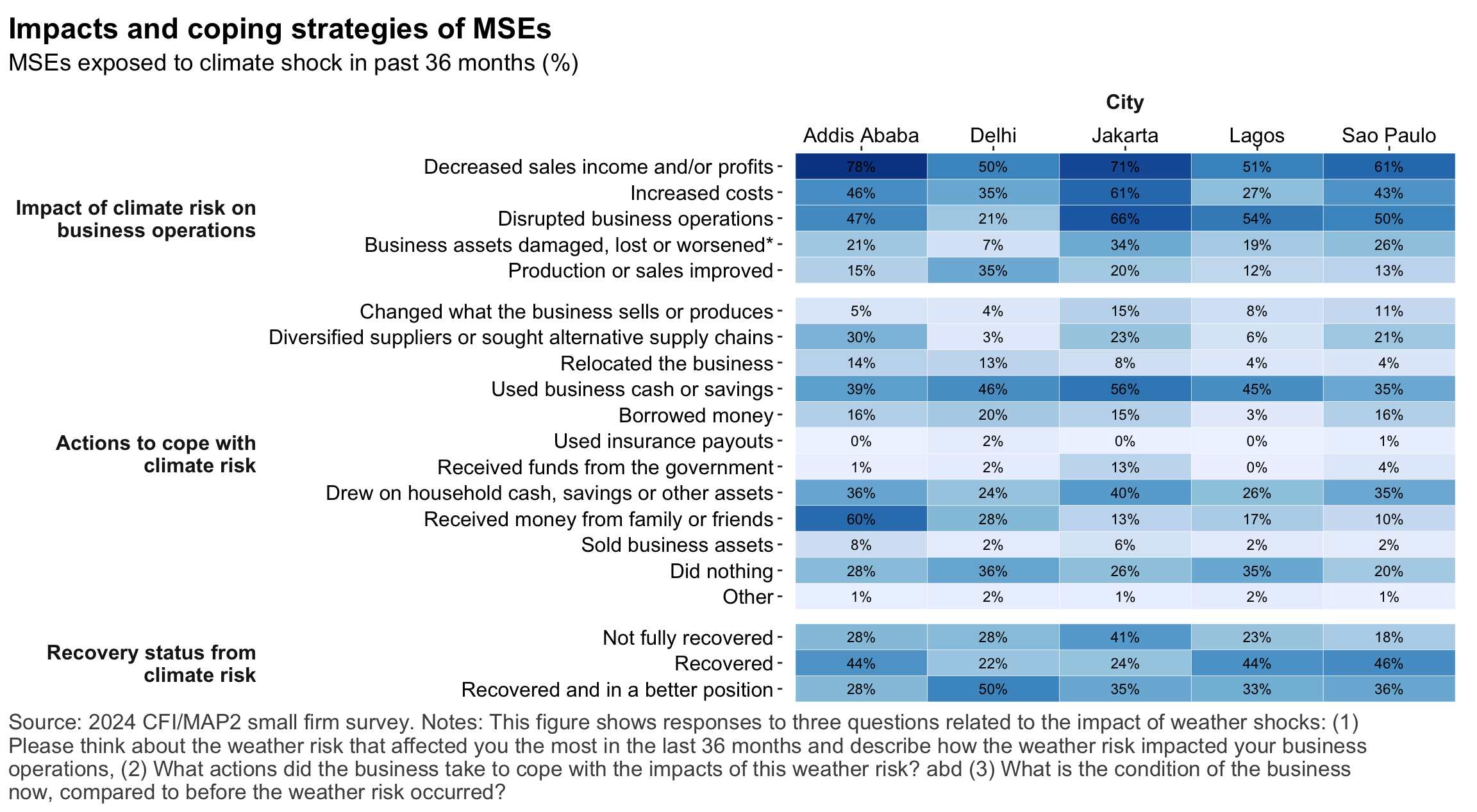

Figure 45: Risks: Impacts

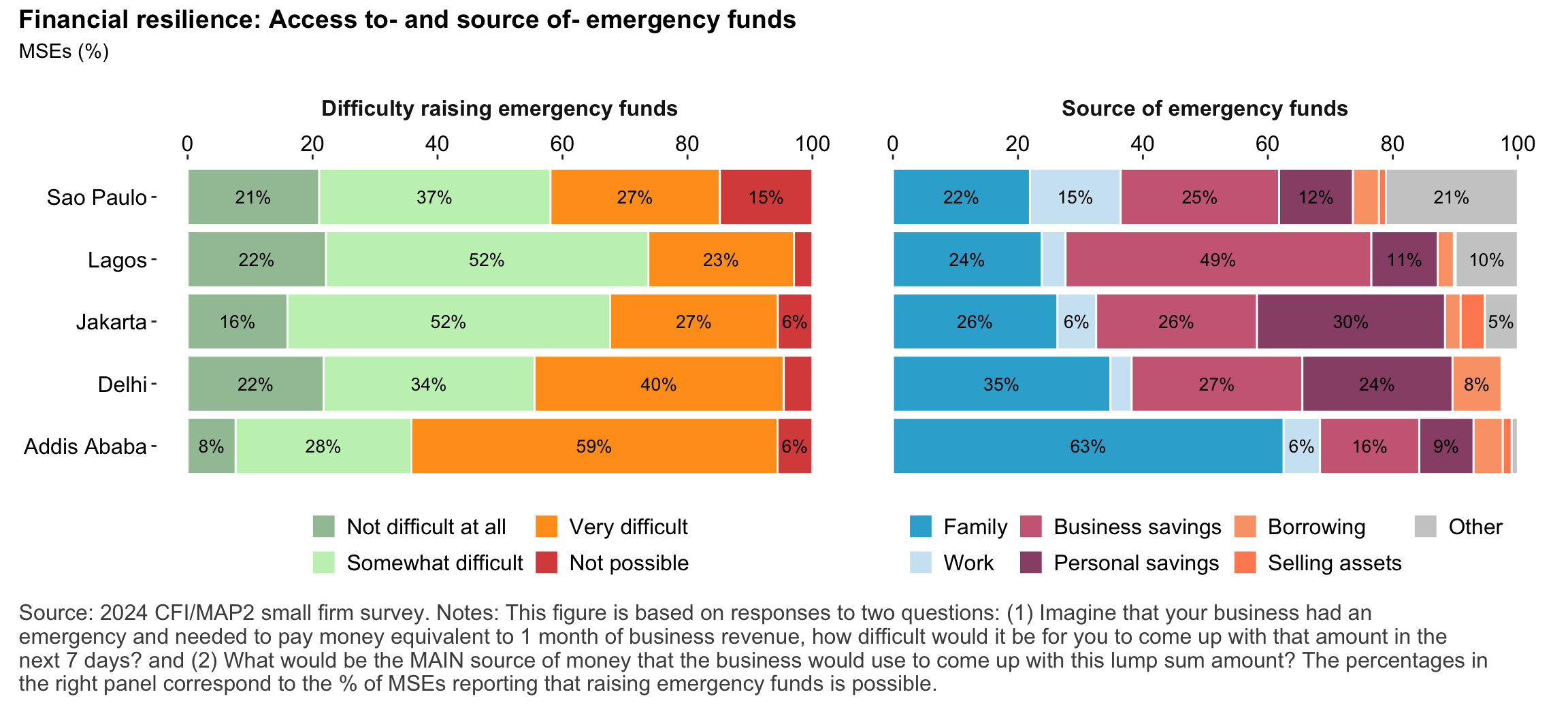

Figure 46: Financial resilience

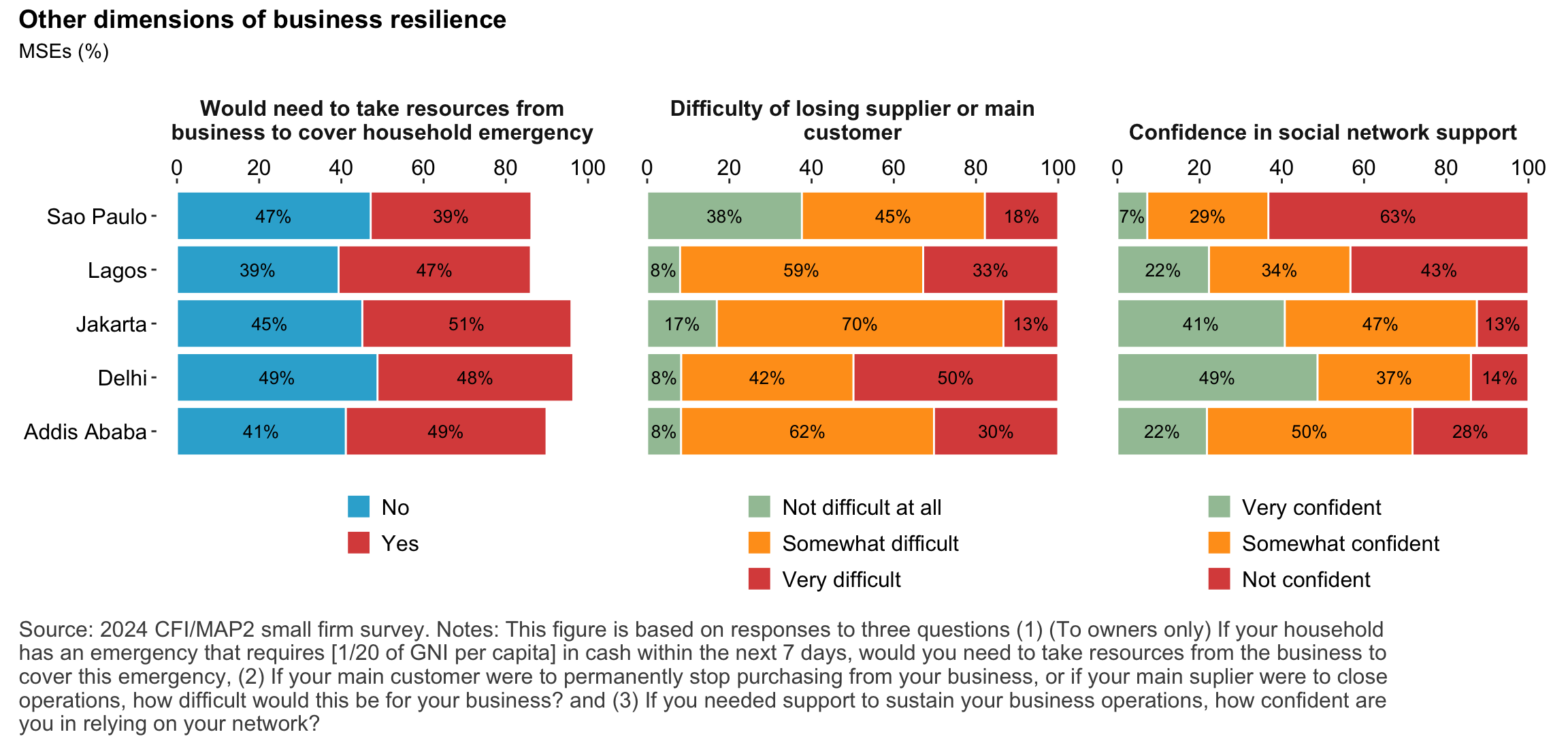

Figure 47: Non-financial dimensions of business resilience

Figure 48: Access to connectivity and devices

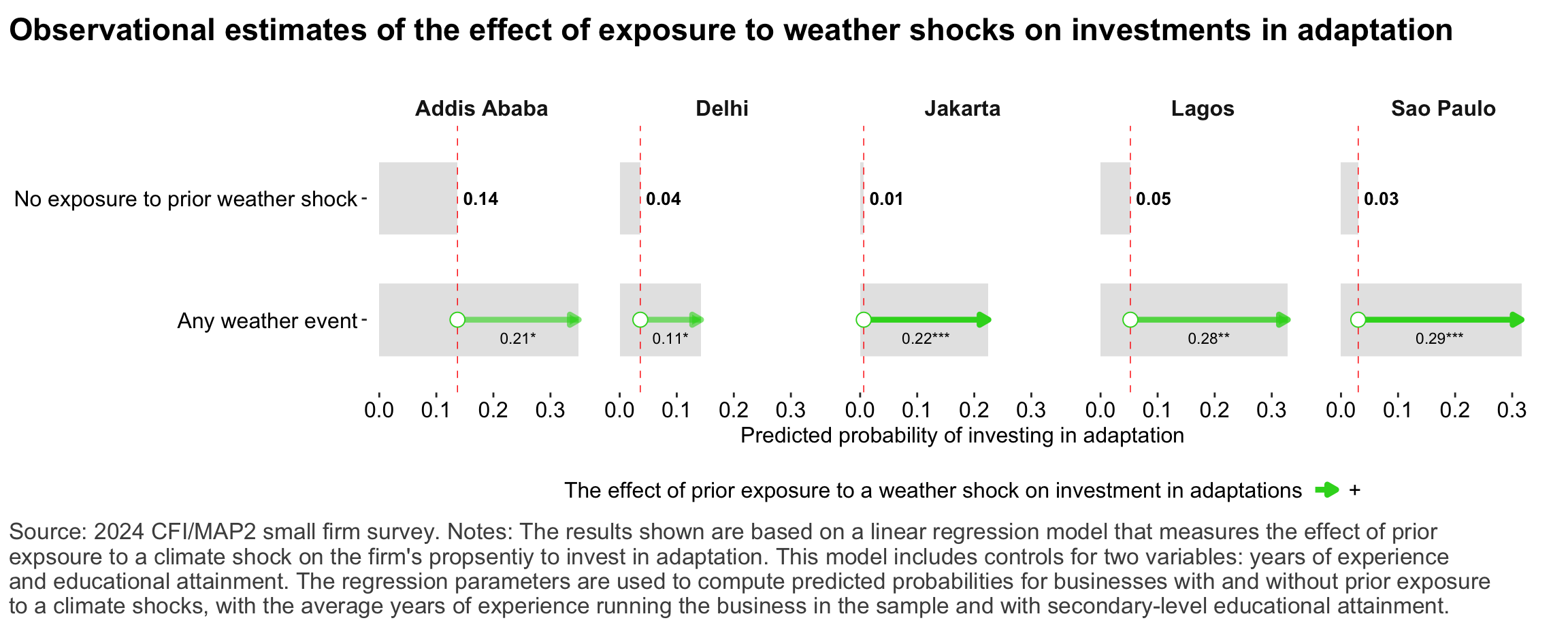

Figure 49: Relationship between prior exposure to weather shock and investment in adaptation

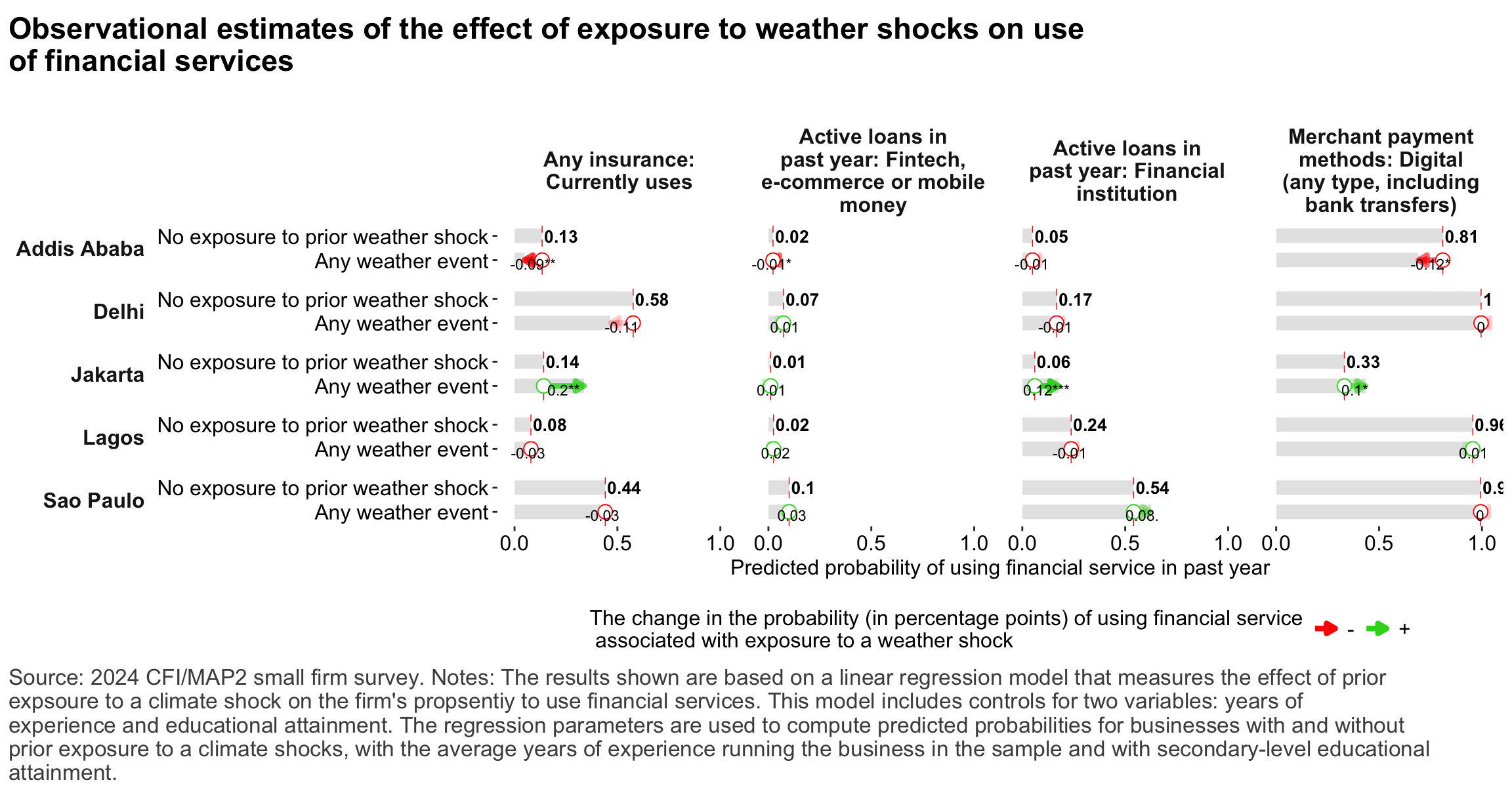

Figure 50: Relationship between prior exposure to weather shock and use of financial services

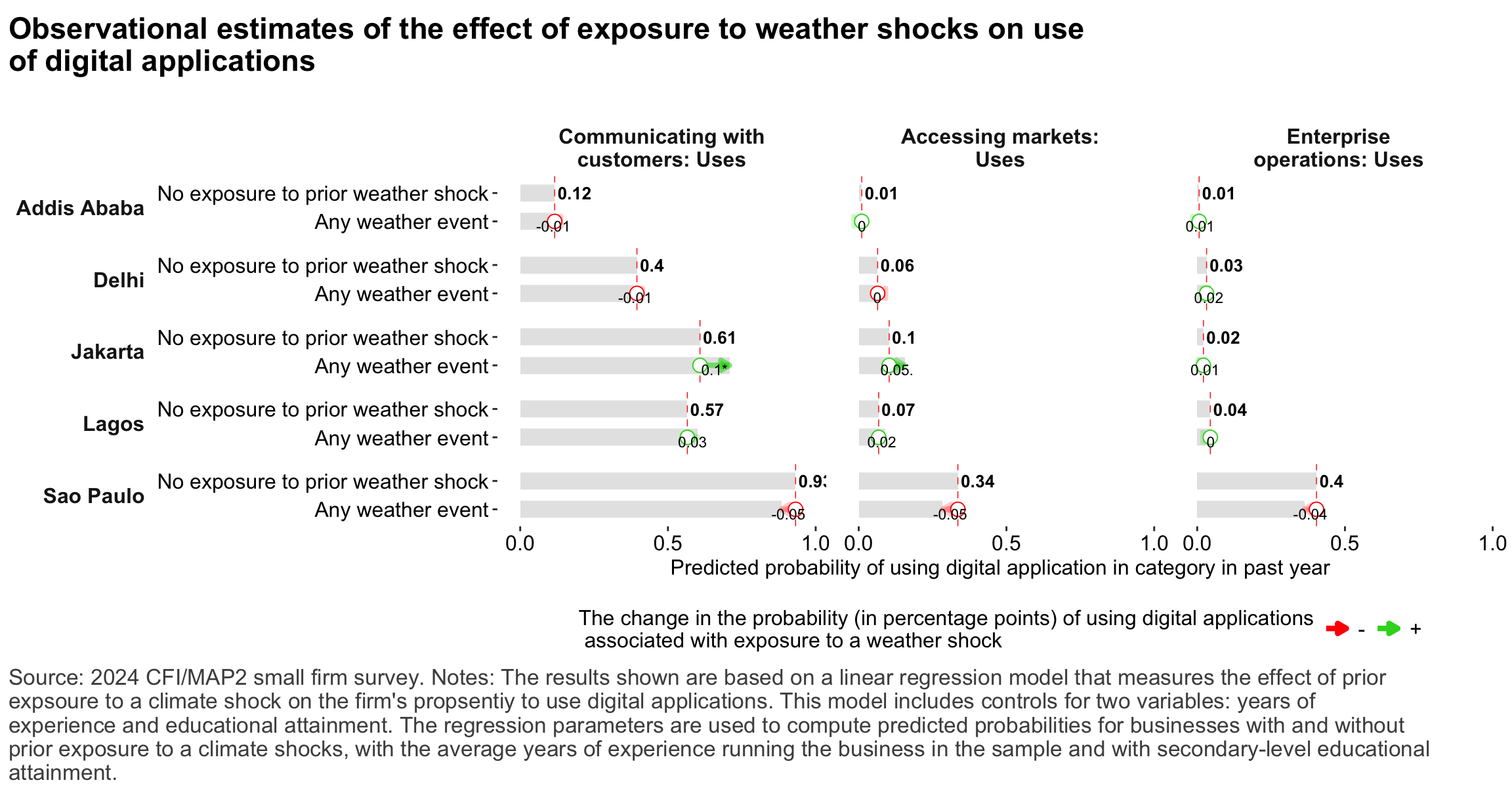

Figure 51: Relationship between prior exposure to weather shock and use of digital tools

Figure 52: Relationship between overall technology adoption & resilience

Annex

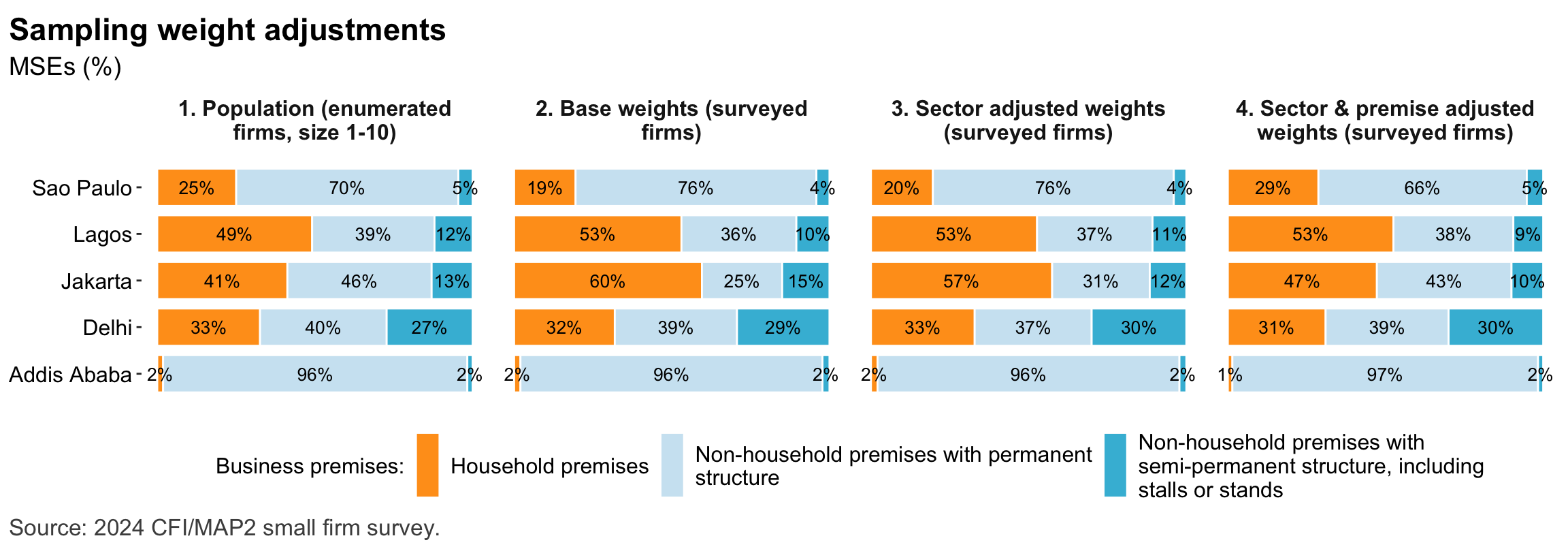

Figure 53: MSEs by premises type

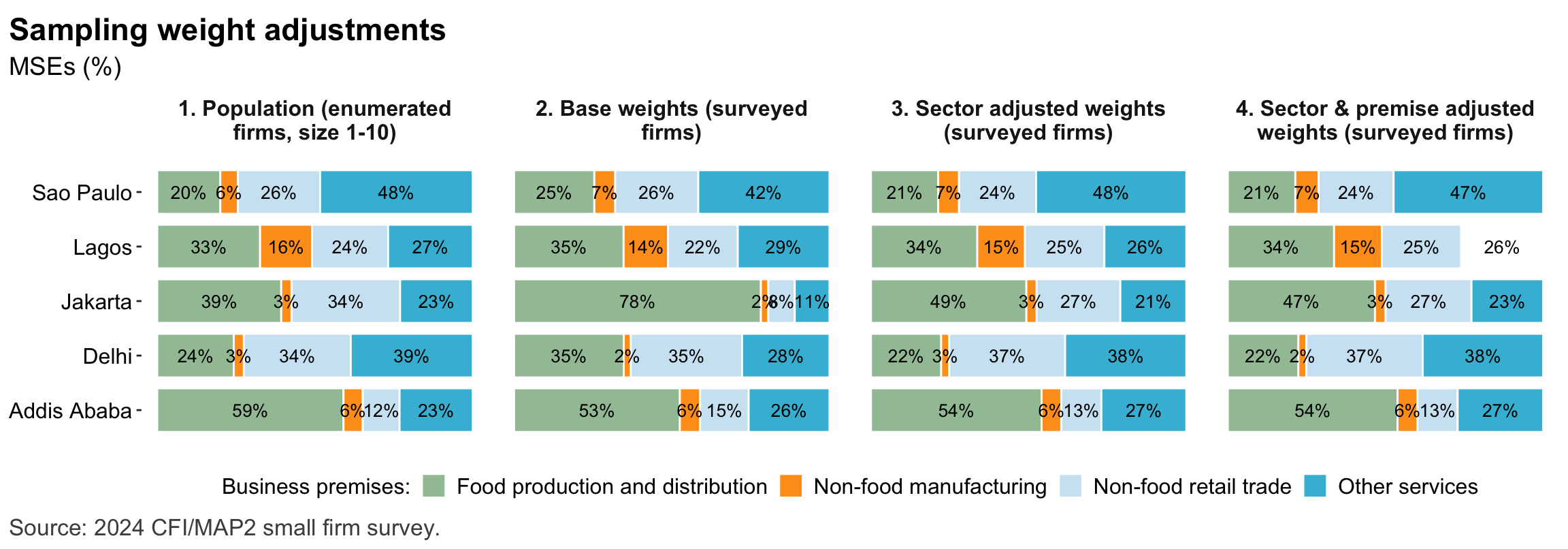

Figure 54: MSES by sector

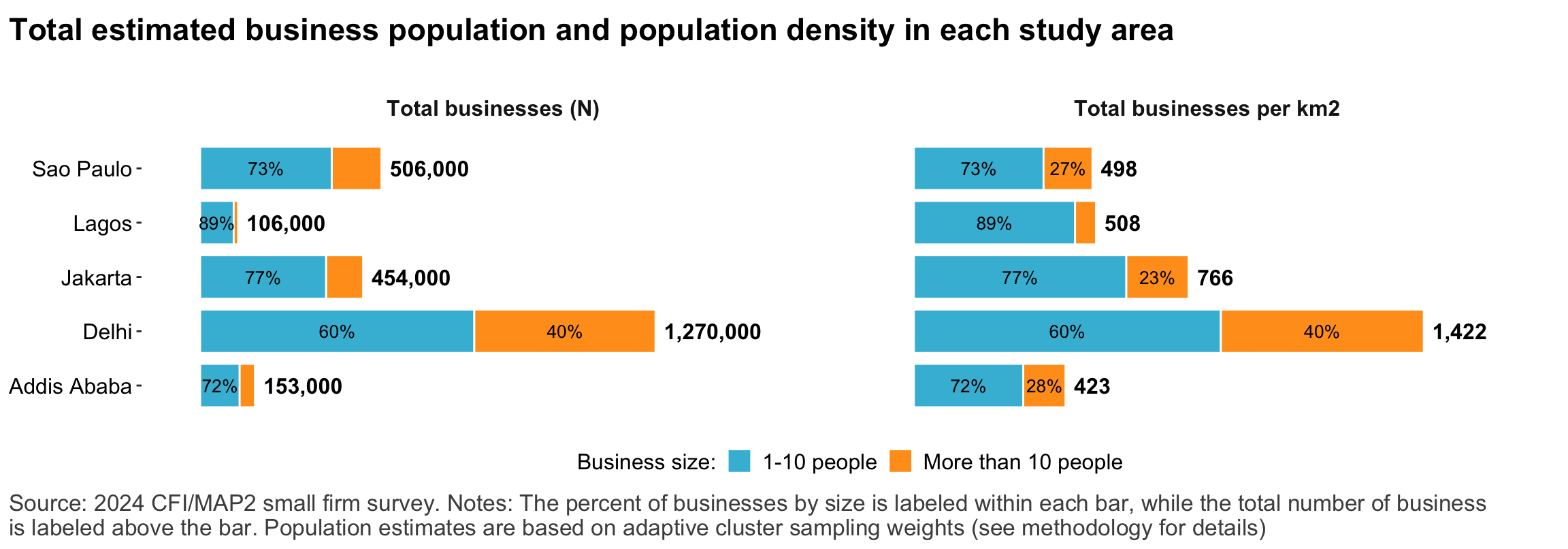

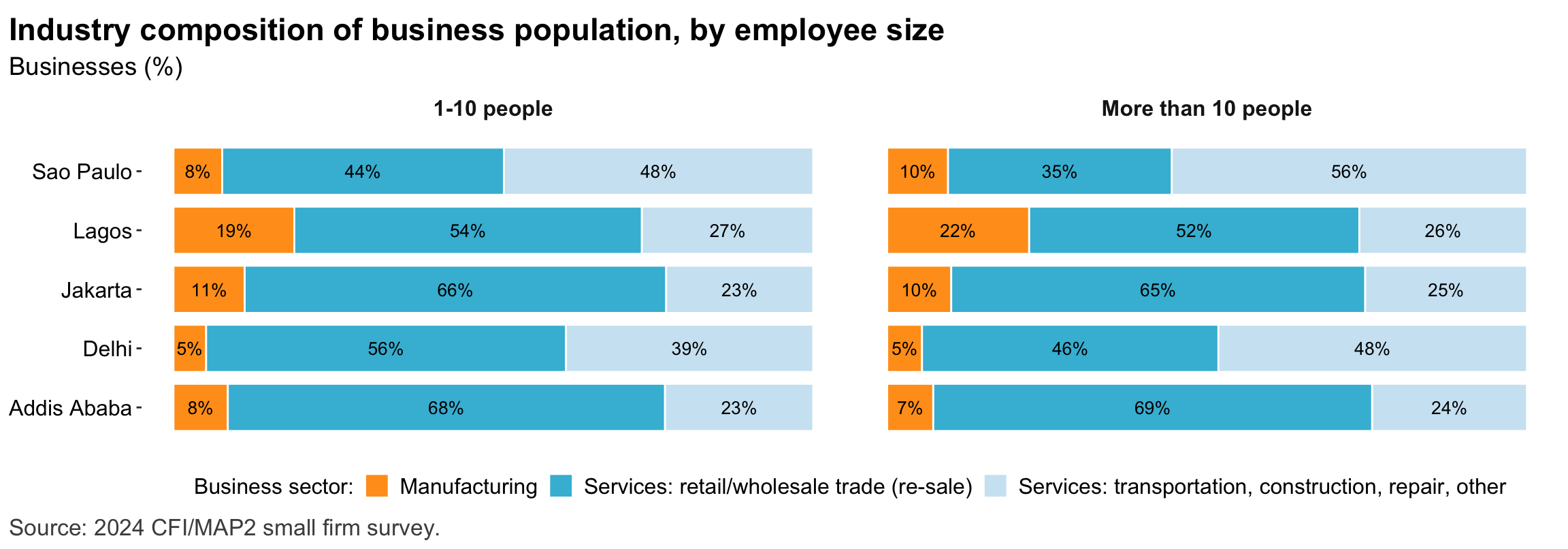

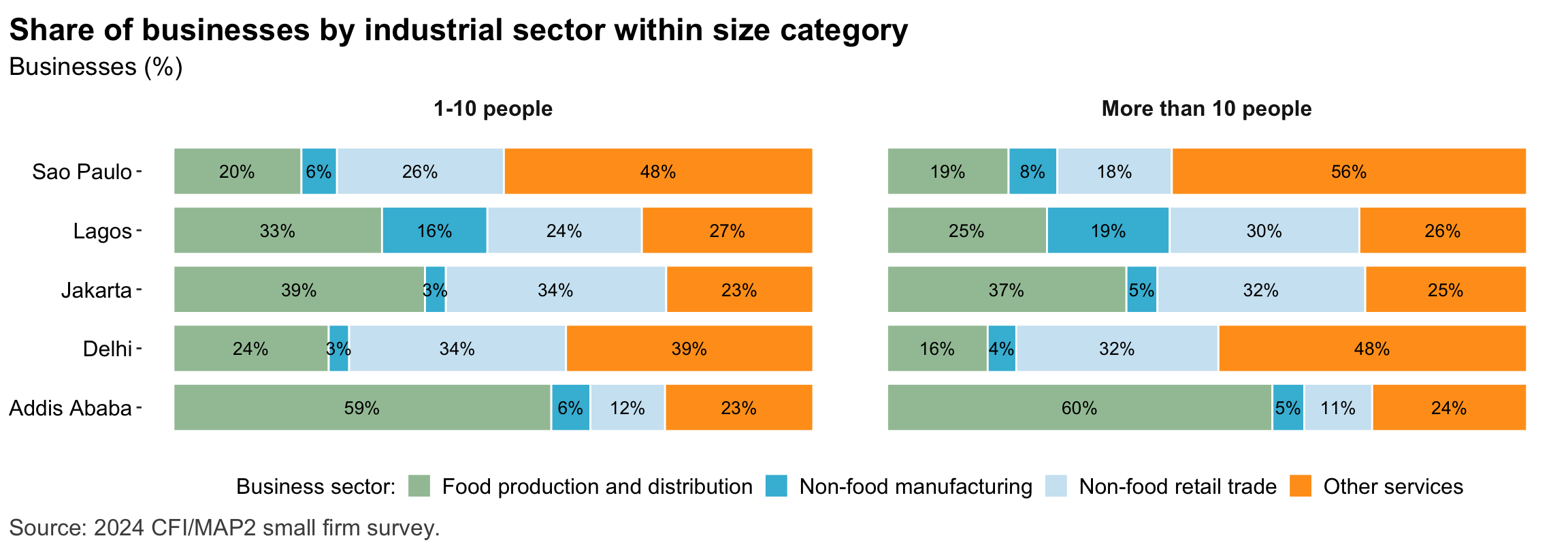

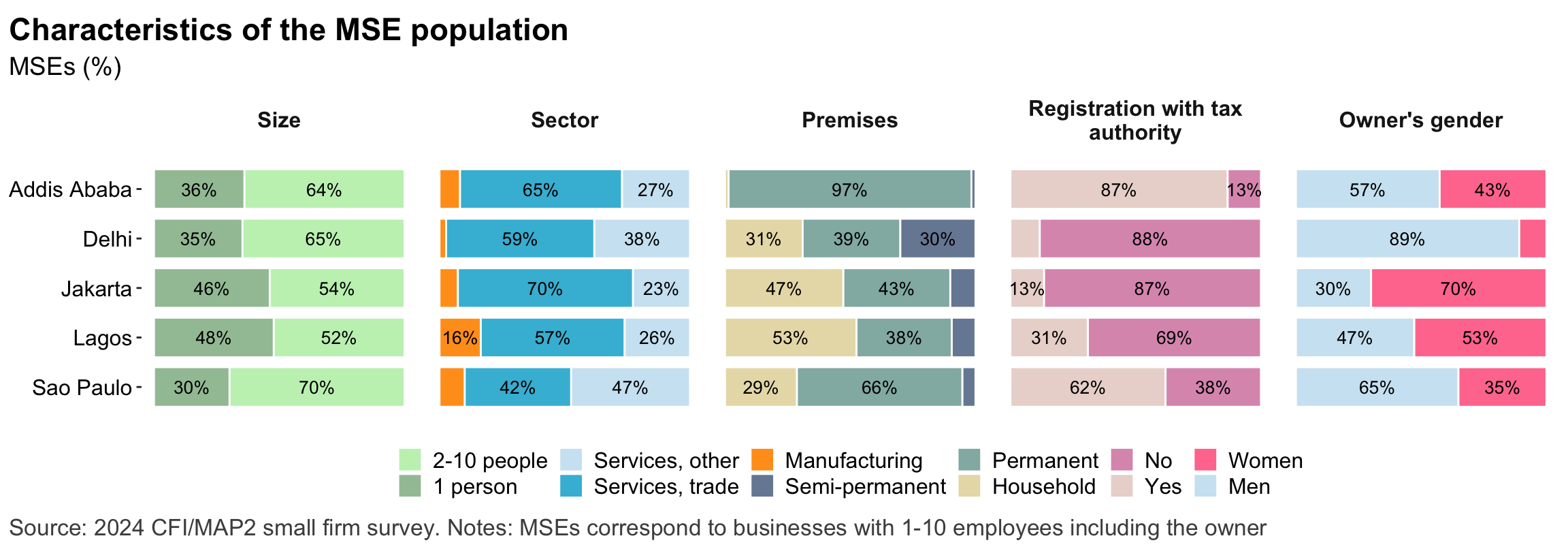

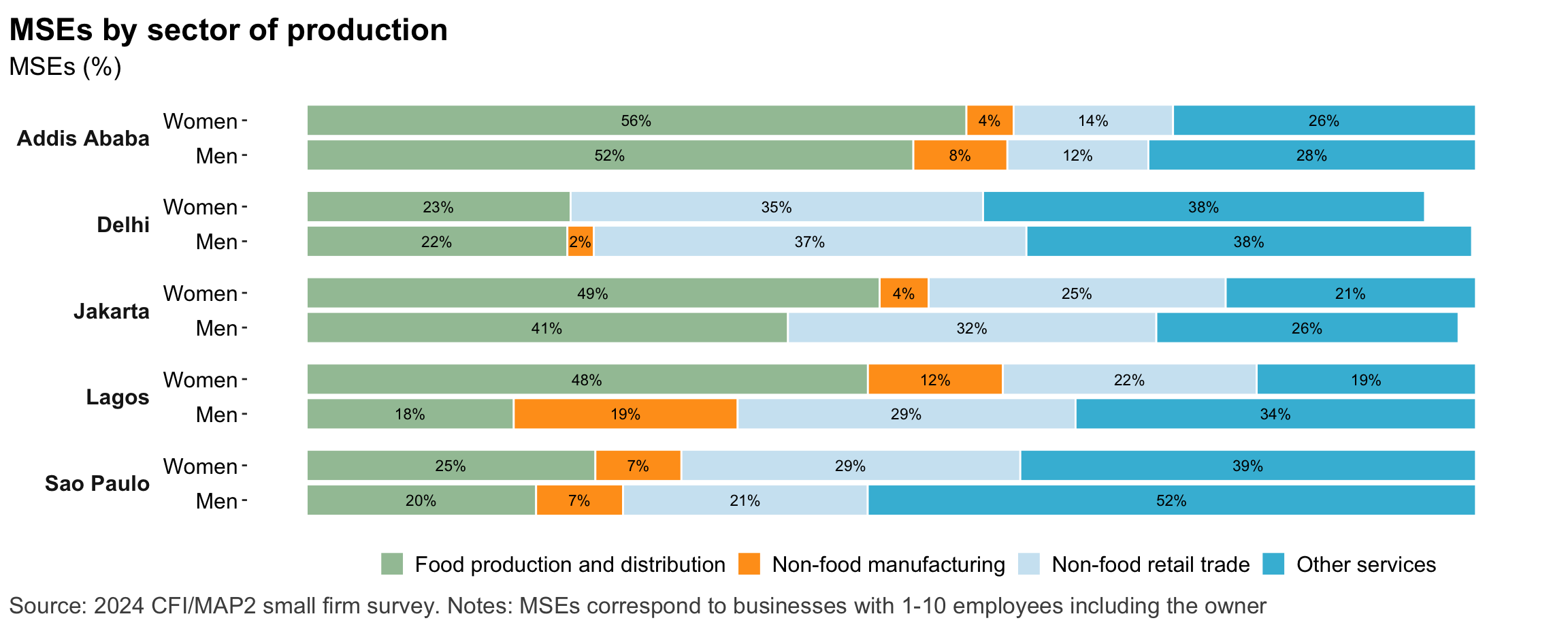

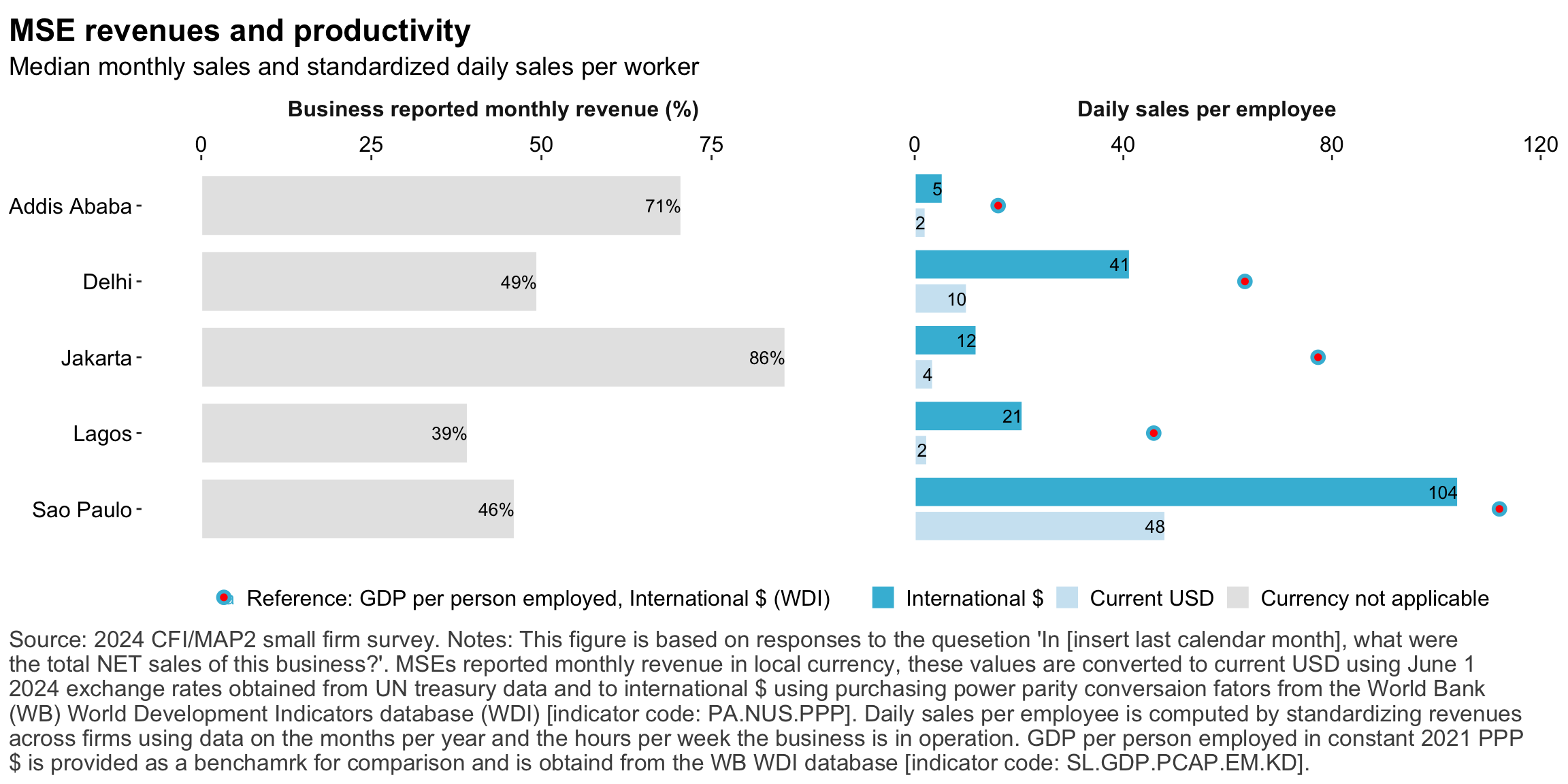

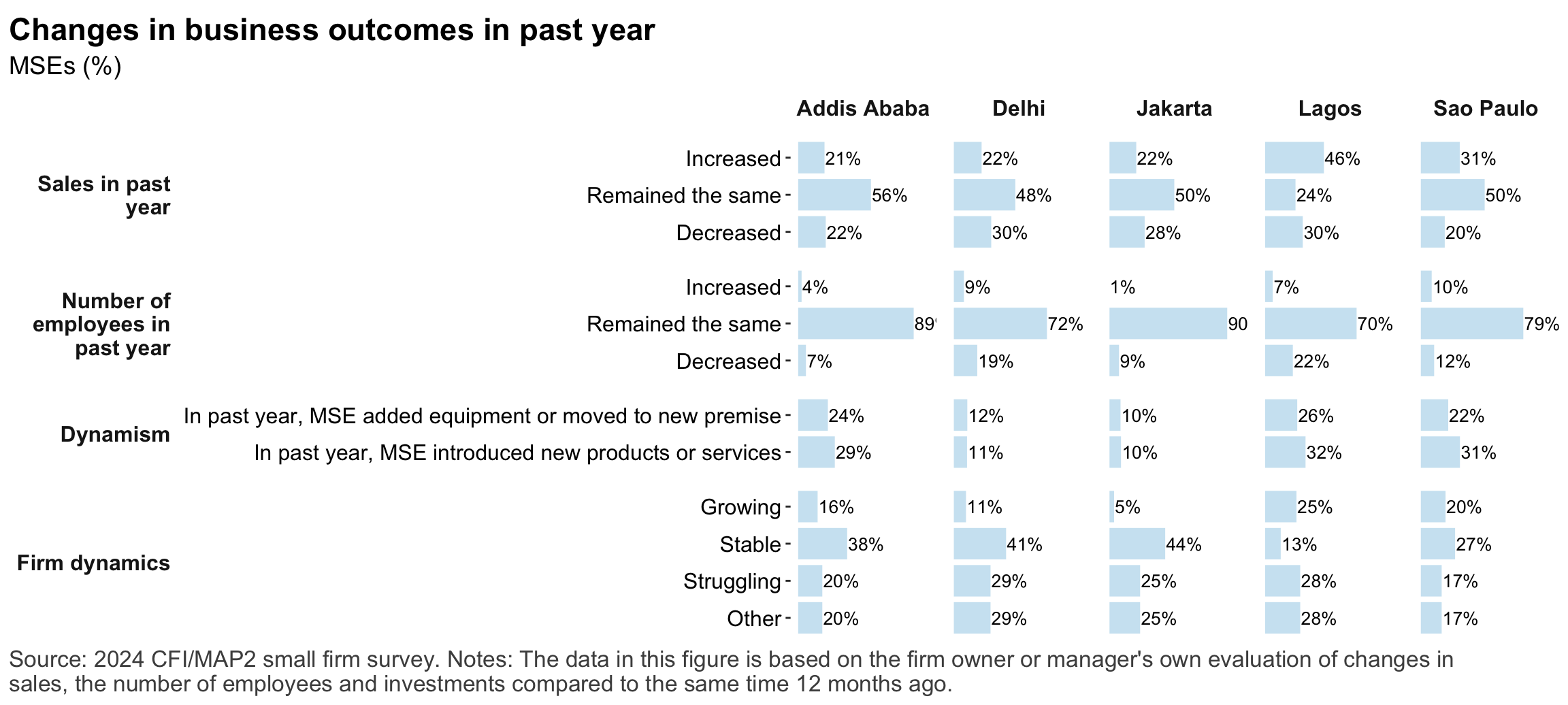

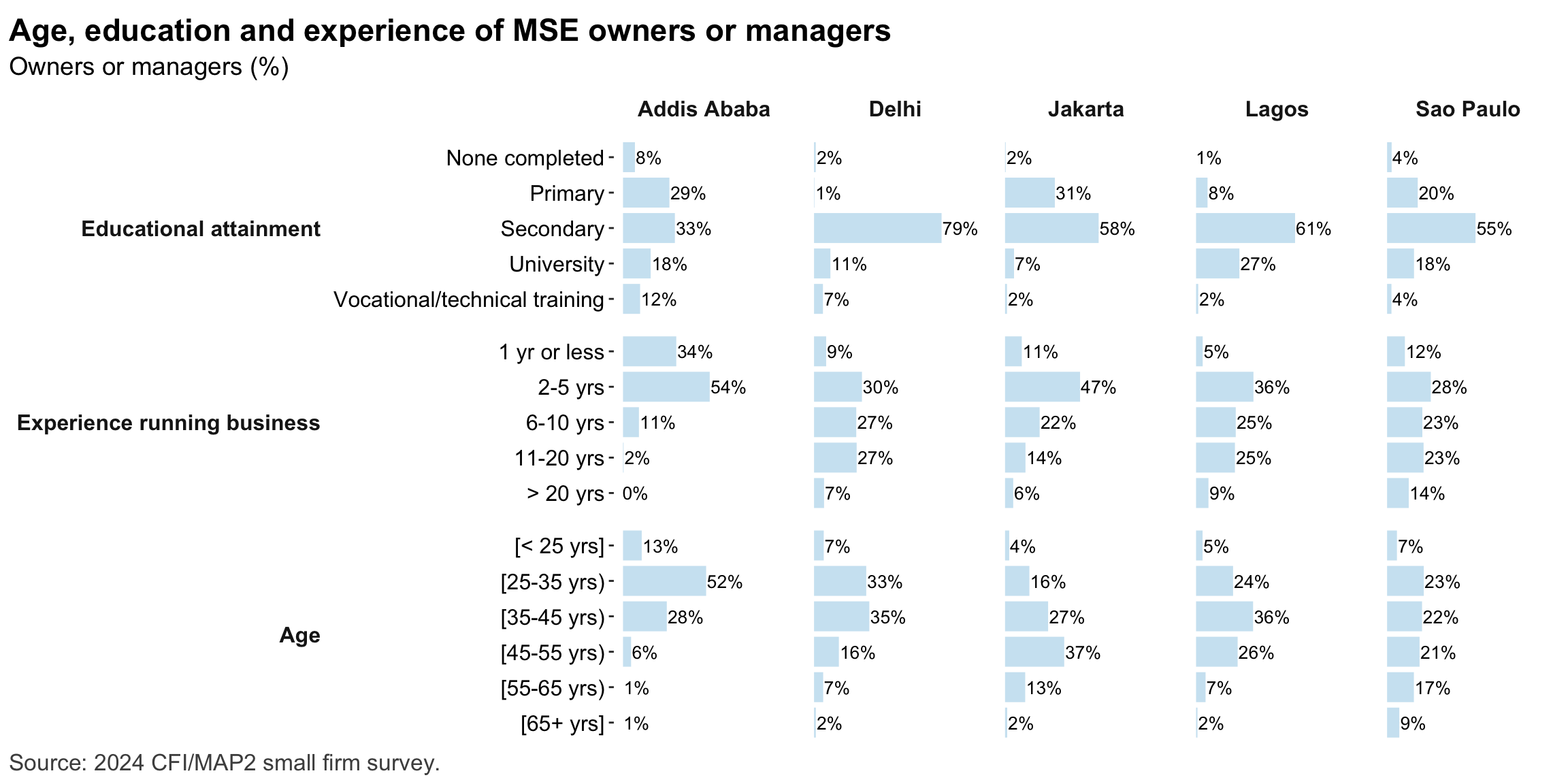

Figure 1: Businesses enumerated by sizeFigure 2: Businesses enumerated by sectorFigure 3: Businesses enumerated by sectorFigure 4: Sample characteristicsFigure 5: MSEs by sector of productionFigure 6: MSE revenues and productivityFigure 7: Changes in MSE outcomes in past yearFigure 8: MSE owner characteristicsFigure 9: Pyschographic characrteristics of SME owners or managers, by genderFigure 10: Pyschographic characrteristics of SME owners or managers, by genderFigure 11: Correlation between owner’s motivations, goals and attitudes to riskFigure 12: Summary measures of financial accessFigure 13: Access to connectivity and devicesFigure 14: Drivers of overall technology adoptionFigure 15: Applications of digital technologyFigure 16: Depth of digital technology adoptionFigure 17: Non-financial digital technology adoption factorsFigure 18: Relationship between internet-connectivity and firm-level labor productivityFigure 19: Relationship between digital technology and firm-level labor productivityFigure 20: Relationship between general digital technology adoption and subjective growthFigure 21: Relationship between digital technology adoption and firm-level labor productivityFigure 22: Relationship between digital technology adoption and firm-level labor productivityFigure 23: Relationship between depth of digital technology adoption and firm-level labor productivityFigure 24: Summary measures of financial accessFigure 25: Financical accounts and savingsFigure 26: Merchant paymentsFigure 27: Demand for creditFigure 28: Barriers to creditFigure 29: Impacts of digital financial servicesFigure 30: Insurance usageFigure 31: Relationship between financial services and firm-level labor productivityFigure 32: Relationship between financial services and financial resilienceFigure 33: Relationship between financial services and firm growthFigure 34: Relationship between financial services and capital investmentFigure 35: Challenges with loan repaymentFigure 36: Consumer protection issuesFigure 37: Consumer protection issuesFigure 38: Predictors of consumer protection risks: DemographicsFigure 39: Predictors of exposure to consumer risks: Breadth of digital technologiesFigure 40: Predictors of exposure to consumer risks: Non-financial digital technologiesFigure 41: Predictors of exposure to consumer risks: Financial servicesFigure 42: Relationship between depth of digital technology adoption and exposure to consumer protection risksFigure 43: Risks: GeneralFigure 44: Risks: ClimateFigure 45: Risks: ImpactsFigure 46: Financial resilienceFigure 47: Non-financial dimensions of business resilienceFigure 48: Access to connectivity and devicesFigure 49: Relationship between prior exposure to weather shock and investment in adaptationFigure 50: Relationship between prior exposure to weather shock and use of financial servicesFigure 51: Relationship between prior exposure to weather shock and use of digital toolsFigure 52: Relationship between overall technology adoption & resilienceFigure 53: MSEs by premises typeFigure 54: MSES by sector